11:55 am

Last week I had mentioned a final probe lower might be necessary to complete the current Master Cycle. Today it may have arrived with support at 460.00 holding the low on day 258 of the Master Cycle. There is now an opportunity for GKX to rally sharply over the next three weeks with the Lip of the Cup with Handle at 500.00 as a probable target. There is a high probability of an ensuing rally lasting up to 8 months or longer.

ZeroHedge observes, “Grain shippers have been scrambling to consider all their export options in the wake of low water levels on the Mississippi River and its tributaries.

“Because of the low water conditions on the river, which is a major conduit for soybean and grain exports, there are a lot of farmers and a lot of agricultural shippers who are asking themselves, ‘What is my plan B? What is my plan C?’” Mike Steenhoek, executive director of the Soy Transportation Coalition, told FreightWaves. “And that answer is going to be different depending on your region of the country and what that market looks like.”

10:05 am

BKX consolidates beneath its mid-Cycle resistance at 109.86. While most traders consider BKX may be in a (short-term) uptrend, it is hovering just above its 50-day Moving Average at 102.50 where the (aggressive) sell signal is confirmed. The Cycles Model suggests a continued decline through the end of the year. While there is commentary about the illiquidity of the market, investors and speculators may not know just how close we are to the brink. In the meantime, (down) tending strength may be given a boost this week.

ZeroHedge comments, “While many market participants are concerned about rate increases, they appear to be ignoring the largest risk: the potential for a massive liquidity drain in 2023.

Even though December is almost here, central banks’ balance sheets have hardly, if at all, decreased. Rather than real sales, a weaker currency and the price of the accumulated bonds account for the majority of the fall in the balance sheets of the major central banks.

In the context of governments deficits that are hardly declining and, in some cases, increasing, investors must take into account the danger of a significant reduction in the balance sheets of central banks. Both the quantitative tightening of central banks and the refinancing of government deficits, albeit at higher costs, will drain liquidity from the markets. This inevitably causes the global liquidity spectrum to contract far more than the headline amount.

Liquidity drains have a dividing effect in the same way that liquidity injections have an obvious multiplier effect in the transmission mechanism of monetary policy. A central bank’s balance sheet increased by one unit of currency in assets multiplies at least five times in the transmission mechanism. Do the calculations now on the way out, but keep in mind that government expenditure will be financed.”

8:45 am

Good Morning!

SPX futures sank to a morning low of 3941.60 before a bounce. It remains on an aggressive sell after the Master Cycle high on Tuesday, having spent 264 calendar days in that Cycle. The Sell signal is confirmed beneath the 100-day Moving Average at 3908.49. The Model suggests a decline through mid-December in which the Cycle Bottom at 3520.54 may be taken out.

The options page is currently unavailable through Schwab.com.

ZeroHedge reports, “After opening modestly in the green, US equity futures have drifted steadily lower all session and were last trading near their Monday lows as concerns that China may tighten Covid curbs after China reported its first Covid-related death in almost six months and a city near Beijing rumored to be a test case for dropping all curbs enforced a slew of restrictions all weighed on growth in the world’s second-largest economy, as well as the ongoing carnage in the crypto space. At 7:30am ET, S&P futures were down 0.5% to 3,953 while Nasdaq 100 futures slumped 0.9% to session lows, below 11,600. The dollar stormed higher as investors sought shelter in the dollar; 10Y yields rose to 3.83%, while bitcoin traded around $16,000 after dumping over the weekend. Oil dipped but rebounded from session lows on concern of a weakening demand outlook from China and following a $10 price target cut to $100 for Q4 2022 from Goldman overnight.”

VIX futures are trading at the upper range of Friday’s trading, but no new high to report. VIX’s problem is the huge number of Zero Day to Expiry (ODTE) trading which magnifies short term moves, but is not reflected in the VIX, which usually measures options expiring 30 days out. Two possible scenarios may flip the VIX in a very big way. First, a solid week of back-to-back declines may change the day-trader behavior pattern. Second, should SPX decline beneath the Lip of the Cup with Handle formation, it may send a strong signal that the bear market is not over. At the moment, investors are still holding out hope for a pause/pivot to end the agony of higher interest rates. The Cycles Model suggests a strengthening (up) trend starting this week.

ZeroHedge observes, “In recent weeks there has been much discussion of the unprecedented explosion in 0DTE (0-days to expiry), or options with less than 24 hours to maturity, which have become an extremely levered way to bet on even the smallest market gyrations (of course, the past month has seen some very major market gyrations, so imagine those magnified by 100x or more when it comes to P&L impact).

Just last week we quoted Goldman’s derivative strategist Rocky Fishman explaining that “the strongest area of volume growth has been ultra-short-dated” options, and that “measured in notional volume terms, S&P options with less than 24 hours to maturity now represent 44% of the index’s trading volume, and have been averaging $470BN notional per day over the past month.”

TNX has been consolidating beneath the 50-day Moving Average this morning. However, the Cycles Model suggests a burst of trending strength starting in the next day or so. It also shows the uptrend may continue through early January.

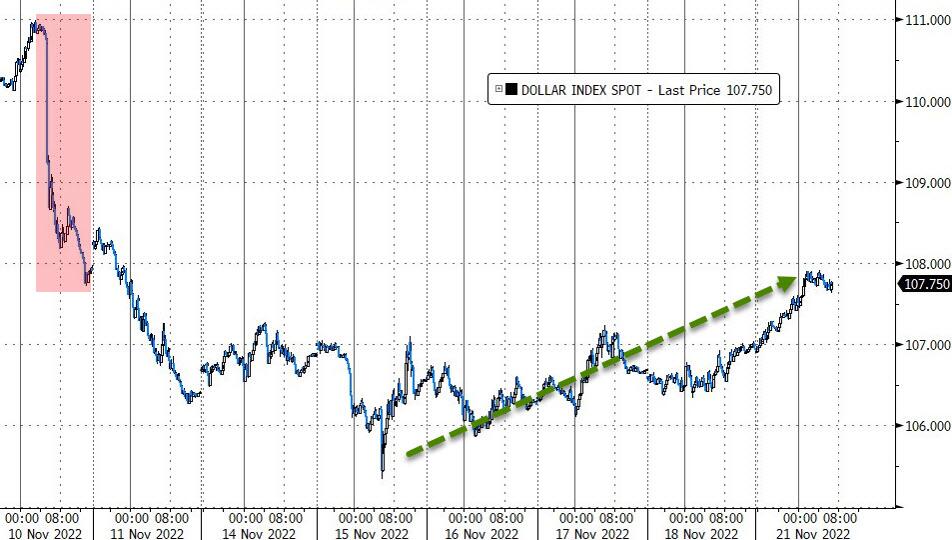

USD futures rose to 107.82 this morning on Day 259 of the Master Cycle. I have marked November 15 as the low, but there is a distinct probability of a deeper low in the next week. There is no buy signal at this time, but it may be considered should USD test the 200-day Moving Average at 104.78. We may see trending strength return to the USD during the week following Thanksgiving.

11:10 am

ZeroHedge explains, “US equity markets are chopping around wildly in the last few days as Nomura’s Charlie McElligott notes that risk is drifting on a mini “triple whammy” causing a modest reversal stronger in the USD (after the post-CPI puke)…

1) China’s again-devolving COVID outbreak (Beijing reported 3 COVID-related deaths, Guangzhou imposed a 5-day lockdown, Hong Kong’s CEO tested positive for COVID, and Shijiazhuang–the 11m population city profiled by the FT last week as a potential “test case” for re-opening–instituted lockdowns and mass PCR testing—h/t AK),

2) the ultimate arrival of cold European weather finally seeing first drawdowns of Gas reserves and

3) a raft of better US economic data late last week (Bloomberg US Eco Surprise Index at best levels since May) is flowing-through financial markets via suddenly-squeezing US Dollar.

Bloomberg Dollar Index has now bounced more than 2% off the three month low made last week, which sits at the root of the overnight risk-asset pullback to start the holiday-shortened US trading week.”

WTI futures are making new lows as I write, currently at 76.44 and falling… The Cycles Model suggests a possible double bottom in December. Meanwhile the decline may be strengthening as a breakdown may occur imminently with WTI trading beneath its Cycle Bottom at 75.86.

ZeroHedge observes, “The first question that comes to mind (as oil already tests multi-month lows) is – why would they do this?

The Wall Street Journal reports that Saudi Arabia and other OPEC oil producers are discussing an output increase, the group’s delegates said…

An increase of up to 500,000 barrels a day is now under discussion for OPEC+’s Dec. 4 meeting, delegates said.

The move would come a day before the European Union has said it would impose an embargo on Russian oil and the Group of Seven wealthy nations’ plans to launch a price cap on Russian crude sales, potentially taking petroleum supplies off the market.

Any output increase would mark a partial reversal of a controversial decision last month to cut production by 2 million barrels a day at the most recent meeting.

The reaction was swift and obvious as WTI tumbled $2 back to a %77 handle…”