8:10 am

Good Morning!

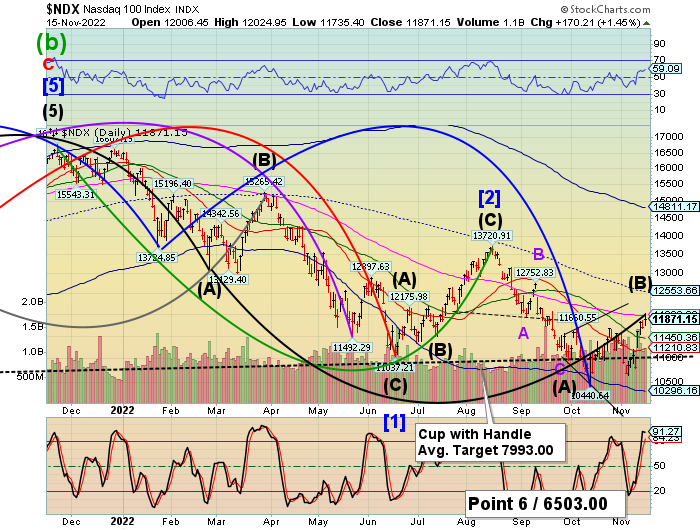

NDX futures bounced to 11923.00 in the overnight market, 50 points shy of the 100-day Moving Average at 11983.82. Since then it has eased lower, but not to new lows. Yesterday it rose to challenge the 100-day, but fell back at the close. The total retracement was 48.3%, a far cry from retracements made just a year ago. Yesterday was day 261 of an average 258-day Master Cycle.

Today’s op-ex shows Maximum Pain for options investors at 11875.00. Long gamma begins at 11900.00, while short gamma resides at 11840.00. QQQ (close 289.39) shows Max Pain at 289.00. Long gamma begins at 290.00, while short gamma may start at 288.00. QQQ options are tightly packed, with the slightest move in either direction starting a potential firestorm of buying/selling.

ZeroHedge remarks, “Remember when we warned that it’s not inflation that will force the Fed to do a 180, but that there is only so much record US Dollar strength the world can tolerate before a pivot is imposed?

We were right… and while this has yet to manifest in official central bank memoranda and bulletins, it has already swept across markets like wildfire.

In our market wrap from yesterday, we showed a stunning chart from Morgan Stanley according to which high-momentum L/S funds had just suffered their 2nd worst 2-Day drop in the past 20 years.”

SPX futures bounced around within the mid-range of yesterday’s trades. Yesterday may have seen the Master Cycle high at 4028.84, a near miss to the mid-Cycle resistance at 4044.33, giving a 64.4% retracement. While the retracement has overshot the proposed 61.8% retracement level, yesterday’s spike high did more to investors’ nerves, urging weak hands to capitulate. Should it be underway, the new Master Cycle may last until mid-December with a likely test of the low.

Today’s op-ex shows Maximum Pain at 3970.00. Long gamma begins at 4000.00, while short gamma may begin between 3925.00 and 3950.00. SPY (close: 398.49) shows Max Pain at 399.00. Long gamma starts at 400.00, while short gamma begins at 398.00, a very tight spread.

ZeroHedge reports, “US equity futures were flat, having traded in a narrow range on either side of unchanged, as investors braced for the latest retail sales data, assessed the easing path of inflation and remained calm in the face of rising geopolitical concerns resulting from a NATO attempt to paint rocket a Ukraine strike on a Polish village as Russian, in hopes of dramatically escalating the war.

Luckily, video evidence refuted the false flag, and overnight NATO was forced to admit that the “:Explosion in Poland was Likely Due to Ukraine Air Defense” Even so, the Western pro-war alliance still blamed Russia with NATO’s Secretary General saying the blast in Poland was likely caused by a Ukrainian air defence missile but that Russia was ultimately responsible because it started the war. “They are responsible for the war that has caused this situation.” Propaganda aside, fears of an immediate spillover from the conflict were soothed, knocking the yen and dollar lower, as demand for safe-haven assets gradually faded.”

VIX futures consolidates between 23.99 and 24.61, awaiting further developments. Having made a Trading Cycle low, the next hurdle to overcome is mid-Cycle resistance at 26.59. The December master Cycle high in the VIX comes a week later than the projected Master Cycle low in the SPX. It will be interesting to see which index dominates.

ZeroHedge remarks, “We are considering VIX hedges for the first time since August

Everything that is “protection” has come down hard and we are starting to get interested. To go outright short cash equities here is not a trade for us – we would want to see an attack and possible overshoot of the 4100 level – but volatility is different. Let’s examine.

Put puke – getting there

Never buy protection when you must, buy it when you can. We are getting closer…”

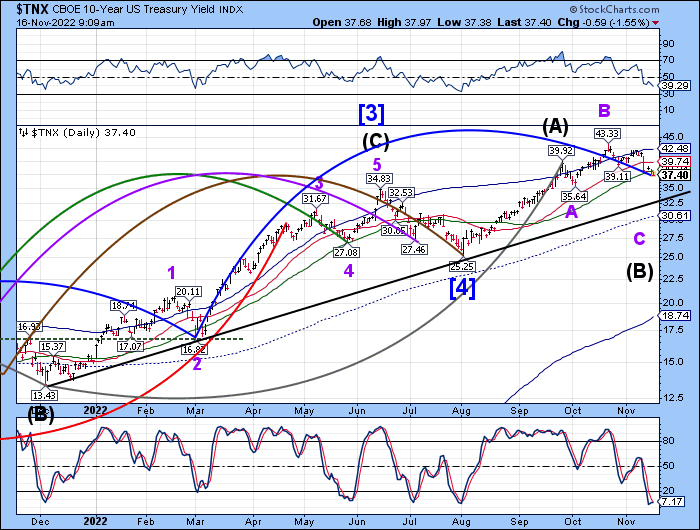

TNX is making new lows this morning as it completes the final probe of the correction on day 260 of the current Master Cycle. Should the reversal take place today, we may see rising rates through the end of the year, according to the Cycles Model. Not a happy thought…

1:30 pm

ZeroHedge reports, “What a difference a month makes: last month, when inflation prints were coming red hot, one couldn’t find a willing buyer for the 20Y auction with a microscope, and as a result we saw a 2.5bps tail, tying the biggest on record. Well, fast forward to today when after two big misses in the form of lower than expected CPI and PPI, we just got the 2nd best 20Y auction on record.

Printing at a high yield of 4.072%, the auction priced not only more than 30bps below October’s 4.395%, the first sequential yield drop since August, but also stopped through the When Issued 4.101 by 2.9bps, which was the second highest stop through on record with just April’s 3.0bps higher.

The bid to cover of 2.64 was also very solid, printing above last month’s 2.50% and above the six-auction average of 2.53%.

The internals were also stellar, with Indirects taking down 75.3%, the third highest on record, and well above the 70.3% recent average; and with Directs taking down 15.4%, below the 17.6% recent average, that left Dealers holding 9.2%, the lowest since September and well below the recent average of 12.1%.”