3:25 pm

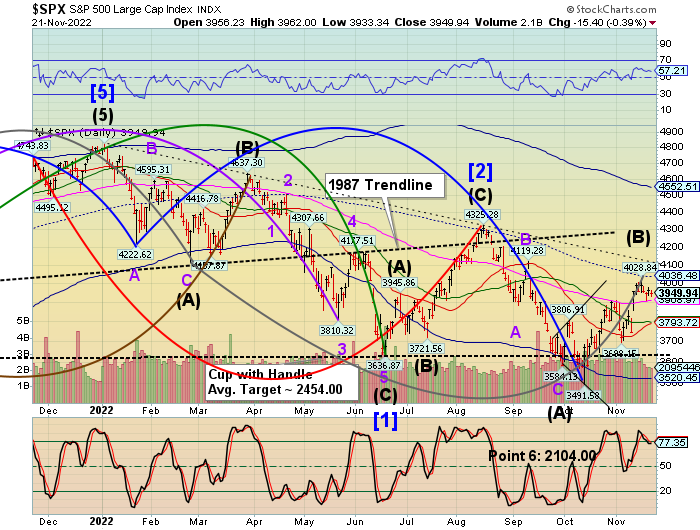

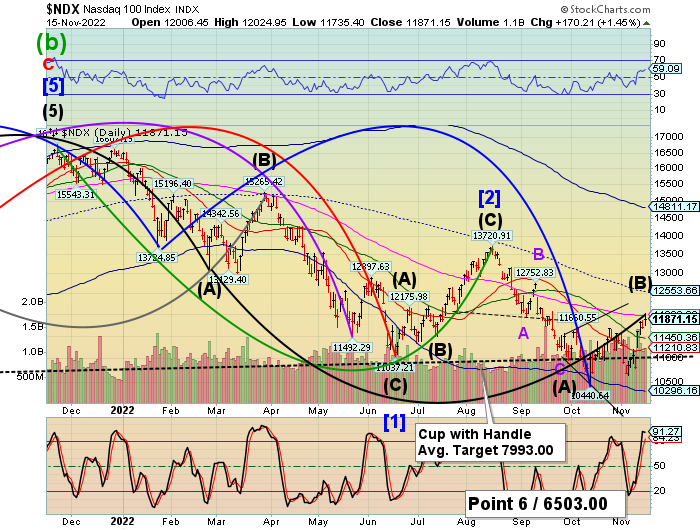

SPX has completed 30 trading days from the October 13 low, completing its final retracement push. I had previously mentioned that Friday would be a day of strength and a pivot day, to boot. It would be wise to prepare for the reversal into Intermediate Wave (C) of Primary Wave [3], a very strong combination for the next leg down.

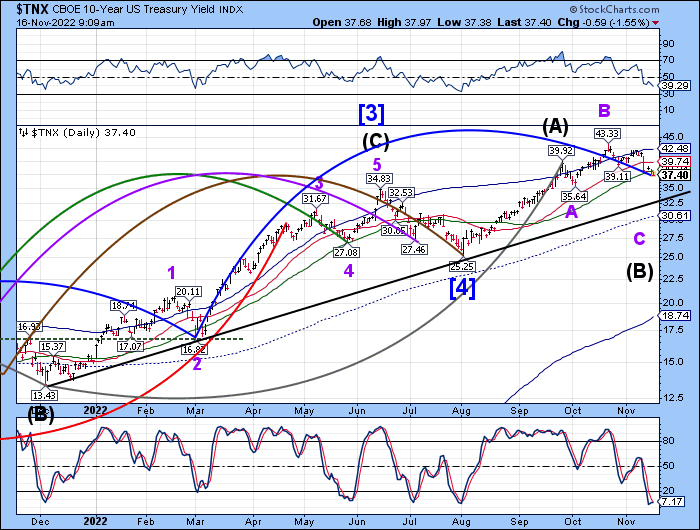

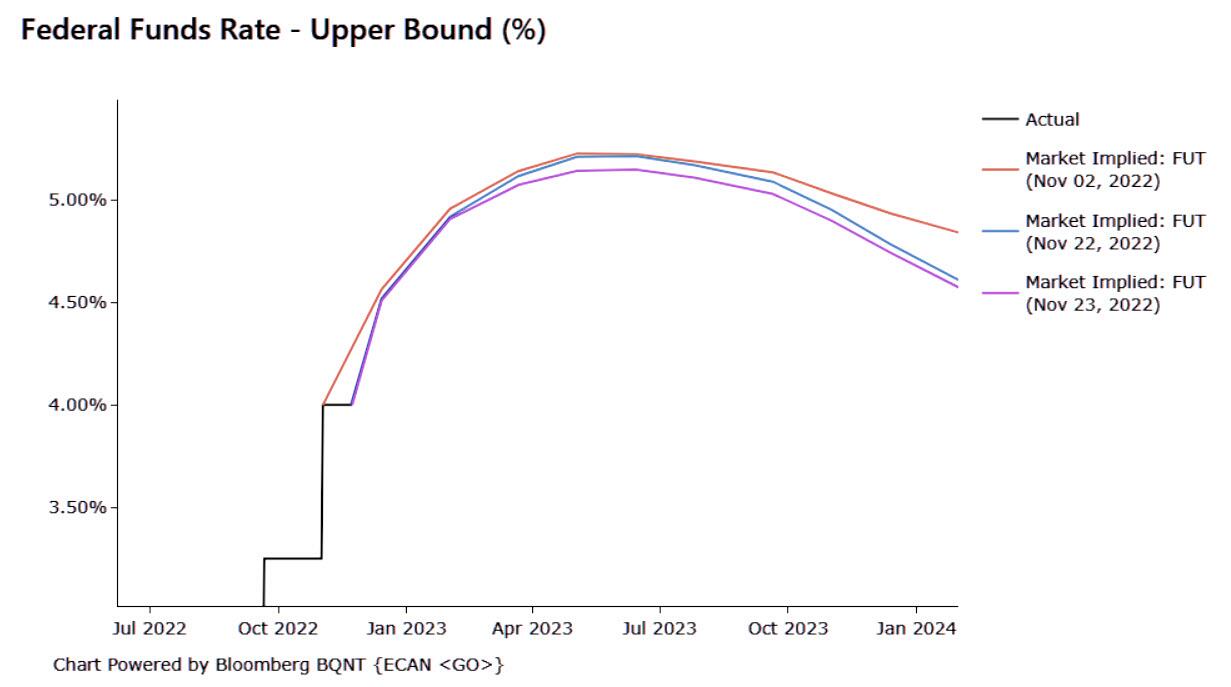

Remember, the Fed always follows the bond market. The Cycles Model already says that yields are going higher!

ZeroHedge comments, “While prevailing consensus was that the Fed didn’t really say anything unexpected, or anything that wasn’t already telegraphed both in the Nov 2 statement and subsequent Fed speak, Wall Street commentators agreed that “the statement overall comes across as dovish” as BBG Economics chief Anna Wong put it, With Integrity Asset Management’s Joe Gilbert adding that “it is constructive that Fed participants were becoming increasingly aware of the lagged impact of all the rate hikes this year. Generally, this is bullish for equities and fixed income because there is now a slight change in consensus at the Fed which means that significantly more rate hikes are now less likely.”

Wong added that “there’s widespread agreement within the committee to slow the pace of rate hikes soon, with only ‘a few’ preferring to wait until the policy stance is more clearly in restrictive territory. We think Powell belongs to this latter group.”

The market agrees with the dovish take and stocks have jumped to session highs while the market implied Fed Funds curve has dipped on the outer end,”

:30 am

Good Morning!

Thanksgiving guests are arriving for a four-day family event. My wife and I are preparing for two dozen people for Thanksgiving dinner, including an introduction to our youngest son’s new fiancée. Please excuse the brevity of this report.

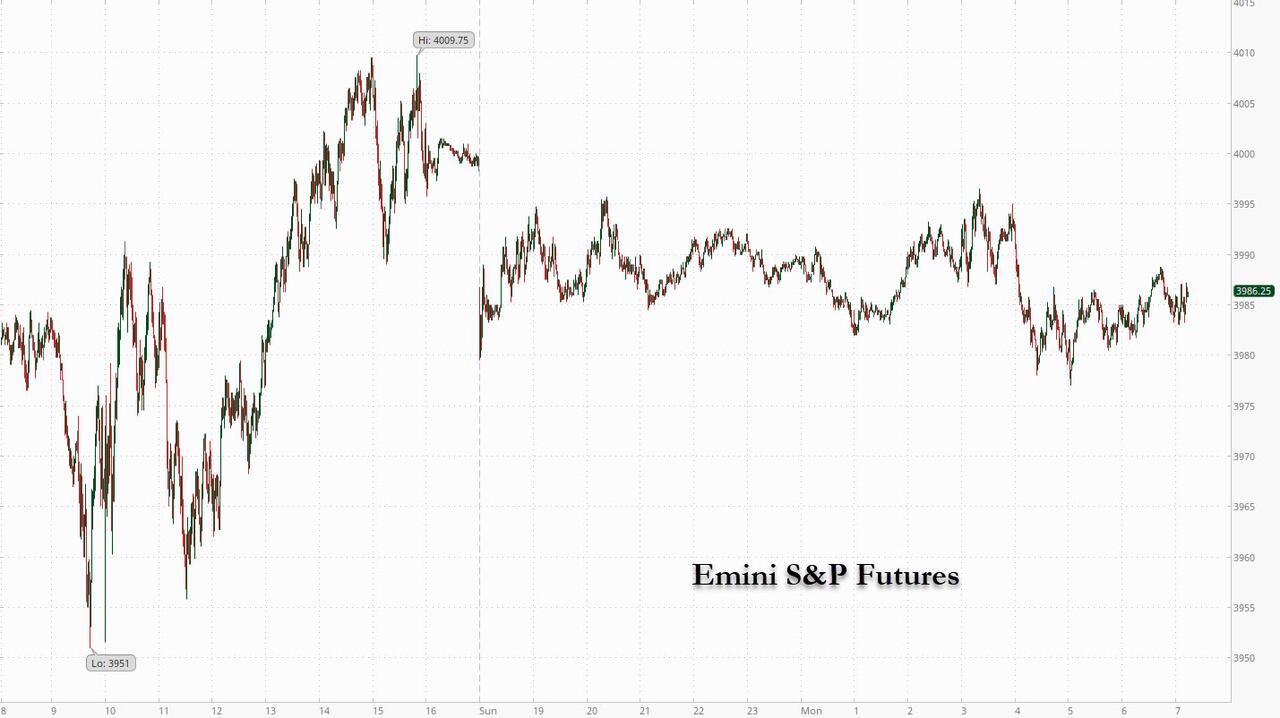

SPX futures rose to 4014.40 in the overnight session. They have since eased back to the flat line. The item du jour is the FOMC report, due to be delivered at 2:00 pm. Investors are not prepared to be disappointed. The Master Cycle high may have been put in on November 15 (day 264). The Cycles Model suggests a strong directional day (trending strength) on Friday. It appears that whether the direction is up or down depends a lot on today’s FOMC performance.

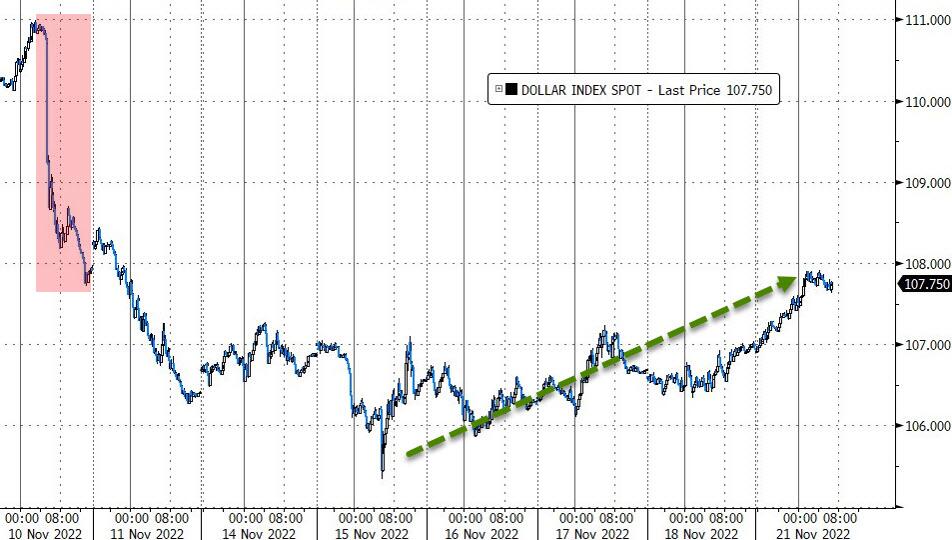

ZeroHedge reports, “US equity futures were steady, trading in a narrow 15 point range before the release of minutes from the latest Fed meeting which may signal that the pace of rate hikes may slow. S&P500 futures up 0.1% by 7:30 a.m. ET, swinging between gains and losses, after the underlying index closed above 4,000 for the first time since Sept. 12 amid lighter trading before Thursday’s Thanksgiving holiday. Nasdaq 100 futures rose 0.1% after the tech-heavy index climbed 1.5% on Tuesday. Credit Suisse shares plunged below their record closing low after the bank warned of a fourth-quarter loss. Oil fell as the EU discussed imposing a price cap on Russian oil between $65 and $70 a barrel (which Russia will never comply with). The Bloomberg dollar index erased earlier declines. Ten-year US Treasury yields rose by one basis point.”

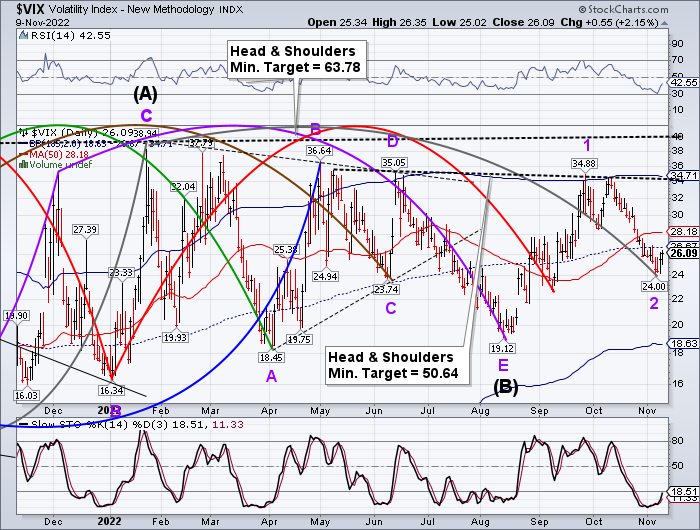

VIX futures remained steady after yesterday’s plunge to a Primary Cycle low. The Cycles Model suggests a strong move is imminent, possibly as early as today.

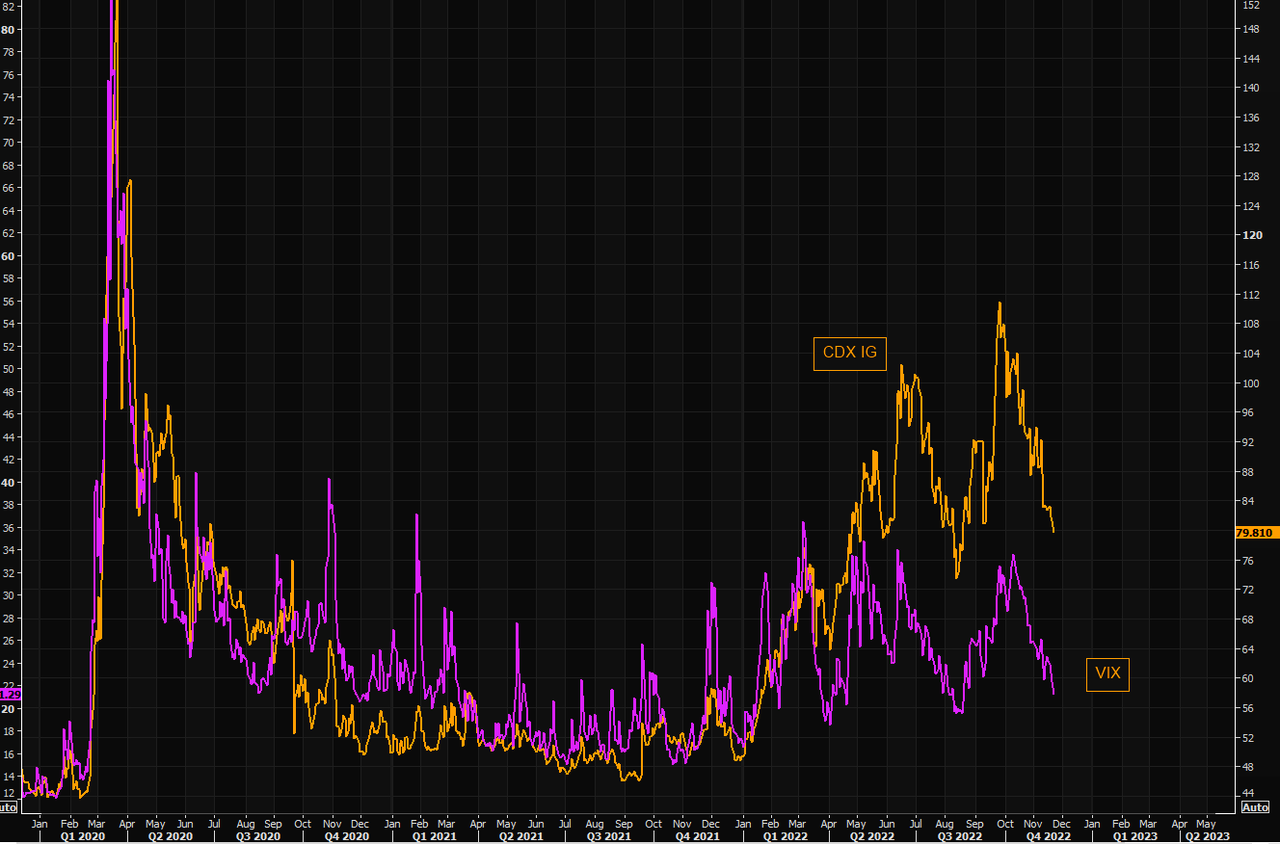

ZeroHedge remarks, “US credit protection puke

CDX IG is printing the lowest levels in a while. The latest move from panic highs is the largest cumulative move lower since credit protection started rising in early 2022.”

Remember this:

“Rule 1. Markets are risky.

Rule 2. Trouble runs in streaks.

Rule 3. Markets have a personality.

Rule 4. Markets mislead.

Rule 5. Market time is relative”

― The (Mis)Behavior of Markets

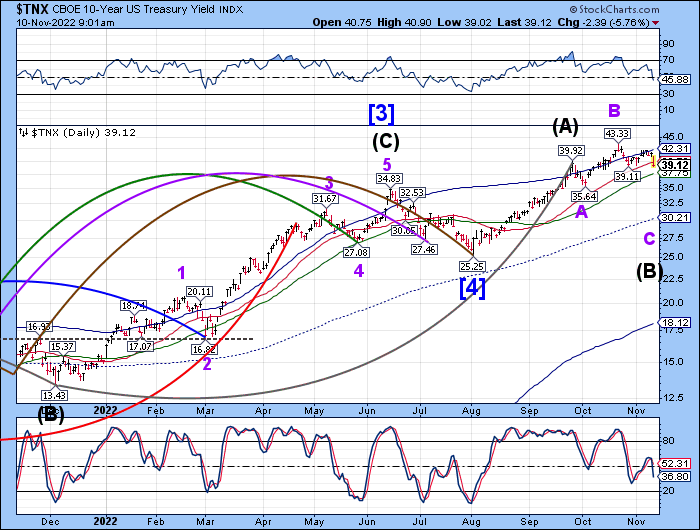

TNX plunged this morning, but failed to make a new low. The Cycles Model suggests a reversal is possible today with yields rising to the first week of January. Stay on the alert.

Yesterday ZeroHedge reported, “After a subpar and tailing 2Y auction and a mediocre and tailing 5Y auction both of which took place on Monday in the holiday-shortened week, moments ago we got the week’s final coupon issuance in the form of $35BN in 7Y paper. It was ugly. In fact, it was almost as ugly as that infamous Feb 2021 7Y auction which sparked a brief selling panic across the Treasury market.

The high yield of 3.890% was below last month’s 4.027%, the first sequential decline in auction yields since July, but more notably it tailed then 3.863% When Issued by 2.7bps. This was the biggest 7Y tail since that infamous Feb 2021 seven year auction which sparked a flash crash across the curve and a mini freak out in the rate market.”

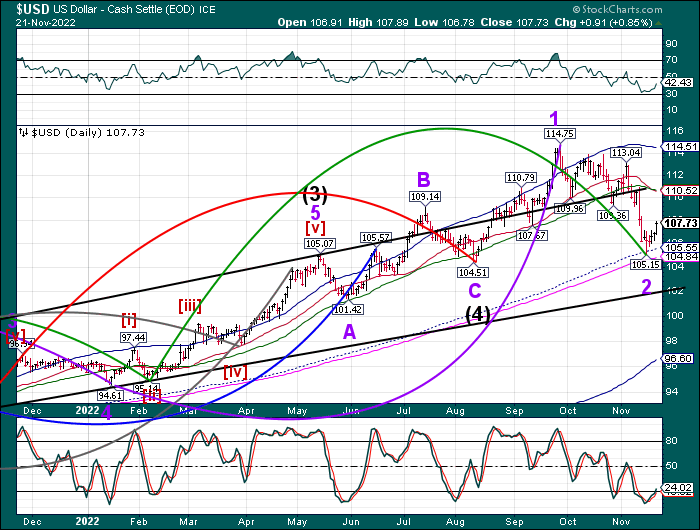

USD futures declined to 106.24 this morning. While the November 15 low may be the Master Cycle low, it is possible for an extension to a newer low this week. There is no buy or sell signal at this time. We await the passage of time to determine the final outcome.

Crude oil futures resumed its decline today, declining to a low of 76.83. The Cycles Model suggests a possible two-week decline that may meet the Cup with Handle target. The 50% retracement of the rally from 2020 is at 68.50, so the Cup with Handle formation is credible. The 61.8% retracement value is at 53.87, not far from the Broadening Wedge target.

ZeroHedge remarks, “Oil prices are tumbling this morning amid Europe’s Russian Oil Price Cap scheme discussions about a price cap between $65 and $70 and rapidly spreading lockdowns across China impacting demand.

“At current price levels, the plan seems ineffective,” PVM Oil Associates analysts Tamas Varga and Stephen Brennock said in a note, referring to the price cap.

“It will be crucial to see the details of the proposed cap to evaluate the price impact.”

Beijing asked residents not to leave the city unless necessary, to stem the spread of the virus.”