1:40 pm

Time is the essence of Cycles. In this case, 21.5 market days have elapsed from the October 13 low in the SPX. This is a typical retracement time. In addition, the Wave structure may be complete. There may not be much of a sell signal today, other than those two items. Typically we would wait for the crossing of an important support. The Cycle Top in the 2-hour is at 3934.65. It may not be breached today. Most investors are bullish again…

Wrong-headedness has captured the market again.

RealInvestmentAdvice cautions, “Since June, the market rallied on hopes of a “policy pivot” by the Federal Reserve. However, those hopes got dashed each time as Jerome Powell clarified that the “inflation fight” remained the primary focus. Mr. Powell made that point very clear following the latest FOMC announcement.

“The question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restrictive.”

Before the pandemic, the Fed’s storyline was to let inflation run hot rather than allow inflation to stay too low for too long. Such makes sense as inflation is easy to deal with by hiking rates and slowing the economy. Deflation is a far different story, as it becomes an entrenched psychological impact that becomes difficult to dislodge.

Today, Powell says the Fed’s concern is entrenched inflation which causes pain to the economy.

The reality is that inflation is not the problem.”

8:00 am

Good Morning!

The stock market is open today (Veteran’s Day), but the bond market is closed for the day.

SPX futures reached an overnight high of 3990.10 as it potentially aims for the 61.8% retracement value at 4008.00. Yesterday was the culmination of a triple boost of trending strength as SPX completes its retracement rally. Today is day 260.00 of the Master Cycle and SPX will have achieved 21 market days of rally from the October 13 low today.

In today’s op-ex, Maximum Pain for options investors appears at 3925.00. The options market is hotly contested in both directions with long gamma starting at 3975 and short gamma at 3880.00.

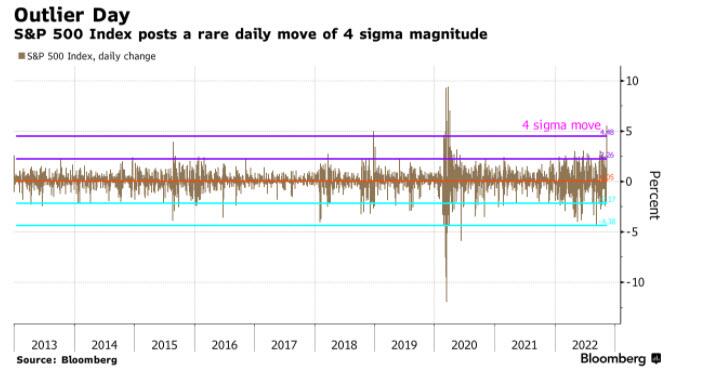

ZeroHedge reports, “One day after its best day since April 2020, when the S&P500 added 5.5%, or a near-record $1.8 trillion in market cap in one day, a rare 4-sigma move that has only occurred 10 times over the past decade, which essentially showed how wrong-footed the market was ahead of the inflation surprise.…

… the index was set to extend its gains as a FOMO panic started to spread among traders fueled by a softer-than-expected US inflation print and as China reduced the amount of time travelers and close contacts of virus cases must spend in quarantine, and pulled back on testing, in a significant calibration of the Covid Zero policy that has upended the world’s second-largest economy and raised public ire.

Contracts on the US stock benchmark advanced 0.3% to 3,974 at 730 a.m. in New York, having earlier risen as high as 3,997. Nasdaq 100 futures also gained 0.7%, while Treasury futures weakened, with the cash market closed for the Veteran’s Day holiday. Commodities also rallied while the dollar retreated for a second day.”

VIX futures rattled around between 23.50 and 23.91 as it consolidates on day 30 of the Master Cycle. Further investigation shows that the September 28 high may have been 34.13, allowing the October 12 high at 34.53 as the top of the Master Cycle. What tipped me off was the completion of a zig-zag decline yesterday, making it a corrective decline. This allows a potential 5-week rally to a mid-December high.

Next Wednesday’s options expiration show that it has change to overwhelmingly short beneath 30.00. Time for a reversal?

TNX cash market is closed today. However TNX futures continue to decline toward the 50-day Moving Average at 37.75. Commentators are gushing about the 4-sigma event that happened yesterday, not recalling that this is still a bear market correction.

ZeroHedge reports the turnabout in bonds. “One day after the ugliest 10Y auction in a long time, which tailed the most in 6 years, today we got a mirror-image, when moments ago the Treasury sold the final refunding auction of the week when it placed $21 billion in 30 year paper (Cusip TL2) at a high yield of 4.080%. While this was the highest yield since July 2011 and was well above last month’s 3.930%, the auction stopped through the When Issued 4.113% by 3.3bps. This was the biggest stop through since at least 2016 so yes, a mirror image of yesterday’s tailing 10Y which also was a six-year outlier, only in the opposite side as it tailed by a similar amount.

The bid to cover of 2.422 was well above last month’s 2.386 and was also the highest since July.”

USD futures made a new corrective low at 106.60.