11:50 am

The last four months have been a good time to accumulate shares in the Ag Index, whichever fund/ETF you choose. Today we find the index at day 254 of its Master Cycle with firm support at 460.00. A confirmed buy signal awaits above 471.80-474.74, the 50-day Moving Average. Keep in mind that the rally from this low may continue for up to a year or longer.

ZeroHedge reports, “Wheat prices slid Thursday after a United Nations-brokered deal allowing exports of farm goods from Ukraine was extended for 120 days, reported Bloomberg.

The Black Sea Grain Initiative was initially agreed upon in July and ended a five-month Russian blockade of Ukraine’s seaports, allowing millions of tons of farm goods to leave Ukraine — a major ag exporter to the world — to countries across Asia, Europe, and Africa.

“I welcome the agreement by all parties to continue the Black Sea Grain Initiative, “UN Secretary-General Antonio Guterres said in a statement, while Ukraine’s President Volodymyr Zelensky tweeted that Guterres and Turkish President Recep Tayyip Erdogan worked together to extend the deal. He added: “waiting for an official announcement from partners.”

11:14 am

I had always understood that the Crypto sector to be at the outer fringe of speculation and have declined commentary until now. This week’s carnage has confirmed my worst fears that, when this financial crisis is over, people will wish they never heard of Crypto currencies (they’re not a currency) before they put their money at risk. The excitement is now gone and the panic is in full swing. The sad part is that the panic may migrate to other parts of the market.

ZeroHedge observes, “Cryptocurrencies have been on the doldrums since the ‘Crypto Carnage’ of Spring 2021. Over the weekend, a Bahama-based crypto exchange FTX Exchange collapsed. It will probably not be the last one.

Due to the massive financial speculation, induced by the credit (QE) programs of central banks, the crypto market grew into a hub of speculation. During their first global crash in spring 2021, it was rumored that some players had been engaged in speculation with leverage of 100x. That is, by borrowing 100 times the value of the underlying asset (cryptocurrency) and investing it back into the market. I have to admit that I had never heard of anything similar. In standard economic thinking, leverage of 12x was considered extreme. That “rule of thumb” was shattered in the crypto markets.”

10:55 am

BKX is on an aggressive sell signal after an early reversal (day 245) from the mid-Cycle resistance at 110.17. Should this be correct, the Cycles Model infers a decline to the end of the year, with a possible extension to the end of February. Support remains strong at 97.00, but if we have a repeat of the Lehman crisis, the supports may not matter.

3:10 pm

SPX ran up to 3954.00, a 39% retracement of the initial decline. It now may be headed for the trendline and the 100-day Moving Average (not sown) at 3906.00. Should it cross beneath it, we may have a confirmed sell signal.

10:38 am

It’s time for a bounce in the SPX, but I wonder if things could get out of hand at this point, with liquidity in short supply and the Crypto plunge with more losses to come. Normally we might see a short-term bounce up to 4000.00, which would be an ideal point to go/add shorts. But there is so much uncertainty that I personally would simply be short and bear the bounces, if they occur.

ZeroHedge observes, “A few days ago we asked how much longer do we have to wait for the “first-day affidavit” in the FTX bankruptcy, traditionally the most detailed and comprehensive summary of how any given company collapsed into Chapter 11 (and in FTX’s case, Chapter 7 soon, as this will soon become a full-blown liquidation)…

… and this morning we finally got our answer when it hit the docket (22-11068, U.S. Bankruptcy Court for the District of Delaware), almost a full week after FTX filed on Nov 11… and boy is it a doozy.

Because how else would one describe it when FTX’s new CEO and liquidator, John Ray III, who also oversaw the unwinding and liquidation of Enron, admits that “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.”

8:00 am

Good Morning!

NDX futures are lower this morning, reaching a low of 11573.40 after reversing from the 100-day Moving Average on Tuesday. That reversal gave us an aggressive sell signal that is confirmed beneath the 50-day Moving Average at 11442.69. It is due for a 30-calendar day decline that may venture to the Cycle Bottom support at 10287.33, where it meets the trendline starting in 2009. There may be a Santa Rally in the last two week of December, but the decline resumes in January with another 30-day decline, where it may decline beneath 8000.00.

Today’s op-ex is overwhelmingly bullish all the way down to 10650.00. Remember that NDX is the playground for institutional investors. It too them a whole month to go long. QQQ (Closing: $285.44) op-ex, on the other hand, has few calls in today’s op-ex. Short gamma starts at 282.00. Friday’s op-ex shows Mas Pain at 279.00 with huge positions on either side. Long gamma begins at 290.00 and short gamma reigns beneath 275.00.

ZeroHedge comments, “When is it time to short?

The question now is if this is the 8th or the 16th of August – the difference could be monumental for the survival of a short position. The latest data from the various prime brokerage desks we trade with indicates that we are very close to the end of the bounce – and that is what this email examines. From a trading perspective we still would want to see a test of 4100 to get involved in a pure delta 1 short – and are happy for now with our VIX logic from yesterday. There is more often than not a little extra juice left to squeeze in moves like these and we need to be surgical in terms of implementation. Stay tuned.

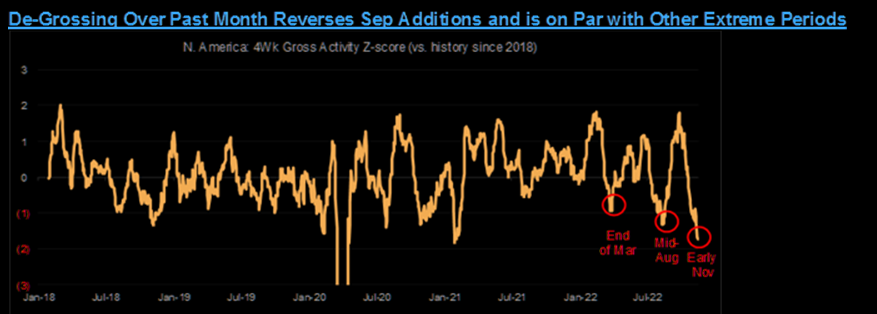

De-grossing done

The excellent “Positioning Intelligence” team at JPM is of the view that the bulk of the de-grossing (especially the type of extreme reductions we’ve seen in the past week) seems likely to be over. The total amount of gross that was added from late Aug to end-Sep appears to be mostly reversed. This is apparent when looking at rolling 4wk gross flows which reached a +2z level in late Sep, but are now approaching a -2z level for a full reversal.”

SPX futures are substantially lower, approaching the 100-day Moving Average at 3906.50. Tuesday’s reversal brought the SPX beneath its 2-hour (short-term trading) Cycle To, giving an aggressive sell signal. The signal remains on the aggressive side until it declines beneath the 100-day for a confirmation. The Cycles Model suggests an approximate 30-calendar day decline that may bring the SPX to or beneath its Cycle Bottom support at 3621.23. Wave [3] may not be complete until early February.

Today’s op-ex shows possible Max Pain at 3955.00. Short gamma begins at 3950.00 with a ramp higher at 3900.00. Long gamma begins at 4000.00.

ZeroHedge reports, “US equity futures dropped to session lows, and surrendered earlier gains of as much as 0.2%, setting up Wall Street stocks to extend Wednesday’s weakness, with traders assessing comments from Fed officials about the path of rate hikes amid earnings reports (such as those from Target) confirming that the US consumer is hunkering down for a recession. S&P 500 futures were 0.8% lower and those on the Nasdaq 100 dropped 0.6% at 7:30 a.m. in New York, with treasury yields bouncing after yesterday’s decline. 10-year Treasury yields rose, following indications from Fed officials on Wednesday that policy would tighten further. The dollar rallied half a percent against a basket of currencies.

VIX futures rose, but still must overcome mid-cycle resistance at 26.56 for a confirmed buy signal. The Cycles Model shows the next Master Cycle high in mid-December.

Next Wednesday’s op-ex shows Max Pain back down to 24.00. Short gamma starts at 22.00-23.00. Long gamma shows call buyers are filtering back in at 27.00 with increasing strength to 60.00.

TNX is rising to test the 50-day Moving Average at 38.29 A move above that level puts TNX on a confirmed buy signal. The Cycles Model shows the 10-year yield rising to the end of the year. The target for Wave [5] may be near 53.16, a peak yield not seen since 2007. Yesterday’s 20-year auction may have marked the bottom in yields for a while.

ZeroHedge reports, “What a difference a month makes: last month, when inflation prints were coming red hot, one couldn’t find a willing buyer for the 20Y auction with a microscope, and as a result we saw a 2.5bps tail, tying the biggest on record. Well, fast forward to today when after two big misses in the form of lower than expected CPI and PPI, we just got the 2nd best 20Y auction on record.

Printing at a high yield of 4.072%, the auction priced not only more than 30bps below October’s 4.395%, the first sequential yield drop since August, but also stopped through the When Issued 4.101 by 2.9bps, which was the second highest stop through on record with just April’s 3.0bps higher.”

WTI futures declined to 83.53, separating itself even further from the 50-day Moving Average at 85.92. It is on a confirmed sell with a potential decline to mid-December. The minimum decline may be to the Cycle Bottom at 76.24. However, it may be just as likely to decline to the lower trendline of the Broadening Wedge at 68.00. Should it go that far, it is likely that the decline may continue through the end of the year.

ZeroHedge observes, “In the past 24 hours, oil traders have received clashing outlooks from two of the market’s leading forecasters — which one is right will determine how prices end this year.

On Monday the OPEC producers’ group once again slashed its forecasts for global oil demand in the fourth quarter, indicating that markets face a supply surplus unless the cartel and its allies implement the output cuts they announced — to much US irritation — last month.

The forecast suggests OPEC+ is likely to continue keeping a tight leash on supplies when it meets on Dec. 4. That would also be consistent with recent comments from Saudi Energy Minister Abdulaziz bin Salman, who said at the COP27 talks in Egypt last week that OPEC+ will remain “cautious.”

Gold futures continued their decline from the potential Master Cycle top made on Tuesday (day 252). Should that be correct, the decline may continue through the month of January. A buying opportunity may re-assert itself by the month of March, per the Cycles Model.