1:46 pm

TNX is still beneath its Cycle Top at 42.22, but received a jolt this afternoon in the form of a “Disastrous 10-Year Auction.” Reception was so poor tat dealers had to take 24% of the offering. They, in turn, will add to the selling, since they do not want to hold such a large supply, which the Fed would normally have taken off their hands.

1:36 pm

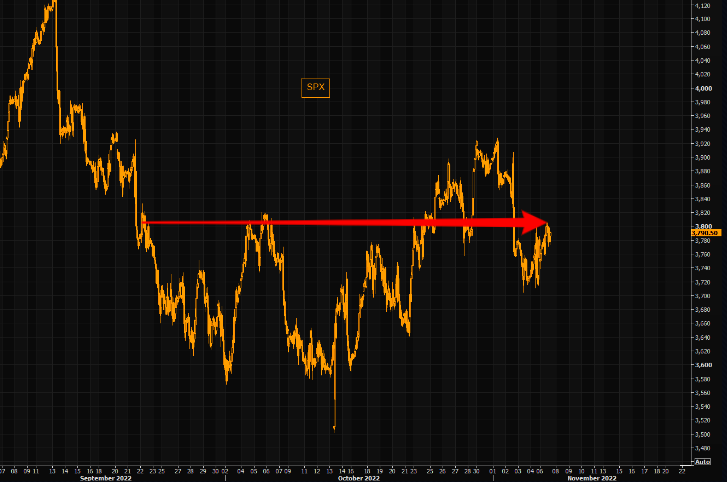

SPX has declined beneath the 50-day Moving Average at 2792.00 and Short-term support at 2882.00, creating a confirmed sell signal. The next level of support is at the mid-Ccle at 3728.88. Take appropriate action.

12:45 pm

NDX has fallen beneath the Li of the Cup with Handle formation, confirming its sell signal. Take appropriate action.

8:00 am

Good Morning!

SPX futures are lower, but have not declined beneath the 50-day Moving Average at 3805.36. The structure appears to be incomplete, so there is a good probability of yet another probe higher. Overhead resistance (100-day MA) is at 3894.72, suggesting only a brief foray above that level. Today is day 258 of the Master Cycle.

Today’s op-ex shows Maximum Pain for options investors at 3820.00. Long gamma comes in at 3855.00, while short gamma prevails beneath 3805.00.

ZeroHedge reports, “Futures and yields are flat, both recovering from a dip earlier in the session, as investors kept an eye on midterm election results ahead of key inflation data later in the week. To the disappointment of bulls, a Red Wave failed to emerge in Congress as voters delivered a mixed verdict in elections shaped by inflation and split around social issues, with Republicans headed toward control of the US House, but by smaller margins than forecast, while the Senate majority remains a toss-up.

Back to markets, where Nasdaq 100 futures were down -0.5%, while S&P 500 futs slipped 0.4% at 7:30 am ET after fluctuating between gains and losses one day after stocks capped a three-day rally.”

VIX futures were rather range bound in the overnight session. Friday’s Master Cycle low at 24.00 remains intact. An aggressive buy is an option here, given the length of the correction. Of course, the buy signal is confirmed above the mis-Cycle resistance at 26.67. Wave 3 should waste little time moving above the Cycle Top resistance at 34.71.

Today’s op-ex sows a battle for supremacy or Max Pain at 25.00, with 3,540 call contracts expiring and 3,960 put contracts expiring. Long gamma begins at 26.00, while short gamma prevails beneath 25.00.

An interesting phenomenon has developed in the VXN, which measures NDX volatility. As we should know, the NDX is interest rate sensitive, which makes the spikes in the VXN problematic. The three largest down-spikes occurred on June 15, September 21 and November 2, 2022. On each of these days the Fed raised interest rates by .75%. Could this be a coincidence, or was there an effort to squash any potential NDX sell-off through the back door (VXN). Those large spikes of selling at the precise hour of the announcements leads me to infer that a very large seller was present to discourage buyers of hedges against a sell-off in the NDX, thereby “calming the markets.”

ZeroHedge comments, “Sharp intra-day falls in the Nasdaq VIX, like those we’ve seen in recent days, have previously been associated with corrections in the Nasdaq 100 itself.

Strange things are afoot in vol world. S&P implied volatility as captured by the VIX has looked low relative to cross-asset volatility, at-the-money volatility and realized volatility for most of this year. This is unexpected given equities are in a protracted bear market. The relative cheapness of deep out-of-the-money puts is perhaps one explanation, as the market believes the Fed’s put is drawing nearer.

Nevertheless, we are also seeing similar patterns in the Nasdaq 100’s version of the VIX, the VXN. It is also very low compared to realized volatility, as well as being close to 15-year lows to at-the-money volatility.”

On top of that, there has been some unusual price action in the VXN in recent days. There has been a cluster of lightning-fast intra-day falls, with an equally sharp rebound straight after. These types of moves are very rare, and they have never been this big, with the low hitting only 20% of the close.”

TNX is higher this morning, but beneath the Cycle Top at 42.22. That resistance may not last, since today may be the first day of a series of “ratchet up” days for the TNX, culminating in a potential Master Cycle high next week.

ZeroHedge reports, “With stocks and gold soaring while the dollar and cryptos plunge in what appears to be an extremely chaotic day for most risk assets as midterms loom, moments ago the Treasury held its first refunding auction when it sold $40BN in 3Y paper at a high yield of 4.605%, the highest yield since Nov 2006 and well above last month’s 4.318%. The auction stopped through the When Issued 4.617% by 1.2bps, the biggest stop through since at least 2016 (and the first non-tail since August).

The bid to cover of 2.568 was virtually unchanged from last month’s 2.567 and came in modestly above the recent average of 2.506.”

USD futures are higher this morning, testing the trading channel trendline near 110.50 and leaving a new Master Cycle low in its wake. It occurred on day 277 of the current Cycle. A breakout above the trendline and the 50-day Moving Average at 111.02 may be imminent, as Trending Strength is about to get a boost. Calls for a weaker USD are premature.

WTI futures have continued their decline to a morning low of 87.14. A confirmed sell awaits beneath the 50-day Moving Average at 85.99. A Master Cycle low awaits in early December, which may offer an opportunity for a long position.

ZeroHedge reports, “Despite ongoing dollar weakness, oil prices tumbled for a second straight day as China Zero-COVID easing hopes faded and the crypto meltdown today appeared to hit ewvery asset class for a period…

“The lack of a concrete timeline or any real details about plans to reopen the Chinese economy and move away from the still very strict and economically crippling restrictions weighed on the energy market into the afternoon,” wrote analysts at Sevens Report Research.

Of course, traders are also waiting for any signals on supply/demand tomorrow with tonight’s API report offering some early insight…”