10:10 am

BKX, our liquidity proxy, made a new retracement high at the open, then reversed lower. JPM’s glowing report comes at a cost to other banks’ solvency. The Banking crisis may be about to resume.

ZeroHedge remarks, “Q2 earnings season officially started just before 7am ET when JPM reported earnings which, as expected, trounced expectations primarily on the back of generous contributions from the First Republican FDIC/taxpayer bailout-cum-gift, which has helped push the bank’s net interest income that much closer to a mindblowing $100 billion.”

8:40 am. Bastille Day

Good Morning! I spent a little extra time in analysis this morning. I hope you appreciate it.

NDX futures spent the night beneath yesterday’s high at 15602.74. It qualifies as an extended Master cycle high at day 273. While there is no definitive reversal, the Cycle formation may be complete.

Today’s op-ex shows Maximum Pain for investors at 15530.00. Long gamma starts at 15550.00 while short gamma begins at 15500.00. Options investors have been front-running a very large playerthat may have withdrawn from the game.

ZeroHedge remarks, “NASDAQ – perfection continues

The perfect trend channel that has been in place since March lows stays very much intact. This time around we touched the 21 day and decided to bounce (without even testing the lower part of the channel). Note how far down the 50 day is…”

That player is the Bank of Japan. Since early January, the Yen has declined 12% to the USD. As a result, that change in the FX market has magnified the gains of all stock investments in the US, but especially in the NDX. Since early this year, the NDX has appreciated by 56.5% in Yen. The Bank of Japan is notorious for owning stocks, something that the Fed would not do publicly. That Cycle may now be over, as this combination is now testing the Cycle Top at 212.65. A cross beneath it implies a change in trend. The “perfect investment” may have lost ist largest supporter.

SPX futures ventured marginally higher, to 4519.80 this morning, but may have lost momentum. As mentioned earlier, yesterday was day 273 in the Master Cycle. A new Master Cycle may have arrived. With it may come a five-fold increase in strength and volatility. I hope you are ready.

Today’s op-ex shows Max Pain at 4465.00 Long gamma starts at 4475, while short gamma may begin at 4450.00.

ZeroHedge reports, “The week’s powerful rally which sent US stocks to a new 52-week high has faded, with futs down small after a quiet overnight session on the day JPM officially ushers in Q2 earnings season as the post-CPI market rally pauses for breath as investors contemplate how recent US inflation data will impact upcoming Fed policy decisions. As of 6:45am ET S&P futures are flat at 4,542 while Nasdaq futures are down 0.1%. Bond yields are 3-5bp higher, and the USD has reversed higher after dropping the lowest level in more than a year. Commodities are mixed with energy lagging and base metals such as iron ore extending gains from yesterday. Yesterday’s dovish PPI and lower-than-expected initial claims supports the soft-landing narrative. Key focus today will be banks earnings; JPM, C and WFC report pre-market. Keep an eye on banks’ commentary on consumer health, credit trends and loan growth. We will also get the latest UMichsentiment data (consensus sees 65.5 vs. 64.4 prior); 1yr inflation expectation is estimated to fell to its lowest in two years”

VIX futures are on the rise, although not yetrising above the 50-day Moving Average at 15.62. Recall that VIX has challenged the 50-day and pulled back. This is a place to accumulate shares.

TNX has declined beneath the Intermediate-term support at 37.92, giving it a sell signal. The Cycles Model suggests that TNX may continue its decline to the first week of August. The likely target may be the Cycle Bottom at 32.59.

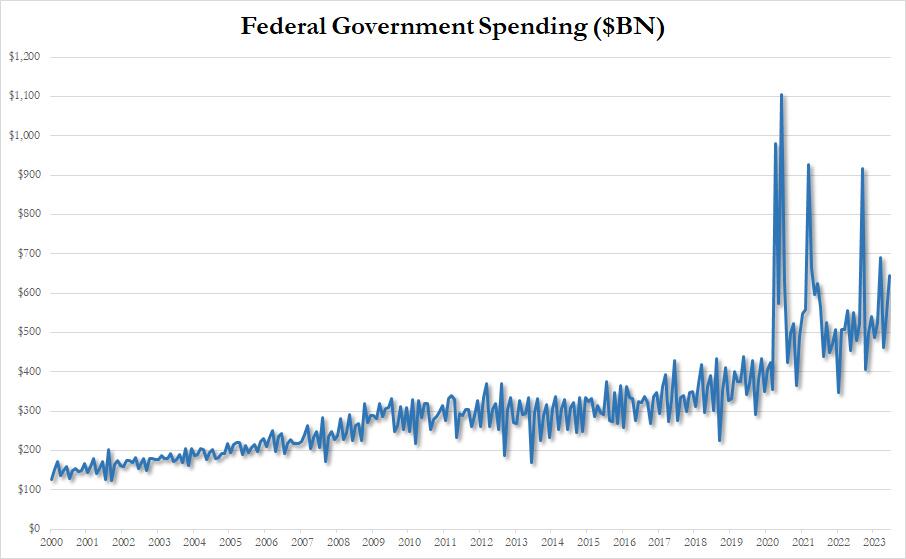

ZeroHedge remarks, “There was a shocking number in today’s latest monthly US Budget Deficit report. No, it wasn’t that US government outlays unexpectedly soared 15% to $646 billion in June, up almost $100 billion from a year ago…

… while tax receipts slumped 9.2% from $461 billion to $418 billion, resulting in a TTM government receipt drop of over 7.3%, the biggest since June 2020 when the US was reeling from the covid lockdown recession; in fact never have before tax receipts suffered such a big drop without the US entering a recession.”

USD futures have bounced to test the trendline near 100.00. It is currently in a throw-under of an Ending Diagonal formation, which may last a couple of weeks. During that time, USD may decline to its Cycle Bottom at 98.32. Calls for the demise of the USD may become more shrill, but this decline is merely a retracement of the 2021-2022 rally from 89.51 to 114.75 and not a change in trend.

ZeroHedge comments, “The prevailing downwards trend in the dollar is primed to remain intact while the real yield curve flattens.

FX is one of the hardest markets to get consistently right. Traders often employ a lot of leverage so there is little room for error, or for indiscipline with stops or sizing. But sometimes getting the bigger trends is not as frustratingly hard.

One of the best leading indicators for the dollar, for instance, is the real yield curve. The intuition is the dollar is driven at the margin by the real return of foreign investors into US yields.”