1:40 pm

Here’s some advance notice on SPX. It has been testing the 2-month tendline for the past week and may be about to trigger an aggressive sell signal. The trendline lies at 4550.00 and is likely to be broken at the FOMC announcement. Remember, this is still an aggressive call. Most traders only recognize the 50-day Moving Average which, when broken, may provide a confirmed sell signal. I am announcing the aggressive signals coupled with the Cycle reversals, giving a higher degree of certainty and a wider trading range which may be more profitable.

10:20 am

The Ag Index may have made its master Cycle high yesterday, on day 265. What may come next s a 4-week decline to the 61.8% retracement at 387.76 or a possible extension to its 2021 low at 380.54. Despite supply and demand fundamentals, the decline may have more to do with a sudden drop in liquidity.

ZeroHedge notes, “On Monday, orange juice futures rocketed to an all-time high due to global supply concerns among agricultural traders. The citrus greening disease continues to affect Florida and is spreading in Brazil — both regions are top producers, and a potential production loss from these areas could significantly tighten global supplies. ”

ZeroHedge points out, “The decision by India to ban certain rice exports has sparked panic buying at supermarkets across the US. Videos circulating on social media show the staple food is flying off the shelves as high demand depletes supplies amid concerns of a global shortage. Some supermarkets have responded by implementing purchase limits, while others have hiked prices. The scenes below should remind readers of the panic buying days during Covid. ”

9:41 am

BKX may continue its probe to the neckline at 93.00 today on day 257 of the Master Cycle. While the Master Cycle may be ending, there appears to be some unfinished business in the Wave structure. Completion may come with a probe to the neckline.

ZeroHedge announced, “Update (16:40 ET) : as leaked earlier by the WSJ, shortly after the close, PacWest Bancorp confirmed that it is merging with smaller rival Banc of California, in what is effectively a take under.

The banks said in a statement that Warburg Pincus and Centerbridge Partners would invest $400 million of new equity as part of the deal. The banks will sell assets with the aim of repaying $13 billion of wholesale borrowings, the companies said Tuesday.

PacWest stockholders will get 0.6569 of a share of Banc of California common stock for each of their shares. While PACW remains halted after hours, BANC shares are now trading at 14.75, suggesting that PACW stock will trade around just around $9 when it reopens at 5pm ET.”

8:00 am

Good Morning!

NDX futures are down this morning to a low of 15503.50, after testing support/resistance at 15566.04. While the NDX is on an aggressive sell signal, it is the most likely to be subject to pushback. The Cycles Model suggests today may be a day of strength. After yesterday’s new high in the SPX, the trend may still be “up.”

Today’s op-ex shows Maximum Pain for options investors at 15530.00. Long gamma begins at 15550.00 while sort gamma begins at 15510.00.

ZeroHedge observes, “Most long in a very long time

Asset managers are the most long US equity futures since December 2009 at 57% of gross exposure… historically these levels have seen the S&P 500 down by an average of 9% over the next 6M, with equities down 2/3 of the time…”

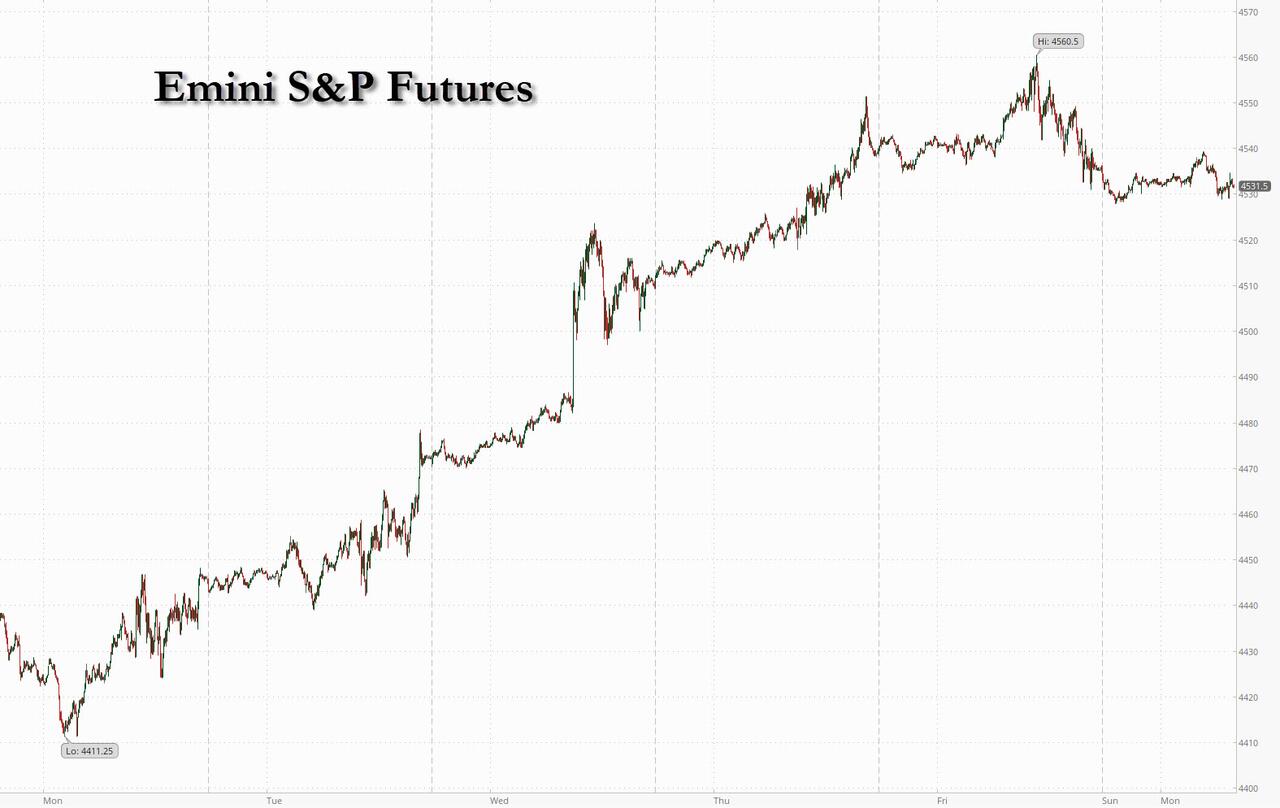

SPX futures are down to 4558.90, teasing the short-term trendline at 4550.00 where a possible aggressive sell signal may lie. The Aggressive sell signal may be reinforced at the Cycle Top support at 4479.77. Today is day 265 in the current Master Cycle. Yesterday’s high may have been the top of this Cycle, but we await confirmation after the FOMC meeting.

Today’s op-ex shows Max Pain at 4545.00. Long gamma starts at 4550.00 while short gamma may begin below 4540.00. This is a very tightly wound market that may spring in either direction at the drop of a pin.

ZeroHedge reports, “US futures are lower as we enter the “last hike” day, with European stocks slumping after ugly results from LVMH (which tumbled 4.5%) and Asian markets also closing in the red as investors brace for more tightening from the Federal Reserve, even as results from some of the biggest European and American companies hinted at slowing economy and declining earnings. As of 7:30am ET, S&P eminis dropped 0.1% at 4,589 while Nasdaq futures were down 0.3%, pressured by disappointing results from some top constituents.”

VIX futures have pressed above yesterday’s high at 14.09. The 50-day Moving Average awaits at 14.97 for a confirmed buy signal. The Cycles Model views today as a day of strength, so it appears likely that the 50-day may play a big role in today’s action.

Today’s op-ex shows Max Pain at 14.50. Short gamma shows very weakly at 14.00, while log gamma starts at 15.00 and runs to 40.00.

ZeroHedge notes, “GS volatility observations

1. The 1-month implied volatility for the average stock in S&P Technology sector (XLK) is in its 29th percentile over the past year which is the highest among all sectors.

2. S&P 500 average stock put-call 1-month normalized skew remains low vs history, implying investors are already positioned for short-term up move which makes it more difficult for the market to rally. (GS derivs)

Bond volatility – last man standing

The MOVE has drifted lower over past sessions, but remains elevated. Let’s see if the last elevated volatility index decides coming down post the upcoming FOMC. The gap vs VIX is still huge.”

TNX is down this morning to a low of 38.59 as it corrects toward Intermediate support at 38.23. Today is day 252 of the current Master Cycle. A lot may happen in the next week.

ZeroHedge remarks, “The size of the Federal Reserve pivot, i.e. the interest-rate cuts expected by the market, is likely to continue falling as inflation starts to decline at a slower rate.

The outcome of today’s FOMC is close to a foregone conclusion. After the expected 25-bps rate hike there is only 10 bps of rate rises left priced in by markets. But it is in the later parts of the SOFR rates curve – where the pivot is – that we’re likely to see more of the price action.

In the chart below of the SOFR curve, we can see the rate cuts priced in by the market have been falling.

Last meeting the Fed passed on hiking rates, but amped up the hawkish message. While it is clear what the Fed will do with rates this meeting, it is less certain what happens at subsequent meetings as the FOMC becomes less convergent in its views.”

USD futures drifted lower to 100.81 this morning. USD may retest its trendline at 100.00, but the new trend may be higher. While the Cycles Model appears calm, the USD may be prone to a sudden move should the Fed surprise.