10:16 am

The Banking Index is in day 255 of its Master Cycle. It appears that the Cycle reversal may be a result of the FOMC announcement on Wednesday, day 257. It is interesting how Cycle turns may occur on days like that. Please note that the trendline at 93.00 from the Head & Shoulders formation has not yet been retested yet. That may occur this week to signal the reversal.

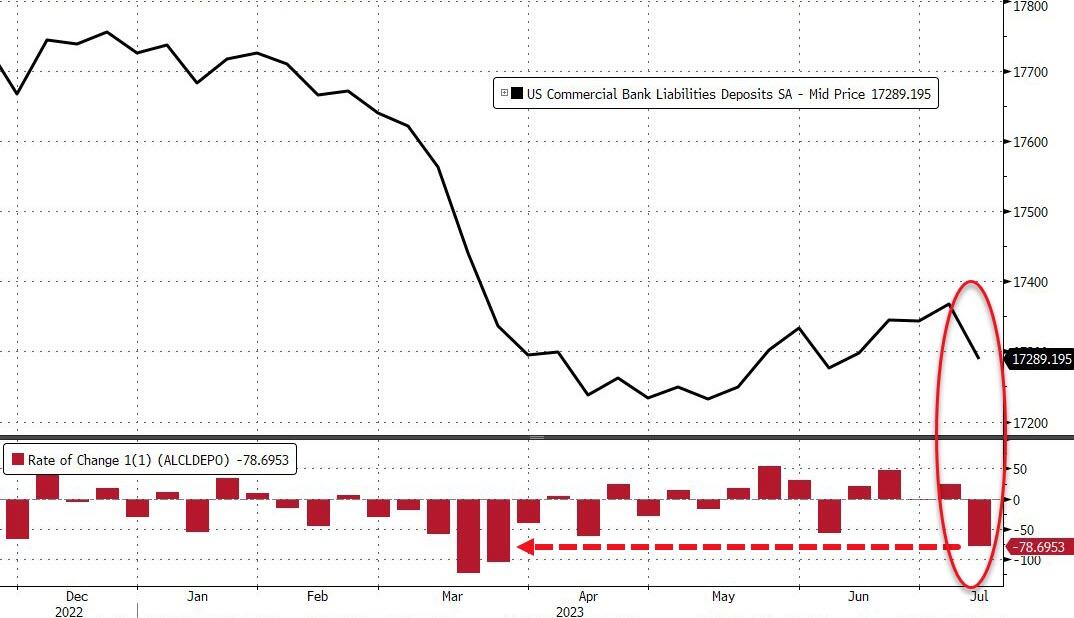

.After Friday’s close, ZeroHedge announced, “The flow of funds continues into retail money-market accounts and banks’ usage of The Fed’s bank bailout fund remains at record highs (above $100 billion), but tonight we get to see The Fed’s latest efforts in obfuscation and seasonal-shenanigans about US banks’ deposits and loans.

Seasonally-adjusted, total deposits plunged $78.7 billion last week – the biggest weekly ‘run’ since March 22nd (right after SVB)…

8:10 am

Good Morning!

NDX futures bounced to 15486.60 over the weekend, but have eased back since then. Last Wednesday’s high at 15932.05 remains the topo of the Cycle.

I am taking the long view (3.5 year chart) in order to point out some important technical details. The first one is that NDX never violated the uptrend line that existed since 1987 (possibly longer). This explains why NDX has outperformed all the other stock indices since the 80s. The second observation is that NDX has been the major beneficiary of vast swathes of liquidity existent since the 80s and until recently. Third, it has retraced 86.9% of the 2022 decline, completing its first probable bear market Cycle. Finally, due to all the previous factors, investors are wildly bullish and may potential be caught wrong-sided in the oncoming decline.

Today’s op-ex shows Maximum Investor Pain at 15380.00. Long gamma starts at 15400.00 while short gamma may begin gat 15350.00.

ZeroHedge observes, “Time may change me, but unlike David Bowie, we can trace time (or at least what went on over time). Let’s look at some weekly performance data for the Nasdaq 100 (NDX), the equal weighted Nasdaq 100 (NDXE), the Russell 2000 (RTY), the S&P 500 (SPX), and the equal weighted S&P 500 (SPW).

The Nasdaq has been leading the charge, but while it went up every week from late April until early June, the performance has been more inconsistent as of late. For the past 3 weeks, the Nasdaq 100 has provided the lowest return of the group (around 1.5% versus almost 4% for the Russell 2000).”

SPX futures retraced to 4550.10 this weekend, but has also eased back. Wednesday’s peak remains the high for the Master Cycle. The trend may revert to a decline.

The long view in the SPX is different from NDX. It had historically remained beneath the 1987 trendline until early 2021. After testing the trendline in February and March 2022, it decisively declined beneath it in May. SPX came back to retest the trendline in August. Normally that would have been the final retest. However, the Liquidity injections by the Fed and the Bank of Japan may have given the SPX another retest. The normal Cyclical pattern is that retracements usually stop near the mid-Cycle resistance, a 20% rally from the low. However, when it exceeded that level, many claim the SPX may now be in a bull market having exceeded a 20% rally from the October low. However, while the rally gained 31% from the low, it has only retraced 82% of the 2022 decline, the bull market is a myth unless the rally exceeds the January 2022 high at 4818.62.

In today’s op-ex, 4550.00 is heavily contested. Long gamma may begin at 4575.00-4600.00, while short gamma kicks in at 4500.00.

ZeroHedge reports, “Futures rose as we enter a very heavy macro and earnings week highlighted by the Fed, ECB, BOJ, global PMIs and GDPs, US PCE, as well as earnings by GOOGL, MSFT and META. Global bond yields are lower after sharp declines in manufacturing and services gauges across Europe fanned concerns about economic growth. At 7:45am ET, S&P futures were 0.2% higher at 4,572 while Nasdasq 100 futures were up 0.3%. The USD was higher as cable slumped after a big miss in UK PMIs, commodities were in the green with gold, iron ore and oil prices all climbing. Today’s macro focus will be the US PMIs release (consensus expects 46.2 on mfg and 54.0 in services). Keep an eye on the price/inflation discussion in the detailed PMI report.”

VIX futures rose to a weekend high at 14.30. The June 22 low remains the bottom of the 21.5 month Cycle. This Cycle Pattern suggests a probable Long Cycle high in February-March, 2025.

Wednesday’s op-ex projects the probable Max Pain at 14.50. While short gamma is virtually nonexistent, long gamma may extend to 40.00. The next monthly op-ex on August 16 shows Max Pain highly contested at 17.00. Short gamma extends between 13.00 and 16.00. Long gamma begins at 18.00 and extends to 60.00.

TNX is lower this morning, on day 250 of the Master Cycle. The Master Cycle low may have been put in early, on Wednesday. However, there is too much potential for TNX to go in either direction in the next week to call the end of the Cycle. Should it go lower, the mid-Cycle support is at 36.82, so the downside may be limited.

USD futures are higher this morning, to 101.15 after it has climbed above its trendline. The bottom of the Cycle may have come early (day 245). Since then it has made an aggressive buy signal. That is worth taking note. Should the buy signal hold, USD may rally through the end of August.