8:00 am

Good Morning!

NDX futures have risen to 15176.40 this morning, riding above the Cycle Top support at 15078.82. The Cycle Top is 2 standard deviations from the mid-Cycle support at 12560.06. After two months above the Cycle Top, a reversion to the mean may also suggest a decline well below the mid-Cycle value. The Cycles Model suggests the current Cycle interval may last until monthly options expiration on July 21. Thus far it is directionless.

Today’s op-ex shows 15120.00 being hotly contested. Long gamma starts at 15150.00. Short gamma begins at 15000.00.

RealInvestmentAdvice comments, “Does stock risk decline the longer the holding period is? It’s a great question and something I received a comment about.

Blaise Pascal, a brilliant 17th-century mathematician, famously argued that if God exists, belief would lead to infinite joy in heaven, while disbelief would lead to infinite damnation in hell. But, if God doesn’t exist, belief would have a finite cost, and disbelief would only have, at best a finite benefit.

Pascal concluded that given that we can never prove whether or not God exists, it’s probably wiser to assume he exists because infinite damnation is much worse than a finite cost.

When it comes to investing, Pascal’s argument applies as well. ”

SPX futures rose to 4452.00, testing the June 30 high at 4458.48. However, the CPI is due at 8:30 and may either boost SPX to a higher peak or take the steam out of the rally. The Cycles Model suggests the current Cyclical interval may last until monthly options expiration.

8:35 am

SPX futures have reached a new high at 4475.40. The CPI was up .2% for the month of June.

Today’s op-ex shows Max Pain at 4415.00. Long gamma starts at 4425.00 while short gamma begins at 4400.00.

ZeroHedge reports, “US equity futures are trading near session highs boosted by a global risk-on mood ahead of a US CPI report for the month of June which JPM said is “more likely to print dovish than hawkish” and is expected to show annual US headline inflation falling almost 1% to 3.1% Y/Y while core CPI is seen dipping less, to 5.0% YoY, which according to the market will erode the case for more rate hikes. Dovish sentiment pushed the dollar lower for a 4th straight day, sending the Bloomberg dollar index to the lowest since April, while also depressing Treasury yields.

As of 7:30am, following Monday’s solid gains, S&P futures traded higher 0.3% to 4,485 led by small-caps as bond yields and the USD move lower. Nasdaq 100 futures also rose 0.3%. Commodities are higher while gold, oil, and iron ore prices all higher amid increasing calls for fiscal stimulus from China; ags are also higher driven by next week’s expiration of the Black Sea Grain Initiative.”

ZeroHedge reports, “Expectations for this morning’s headline CPI print were for a plunge from 4.0% YoY to 3.1% YoY (due to shelter, used-cars, and seasonals); however, what The Fed will be watching for is Core Services CPI Ex-Shelter, which fell to +3.93% YoY – the lowest since Jan 2022…

Source: Bloomberg

The headline CPI rose just 0.2% MoM (below the 0.3% MoM expected) which dragged the headline down to +3.0% YoY (cooler than expected) – the lowest since March 2021..”

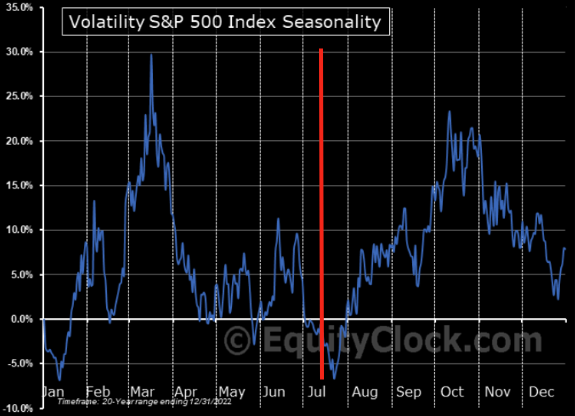

VIX futures plunged to 14.03 this morning on the CPI report.

Today’s op-ex shows Max Pain at 13.50. There is no short gamma. Long gamma begins at 16.00. Next week’s monthly op-ex shows Max Pain rising to 17.00. Short gamma makes a comeback beneath 16..00 while long gamma takes a strong position at 20.00 to 35.00.

TNX futures declined to 38.85 this morning. The correction in TNX may last to the end of the month.

ZeroHedge reports, “If there were some concerns that the week’s first coupon auction would be a disappointment due to today’s risk-on sentiment and lack of concessions into the 1pm auction block, they were promptly blown away moments ago when the Treasury announced results from today’s sale of $40BN in three year paper, which were nothing short of stellar.

Stopping at a high yield of 4.534%, this was more than 30bps higher than last month’s 4.202% and not far below the current cycle high of 4.641% reached in March (just before yields collapsed following the March banking crisis). The auction also stopped through the When Issued 4.536% by 0.2bps, the 4th stop through in the past five auctions (last month the auction tailed by 0.2bps).

The Bid to Cover jumped to 2.882 from 2.696, and was also above the 6-auction average of 2.686.”