3:35 pm

SPX futures may be bouncing off the Diagonal trendline at 4525.00. The 2-moth trendline is a clear demarcation for a sell signal. Keep that in mind as tomorrow may be the largest July op-ex in history.

ZeroHedge remarks, “Tomorrow will see the largest July options-expiration on record, driven by continued growth in index and ETF options volumes.

Admittedly, July tends to be one of the smaller expirations of the year (January, March, June, September and December are the largest expiration months).

But, Goldman Sachs’ John Marshall estimates that over $2.3 trillion of notional options exposure will expire this Friday including $500 billion notional of single stock options.”

3:04 pm

NDX fell deep into short gamma territory beneath 15800.00 as the monthly op-ex and rebalancing loom large. There is likely to be a bounce in the overnight session but the damage has been done.

ZeroHedge remarks, “Something remarkable is taking place under the market’s silky-smooth, VIX 13 surface: hedge funds are quietly blowing up. Not blowing up in the traditional sense of Amaranth, LTCM or Archegos, but as a result some rather unique market dynamics (discussed in “Historic “Spot Up/Vol Up” Chase Amid Multiple Unprecedented Developments In Derivatives“) hedge funds find themselves suddenly breaching position limits and forced to liquidate exposure (on both the long and short sides), in other words, degross and delever.”

12:30 pm

The Ag Index has gained a lot of volatility, as news of world evens go from bad to worse. It should be no surprise to see the dramatic moves over the past month. At the end of June I had stated that this is a good time for accumulating shares of Ag products and businesses, with patience. The reasons for this are two-fold. The first is the opportunity to double or triple returns in the next year. The second is that GKX is likely to decline to an earlier-stated target at 380.00 before the real uptrend begins. The Cycles Model now suggests a month-long decline toward that stated target. No one said that long-term investing is easy, but the rewards are there for the cool-headed.

ZeroHedge warns, “With as of Monday the Black Sea Initiative grain deal effectively having collapsed, Russia has been warning that ships traveling to Ukraine’s Black Sea ports will be seen as potential military targets. The dire warning came after Ukraine’s government said it would persist in its grain and food exports via a temporary shipping route. A Wednesday statement from the Russian defense ministry (MoD) had announced “the flag countries of such ships will be considered parties to the Ukrainian conflict.”

Ukraine on Thursday issued its own ‘retaliatory’ message, warning in turn that ships and food tankers going to Russian ports could come under threat. US intelligence is also now alleging that Russia has begun laying mines once again in order to block Ukrainian ports.”

ZeroHedge explains, “After cancelling the Black Sea Grain Initiative deal, Russia has attacked the port of Odesa. Ukraine said the drone and missile strike specifically targeted its capacity to export grain out of Odesa, damaging a warehouse and a grain and oil terminal. Adding insult to injury, Russia warned that any ships sailing to Ukraine’s Black Sea ports would be seen as “potentially carrying military cargoes,” to further stifle Ukrainian exports. Russia did not say what it would do if any ships were found sailing to Ukrainian ports, but the US issued a warning that Russia’s attacks may expand to civilian ships.”

12:16 pm

The Banking Index may be in the final days of the retracement rally, having exceeded the 38.2% retracement value at 87.79 today, day 251. $300 billion provided by the Fed in March has just delayed the banking index from imploding. Liquidity is starting to unravel again with dire consequences. The Cycle Model infers that (down) trending strength is about to return with a potential panic starting this weekend. Americans have stopped paying down their debt, leaving banks holding the bag.

ZeroHedge remarks, “The New York Federal Reserve Bank said more Americans had their credit applications rejected last month at levels not seen in years.

The New York Fed reported on July 16 added that fewer people across the country also sought to borrow.

The report was part of the bank’s monthly Survey of Consumer Expectations, which is taken every four months to assess credit access issues in the United States.”

7:30 am

Good Morning!

NDX futures have fallen beneath a short-term support at 15775.00 this morning. That, coupled with the Cycles Model suggesting the end of the Master Cycle, allows us to consider an aggressive short position. The next level that reinforces the aggressive short position is the Cycle Top support at 15388.52. At the minimum, long positions should be cleared.

Today’s op-ex shows Max Pain at 15825.00. Long gamma starts at 15850.00 while short gamma may begin at 15800.00. Sentiment leans toward the longs, but is weakening.

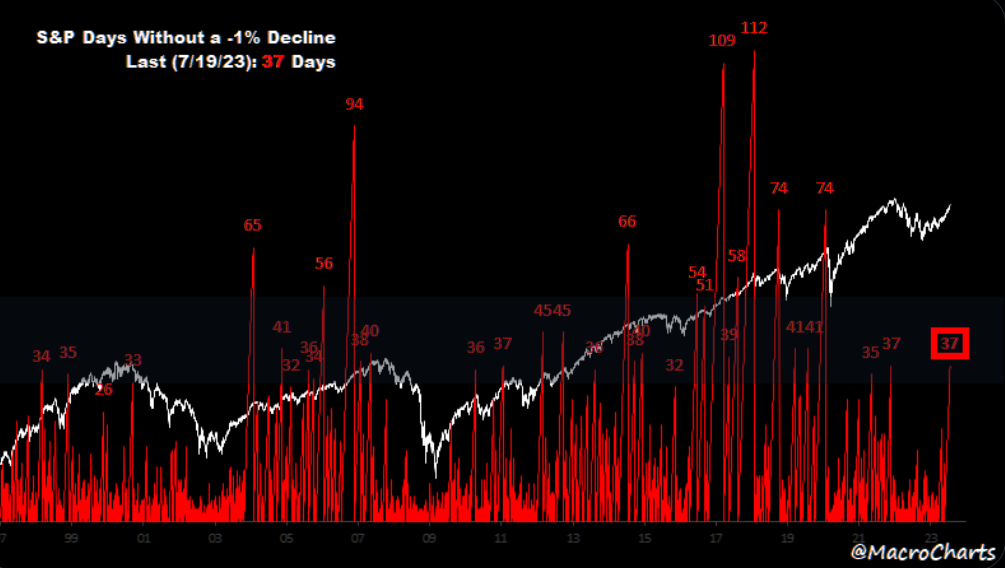

ZeroHedge remarks, “No declines market

The S&P has gone 37 days without a 1% decline. We saw this last at the November 2021 top. Is this time different?

Source: MacroCharts

Inverted fear

MAGMA options pricing is becoming extreme. Skew for this “sector” is close to all time lows, 1st %ile over 10yr. Some of the majors such as AMZN, MSFT, GOOGL are all trading with inverted skews, calls over puts. Upside fear is the new normal…”

SPX futures have eased down to a morning low of 4549.90. We may have seen the Master Cycle high yesterday, on day 258. It also marks the probable end of an 18.5-month Cycle from the 2022 top. Should the reversal make its turn here, the Cycles Model suggests a decline to the end of August.

Today’s op-ex shows the strike at 4550.00 being hotly contested by both puts and calls. Long gamma may begin at 4570.00, while short gamma may start at 4530.00.

ZeroHedge reports, “US equity futures are lower as tech stocks struggle after some disappointing earnings updates from the sector. At 7:30am ET, S&P futures are down 0.2% while Nasdaq futures slide 0.8% as Tesla drops 3% in the premarket after Q2 profitability shrank, and Elon Musk said Tesla will have to keep lowering the prices if interest rates continue to rise. Months of markdowns have already taken a toll on automotive gross margin, which fell to a four-year low in the second quarter. Netflix tumbled over 6%, its biggest intraday decline since December, after missing sales estimates and projecting third-quarter revenue that fell short of Wall Street estimates suggesting a crackdown on password sharing and a new advertising tier aren’t yet delivering the sales growth analysts anticipated. The rest of the Magnificent Seven are also lower while premarket bright spots includes airlines and banks. European chipmakers are also on the back foot after a cautious outlook from TSMC. Elsewhere, Treasury yields have climbed across the curve, while the dollar has drifted lower. Gold, oil, iron ore and bitcoin prices all increased. The macro data focus is on Leading Indicators, Jobless Claims, Philly Fed, and Existing Home Sales.”

VIX futures made a morning high of 13.98. The Cycles Model suggests a return of trending strength today and rising through next week.

Zerohedge remarks,”VIX’s “natural” floor

SPX is a trending asset, while VIX is a mean reverting asset. We have seen the SPX move higher, while the VIX refuses moving much lower. Volatilities at these levels have very limited downside. Using cheap volatilities for various strategies here makes a lot of sense. Replacing longs with calls, chasing further upside via calls or hedging downside exposure are all looking attractive.”

TNX may have resumed its rally, having risen above the Intermediate-term resistance at 37.98. However, the Cycles Model suggests possibly another week of decline. While normally this morning’s move would be a buy signal, the MOdel suggests we wait for further confirmation.

ZeroHedge comments, “Large and persistent fiscal deficits will entrench inflation and decimate the long-term real return of stocks and bonds, while reversing the secular underperformance of real assets.

Leviathan is back. After the post-GFC years of fiscal restraint, governments around the world are now running persistently higher deficits. This is a sea change, and it means a markedly different investment environment.

The Fed put was a backstop for financial assets. But the Treasury put is a different beast.

Assets may be able to post a positive nominal return, but in real terms they are likely to do poorly. Real assets, after 60 years of dreadful underperformance, are poised to finally begin outpacing stocks and bonds.”

Yesterday, ZeroHedge reported, “Moments ago, the Treasury held this week’s lone coupon auction in the form of a 20Y sale (really a 19Y-10M reopening) which came in solid, if not quite as stellar as last week’s auctions.

The high yield of 4.036% was above last month’s 4.010% and the highest since last November’s 4.072%; it also tailed the When Issued 4.035% by one modest basis point.

The bid to cover was 2.68, which while below last month’s 2.87 was just above the recent average of 2.67,

USD futures have continued to rise above the trendline at 100.00 for a possible confirmation of a buy signal. The reversal is about two weeks early, so we may wish to reserve judgement for another day or two. Should the reversal hold, the uptrend may be established, lasting through the end of August.