11:05 am

SPX has ventured into short gamma beneath 4490.00. The 2-hour mid-Cycle and Intermediate support lies at 4481.00. Hourly Cycle A ended at yesterday’s close. Hourly Cycle B is beginning as short gamma begins to influence the SPX. This may last until monthly options expiration. This is no place to be long, since SPX signals become elevated to a confirmed sell signal beneath 4481.00. The 50-day Moving Average lies at 4404.40 where most traders assume a sell signal.

10:00 am

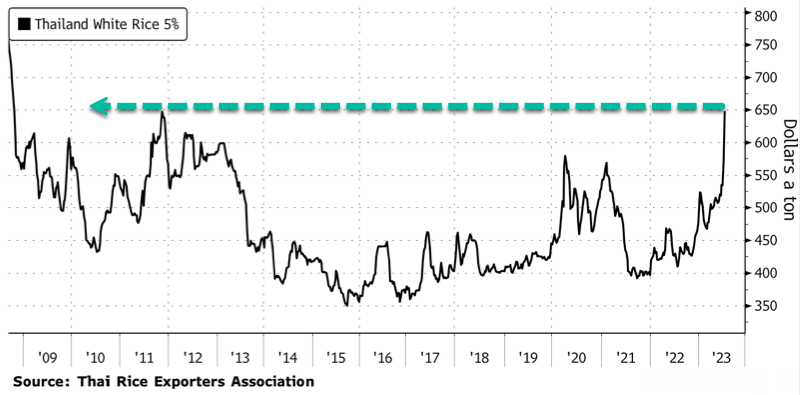

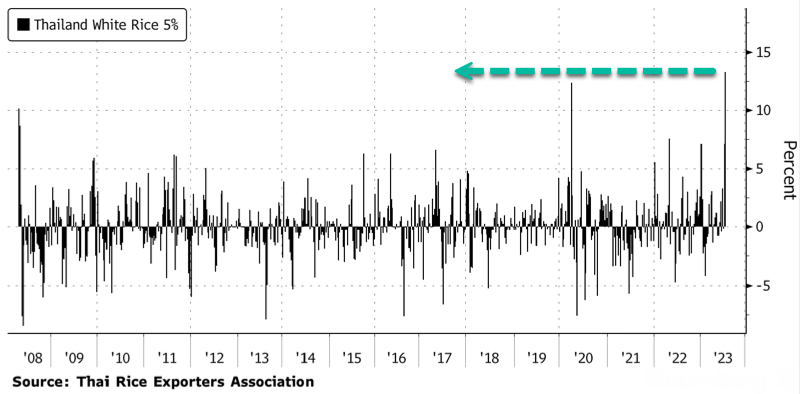

As the worldwide food crisis gathers momentum it is surprising to many that the Ag Index is still in decline. The Cycles Model maintains that there may be another two weeks of declining prices. As it turns out, the Cycles May be more powerful than any fundamental reason for the price being what it is. While worldwide demand due to shortages may be rising, domestic consumption has gone down as consumers retrench. This provides investors with a potential opportunity to buy food and ag-related investments at prices not seen in two years. The news of pending shortages may not have hit the grocery shelves yet.

ZeroHedge observes, “On Wednesday, the Thai Rice Exporters Association revealed that the price of Thai white rice 5% broken, a key Asian benchmark, reached the highest level since Great Financial Crisis. This surge is mainly attributed to increasing fears of a global shortage due to the damaging effects of the El Nino weather phenomenon on Asian farmlands and India’s recent decision to restrict certain rice exports.

Thai white rice 5% broken hit $648 per ton this week, the highest level since October 2008. Prices are up over 50% since the start of 2022.

The weekly change in rice prices is about a 13% surge, the largest since the index began in the summer of 2008. ”

8:15 am

Good Morning!

NDX futures rose to an overnight high of 15354.10, approaching the Ending Diagonal trendline at 15500.00. It has since reversed back down to the flat line. While NDX may be positive for another hour or so, it may already have made the key reversal in the overnight session.

Today’s options expiration shows Maximum investor pain at 15280.00. Long gamma begins at 15300.00. Short gamma starts at 15200.00. Sentiment is still positive in the NDX, with calls outnumbering puts.

ZeroHedge comments, “SPX – say hello to the 50 day moving average

SPX is approaching the 50 day moving average. The big trend channel since March lows is still intact, but watch for a possible break down eventually. Momentum has changed rapidly…100 and 200 day moving averages remain way lower.

Source: Refinitiv

NASDAQ hitting the 50 day

NASDAQ is currently trading right on the 50 day moving average. 15200 is a short term level to watch, but the bigger support is at 15k. NASDAQ is now established “well” below the channel and pretty much all bigger candles since recent highs are all bearish.”

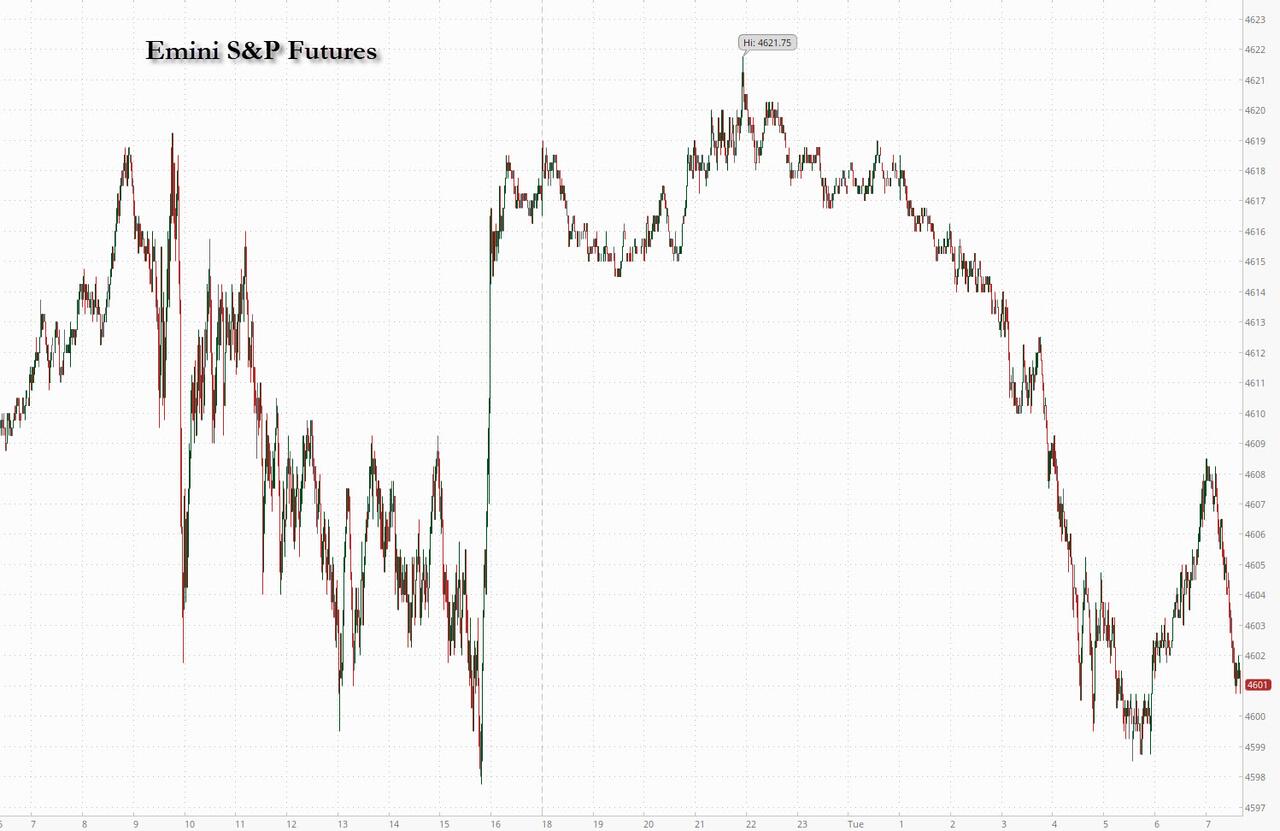

SPX futures rose to an overnight high of 4517.30, nearly matching Monday’s high at 4519.84 and completing an expanded flat correction. It has since pulled back to the Max Pain zone. The Cycles Model indicates a probable change in the hourly Cycles, suggesting a panic decline may have begun. Indications are that the decline may accelerate into the monthly options expiration. The initial target may be the March 13 low at 3808.86.

Today’s op-ex shows Max Pain at 4500.00, which is hotly contested with 4854 calls and 5115 put contracts. Long gamma starts at 4530.00 while short gamma triggers at 4490.00 and remains strong down to 4380.00. Today may be dominated by short gamma.

ZeroHedge reports, “S&P futures point to a higher open after China officially entered into deflation with -0.4% CPI print, continuing the buying momentum from the second half of yesterday’s session while European stocks rebound sharply from yesterday’s rout led by a rebound in Italian banks after the government backtracked on part of its new windfall tax on lenders. As of 7:45am ET, both S&P and Nasdaq 100 futures are 0.2% higher with other global markets also in risk-on mode, with the euro strengthening, copper rebounding, 10Y TSY yields rising to 4.03% ahead of another closely watched bond auction later today (US government is selling $38 billion of new 10-year notes, $3 billion larger than the last 10-year note debut in May) and oil rising by $1, just inches away from 2023 highs. Rice in Asia soared to its highest level since 2008.”

ZeroHedge warns, “We just had a long period of calm in the market, but now it is as or more important than ever this year to be monitoring market gamma levels.

We just had the first negative market gamma reading of the quarter on Thursday, and then an even stronger negative market gamma reading on Friday.

The longer the market remains trapped in negative market gamma territory, the more dangerous it gets because there is more opportunity for fragility (from declining liquidity and shock absorbing gamma) to meet a burst of systematic market risk or other kind of momentum event.”

VIX futures declined further in the overnight market to 15.47, completing an expanded flat correction. Yesterday’s breach of the trendline at 18.00 has put it on a confirmed buy signal. Next Wednesday’s monthly op-ex has special significance and may give us a new high not seen since March.

ZeroHedge announces, “Welcome to fear

Regular readers of TME are familiar with one of our favorite “under the hood” stress indicators, the VIX 2/8 months spread. This one is moving into fear territory…

Source: Refinitiv

Last time…

…VIX was here, the SPX traded close to 4250. You do not compare mean reverting assets to trending assets over longer time periods, but shorter term “gaps” are not to be dismissed.

TNX bounced back above 40.00 and may threaten to make a new high. Usually corrections stay within the limits of the previous high or low. However, there are expanded corrections that may probe a new high and still be corrective, as the Cycle may end back down at the low. This may be such an event.

A more likely explanation is that Wave 5 may be expanding. The reason is that the new Master Cycle runs to mid-September. If so, we may see TNX reach 45.00-50.00 within this Master Cycle.

ZeroHedge reports, “Amid all the recent worries about demand for US paper, between the Fitch downgrade, the $1 trillion planned issuance in Q3, the doomsday language in last week’s TBAC refunding statement which warned of big increases in auction sizes in coming months and – of course – Ackman’s latest melodrama, some were worried that today’s 3Y auction would be a dud. It wasn’t, and in fact today’s 3Y auction was nothing short of spectacular.

The high yield of 4.398% was below last month’s 4.534% and also stopped through the When Issued 4.416% by 1.8bps, the second consecutive stop through auction and 5th of the last 6.”

USD futures are consolidating, testing the 50-day support. The Cycles Model suggests the new Master Cycle may run until the end of August. There are conflicting views on what happens next. USD is setting up for a very large move higher. However, it may have some downside work to finish before the move to higher ground. I remain neutral at this time until further developments.