The Lord’s Prayer

Our Father, who art in heaven, hallowed be thy name. Thy Kingdom come, Thy Will be done, on earth as it is in heaven. Give us this day our daily bread and forgive us our trespasses, as we forgive those who trespass against us. And lead us not into temptation, but deliver us from evil. Amen.

10:35

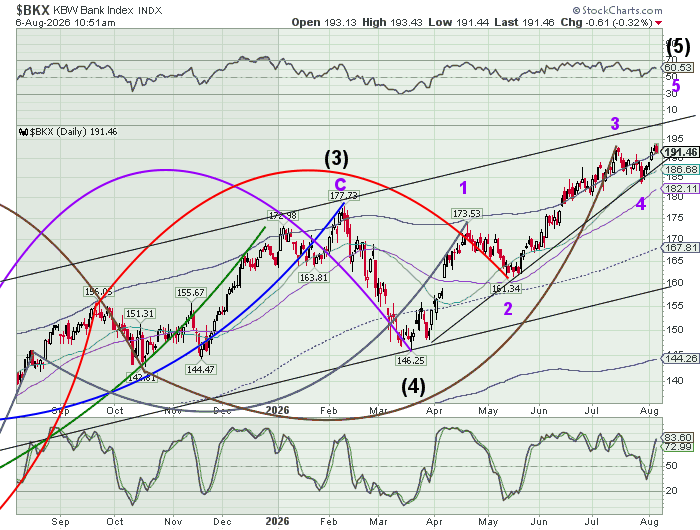

The Ba The Banking Index has just made a new all-time high. The Cycles Model may allow the rally to continue to the end of the month. However, there is a strong resistance at the upper trendline near 200.00.

The Banking Index has just made a new all-time high. The Cycles Model may allow the rally to continue to the end of the month. However, there is a strong resistance at the upper trendline near 200.00.

8:00 am

Good Morning!

SPX futures consolidated above the Cycle Top support/resistanceline at 7721.64. SPX has exceeded its initial target and is now attempteing to go higher. Although it may do so, it is in a corrective phase which allows it to decline to the 52-day Moving Average at 7482.90 in the next couple of days. Options markets show investors have quit buying puts and are scrambling for calls.

ZeroHedge reports, “US futures are mixed with S&P futures modestly higher offset by a slide in tech: as of 8:00am ET, S&P futures are up 0.1% while Nasdaq futures drop 0.5%, hit by a plunge in Sandisk (down 9% in pre-market), and rival Western Digital which tumbled 15%, after both companies reported earnings.”

NDX futures have declined beneath the 52-day Moving Average at 29388.13 this morning. Should it break beneath it Intermediate support at 29150.00, it may decline further, possibly beneath 28000.00. Shorts are still holding seay with the NDX, but it may not last. The NDX has made an impressive recovery thus far, but Korea’s AI sector is still underwater. Once a new support has been found, short covering may take the NDX to impressive new highs.

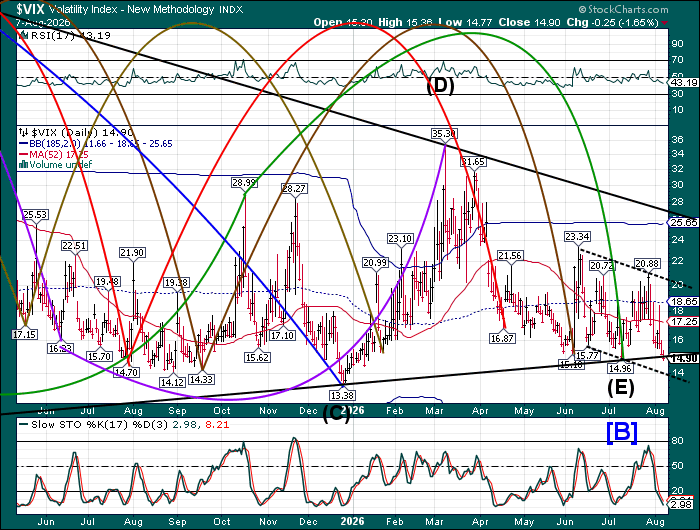

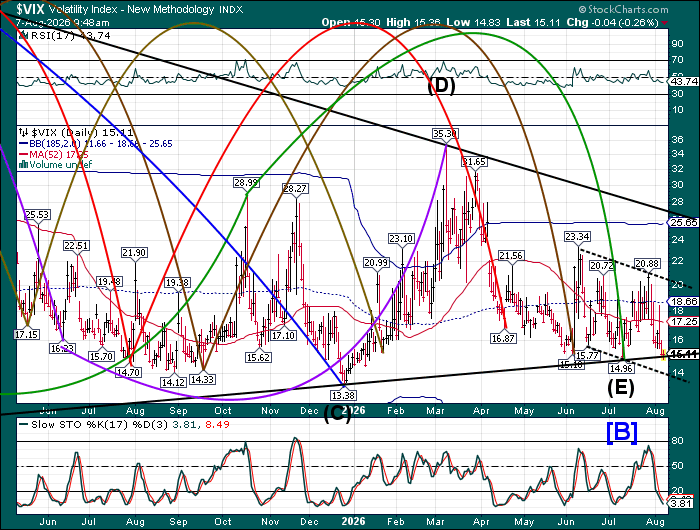

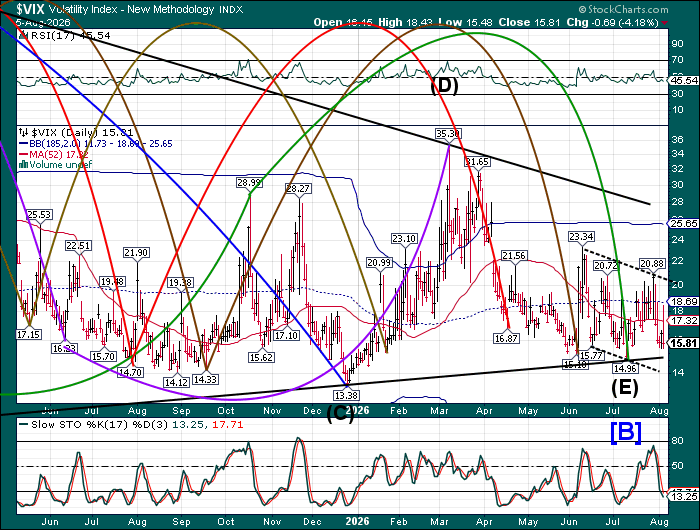

The premarket VIX is consolidating near its low. It may stay in the current trading range for a couple of days, but the downside track is incomlete and a “tail” should develop soon beneath the Triangle formation.

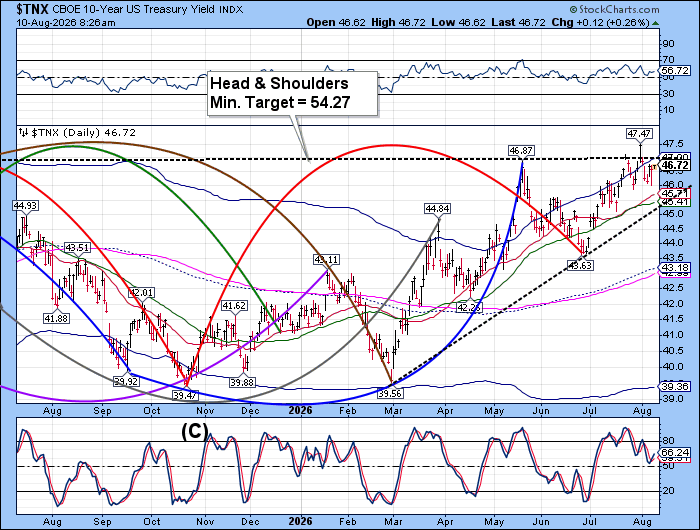

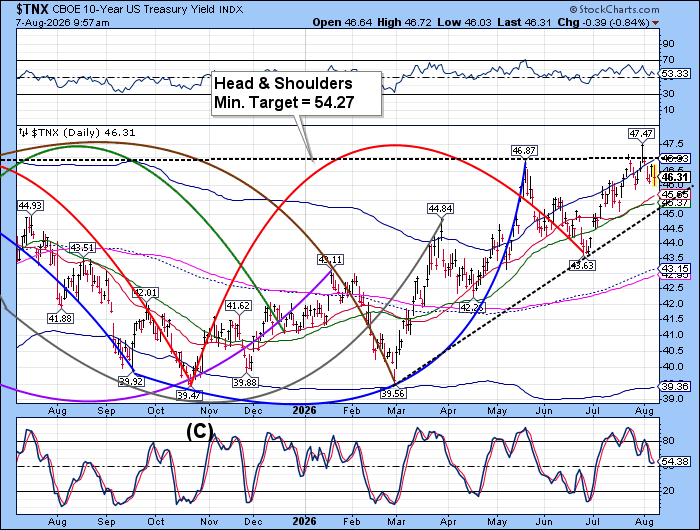

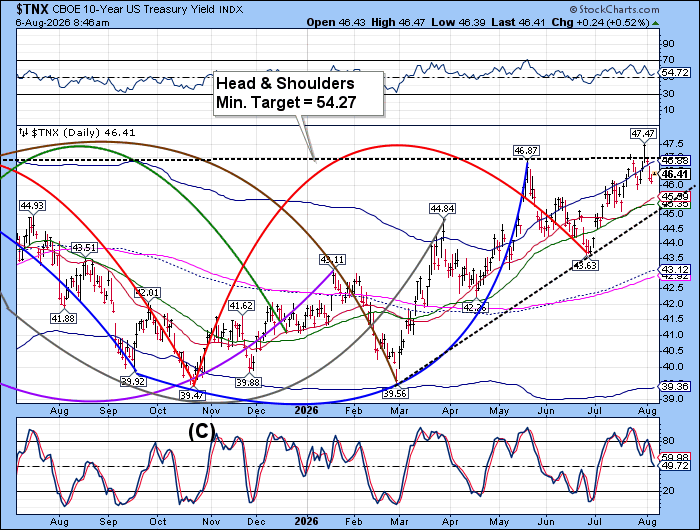

The US 10-year Bond Yield has bounced, but may be repelled by short-term resistance. If so, TNX may decline further to it 52-day Moving Average at 45.30. However, the Cycles Model suggests Trending Strength may return over the weekend. It is possible that T”NX may emerge above its Head & shoulders neckline next week, activating its target mechanism by early September.

ZeroHedge comments, “For yet another quarter, the Treasury’s Quarterly Refunding offered no surprises, which considering the state of the US bond market is probably not a bad thing.”

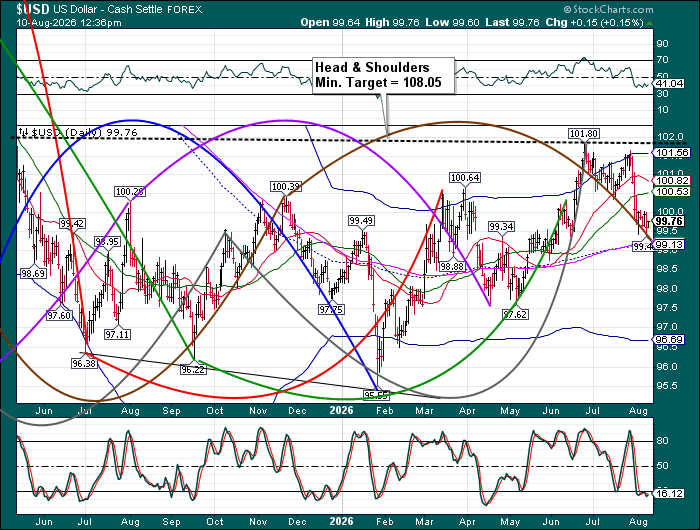

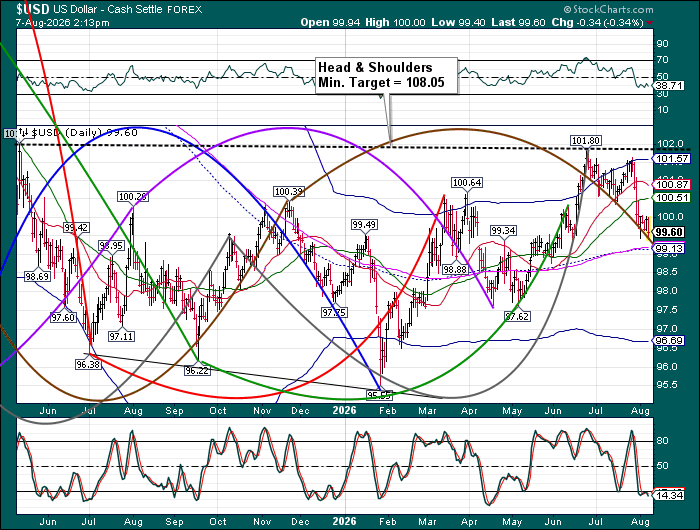

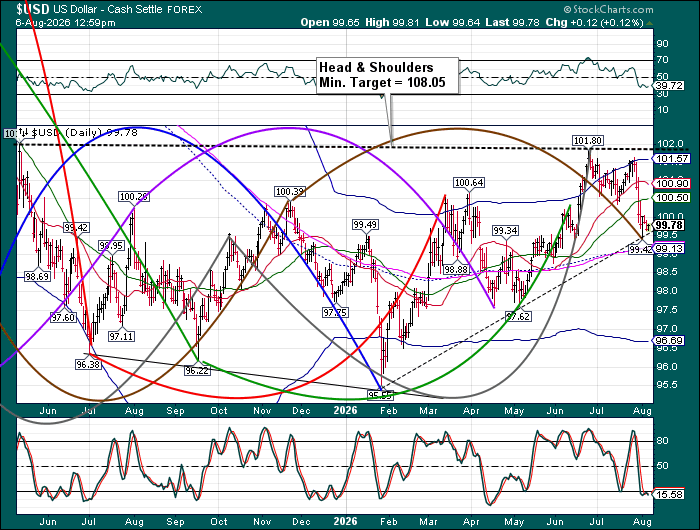

The US Dollar may have emerged from a retest of its uptrend line near 99.50 and may be ready to show strength in its move higher. The Cycles Model suggests a particularly long-lived uptrend may have befun, fueled by the Dollar shorts.

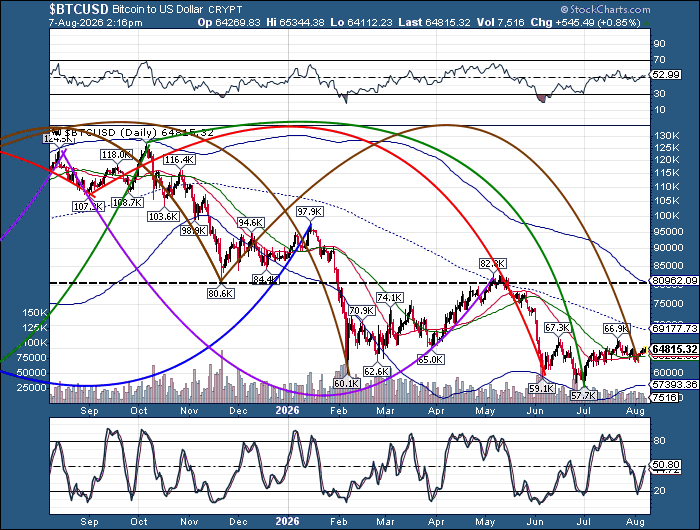

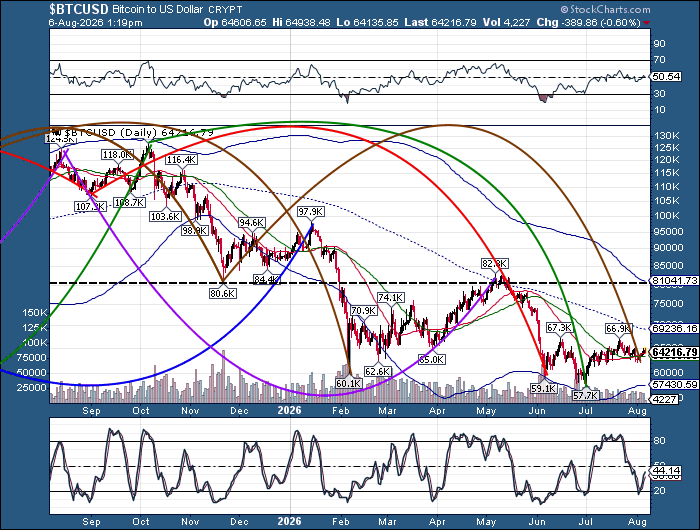

Bitcoin is tentatively emerging from a Poaaible Master Cycle low at the 52-day Moving Average. It may have made an aggressive buy signal, but confirmation comes above the mid-Cycle resistance at 69236.00. Demand for bitxoin may be coming from Japan and Europe, both of which are showing signs of crisis. The new uptrend may last to the end of September.

ZeroHedge muses, “Looks like $100,000 bitcoin may be on deck, because Cramer is selling.”

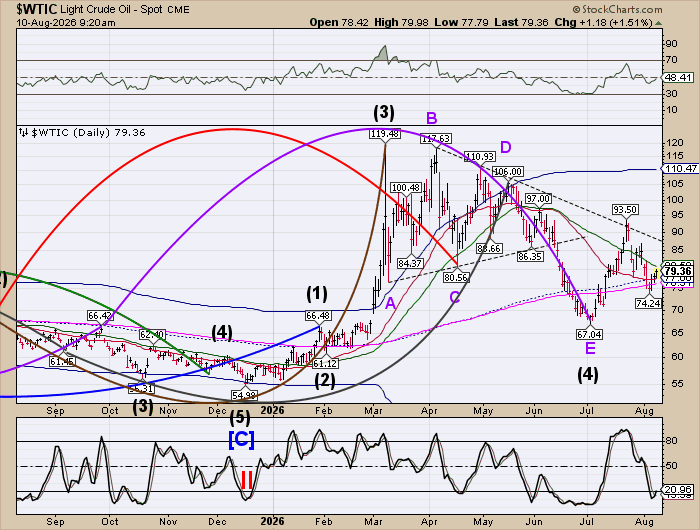

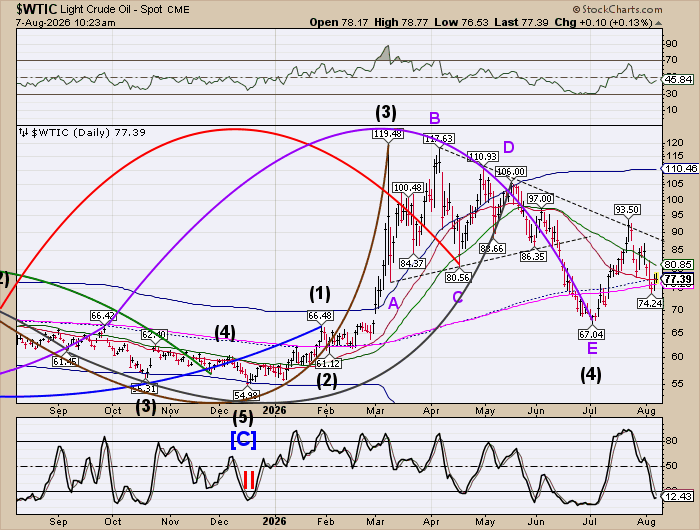

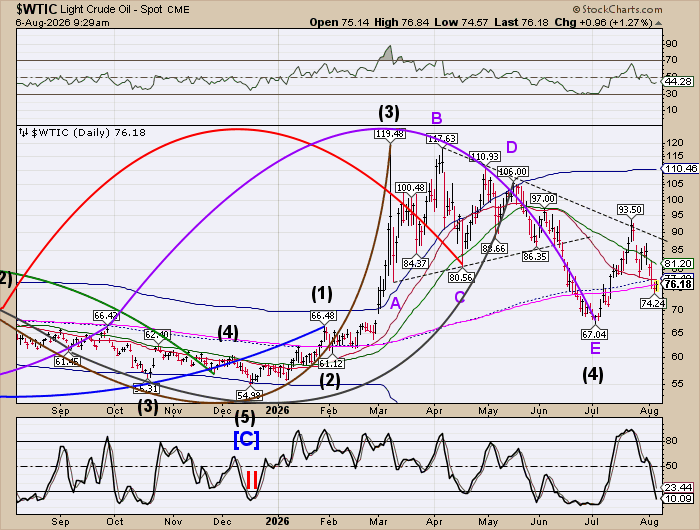

Crude oil has bounced toward Intermediate resistance at 77.23 this morning. However, the Fractal structure may be incomplete, leaving yet another probe lower. A possible floor may be found at round number support at 70.00. The Cycles Model suggests the eversal may arrive in the next week.

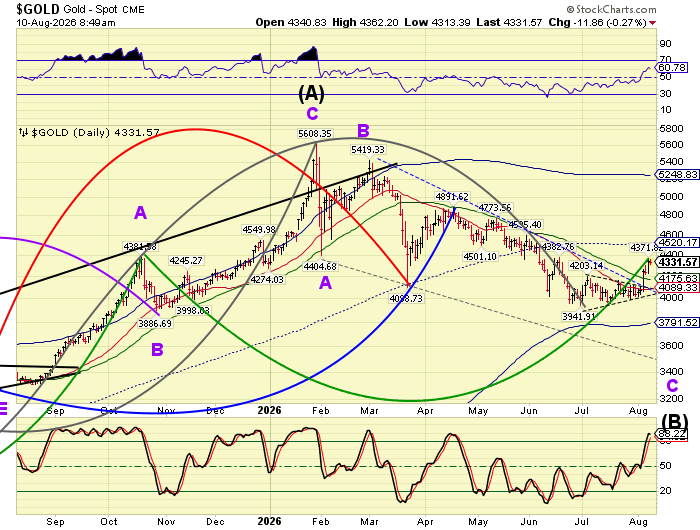

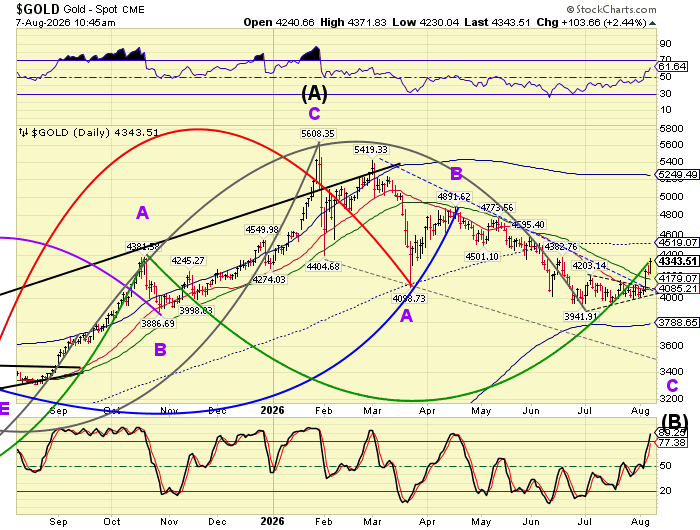

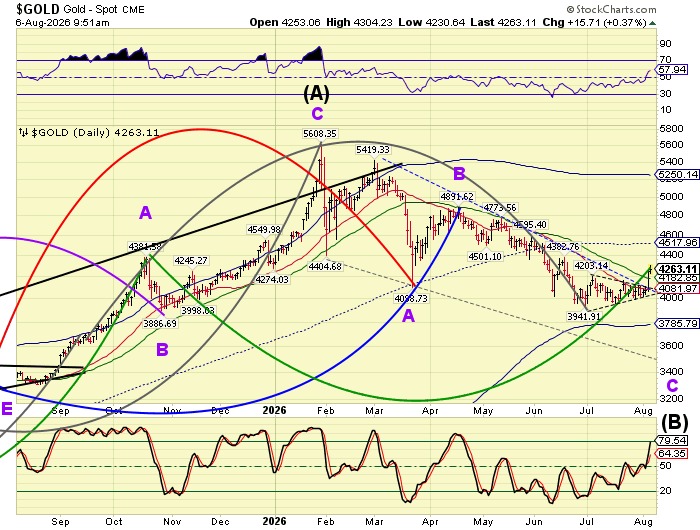

Gold may be finalizing a very stretched Master Cycle today, as the gold bulls emerge from hiding. On Tuesday I mused that, “A brief probe above the Triangle is possible…” Well, there it is. The Cycles Model calls for a decline to mid-September. A sell signal may be offered beneath the 52-day Moving Average. Thetarget for this decline may be near the lower trading channel trendline at 3500.00. However, it may go deeper than some people project.

ZeroHedge opines, “On July 27th, 2026, I penned an article proclaiming, “Gold may have just bottomed.”

I missed the exact lows by a few days, but the charts are signaling that the lows are in. What I’m about to show you are some of the most bullish charts in the markets today.”

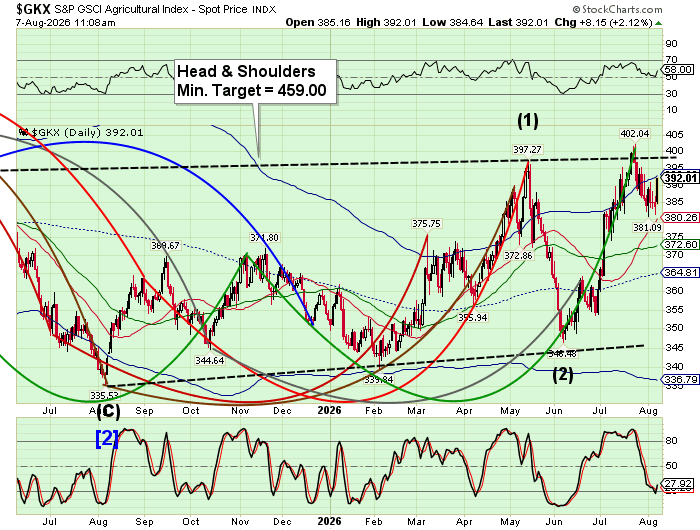

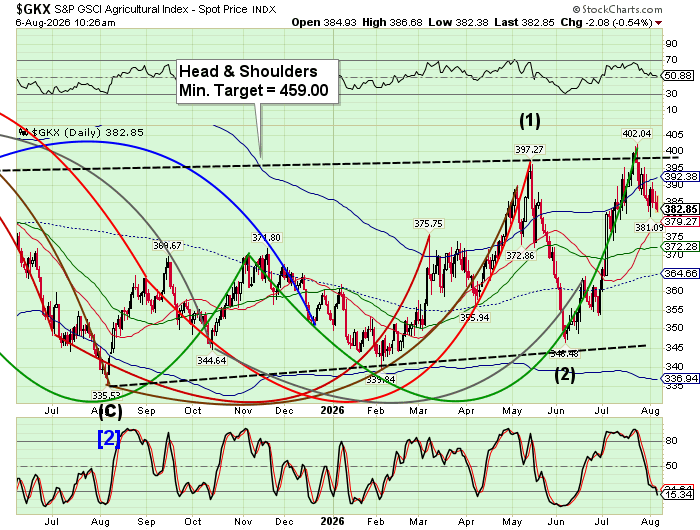

The Agriculture Index may have just completed its minimum retracement from its July 24th high. Should that be so, it may probe back above the Head & shoulders neckline, activating that formation. The alternate view may be another week of decline to the 52-day Moving Average at 372.28. The Cycles Model reveals a possible burst of strength over the weekend that may favor the first option.

ZeroHedge observes, “UBS analysts identified five long-term forces likely to keep global food inflation “structurally higher” above its pre-pandemic average of about 2.5%, crushing consumer hopes that price pressures will simply fade.

“While food inflation globally has fallen from the COVID peak, a new debate is emerging: is the c2.5% LT average obsolete?” London-based managing director and equity-research analyst Sreedhar Mahamkali asked in a note penned on Monday.”