12:32 pm

SPX may have stalled near the 50% retracement level at 4287.32 at the 4.3-day mark from the Wave 2 high. The dealers and hedge funds may have quit covering their shorts (buy high and sell low). The main issue for the rest of the day is to keep the SPX out of short gamma territory.

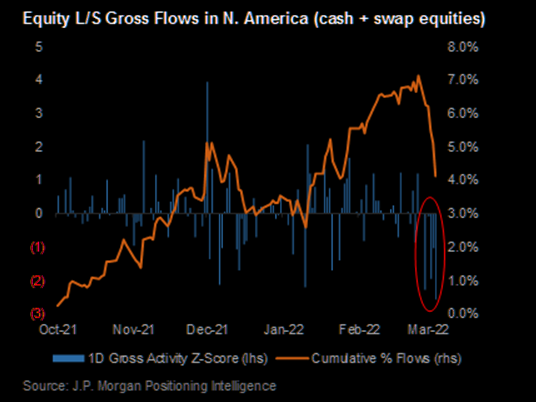

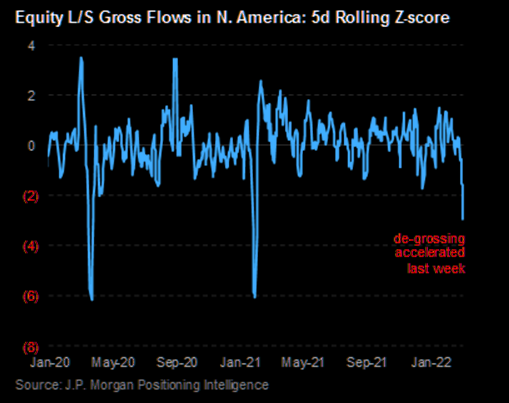

ZeroHedge explains, “Why such a violent equity squeeze on such ‘meh’ Ukraine / Russia headlines?

Nomura’s Charlie McElligott summarizes the long and the short of it succinctly below (Spoiler alert – Same shit, different day!)

As we’ve repeated numerous times, stocks are so deeply-immersed in Negative Gamma and critically, EXTREME “Short Delta” location for Options Dealers from all that downside hedging (after yesterday’s session, $Delta for SPX / SPY 0.2%ile, 0.0%ile for QQQ, 0.4%ile for HYG, 4.1%ile for IWM) that this means violent rallies which have to be “bot into” as Dealers cover shorts in futures.

Accordingly, McElligott has noted that any rally would have potent kindling for a short-squeeze from said “negative Delta,” as all those downside Puts are torched as we rally away from lower strikes, and the coupled “short hedges” from Dealers in futures will be bot back / covered.”

9:45 am

GKX may have made its Master Cycle high yesterday, on day 257. This may be a case of the lack of liquidity in the market trumping supply and demand, at least temporarily. Should that be the case, we may see GKX correcting down to the mid-Cycle support at 514.65 by the week of March 21.

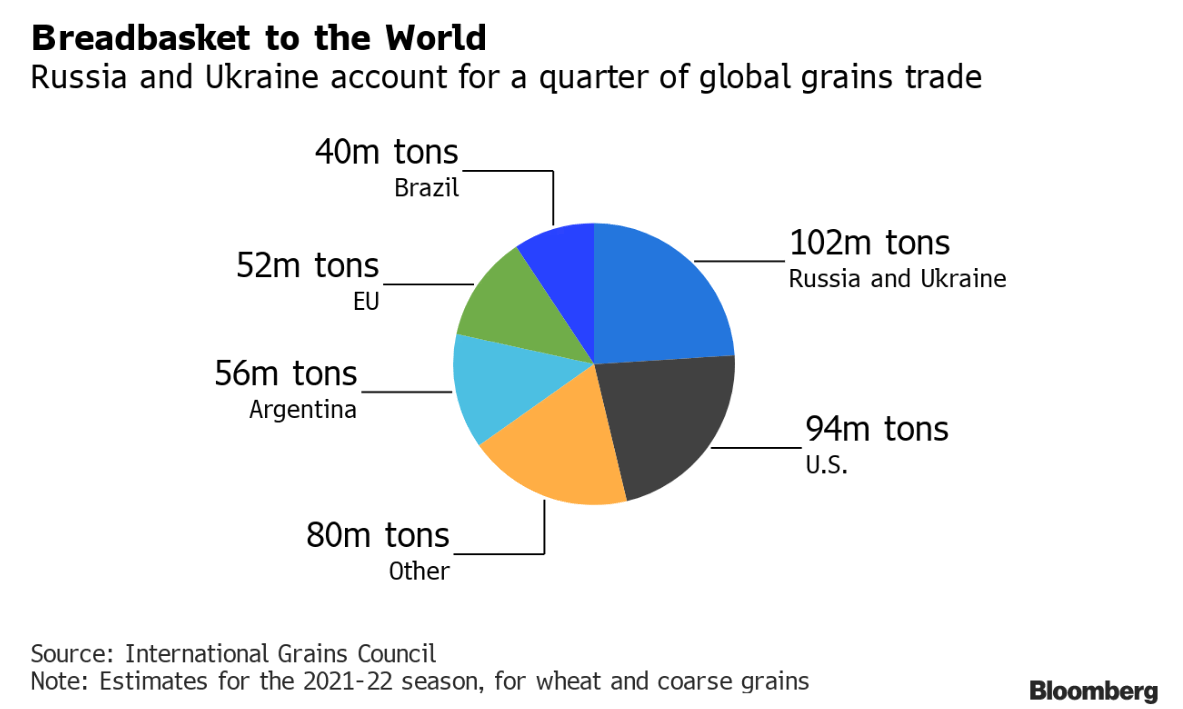

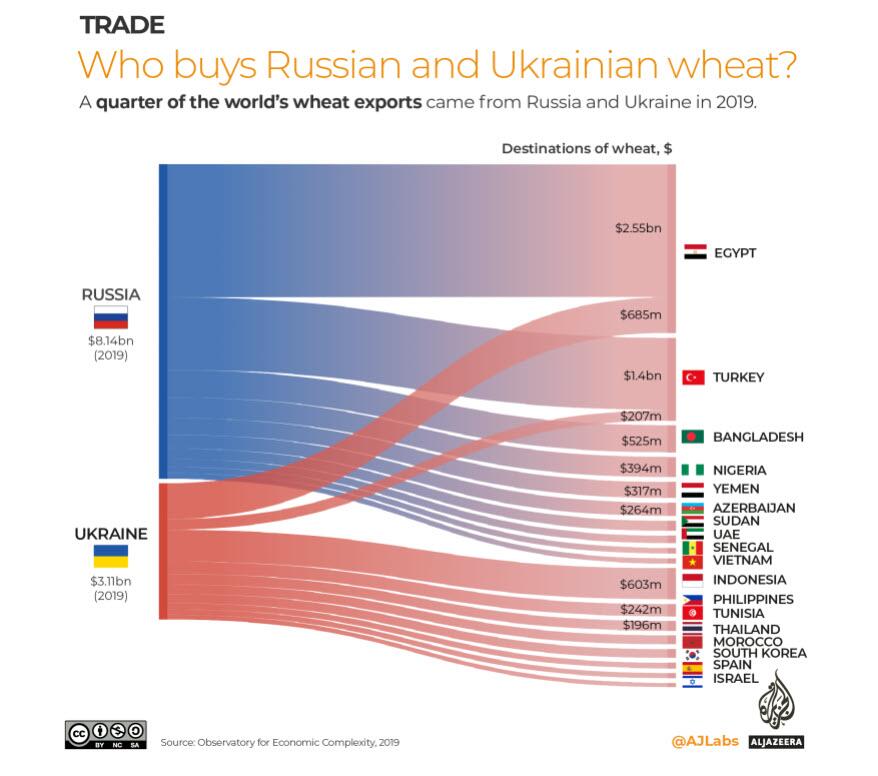

ZeroHedge remarks, “The world is heading for a “catastrophic” global food crisis as a result of the war in Ukraine, which will cause “hell on earth” for food prices, according to experts.

“Half the world’s population gets food as a result of fertilisers… and if that’s removed from the field for some crops, [the yield] will drop by 50%,” Svein Tore Holsether, head of agri company Yara International, told the BBC.

Known as “the breadbasket of Europe,” Russia and Ukraine export around a quarter of the world’s wheat and half of its sunflower products, such as seeds and oil.

“For me, it’s not whether we are moving into a global food crisis – it’s how large the crisis will be,” said Holsether, noting that increasing gas prices were causing a steep rise in the cost of fertiliser.”

8:10 am

Good Moring!

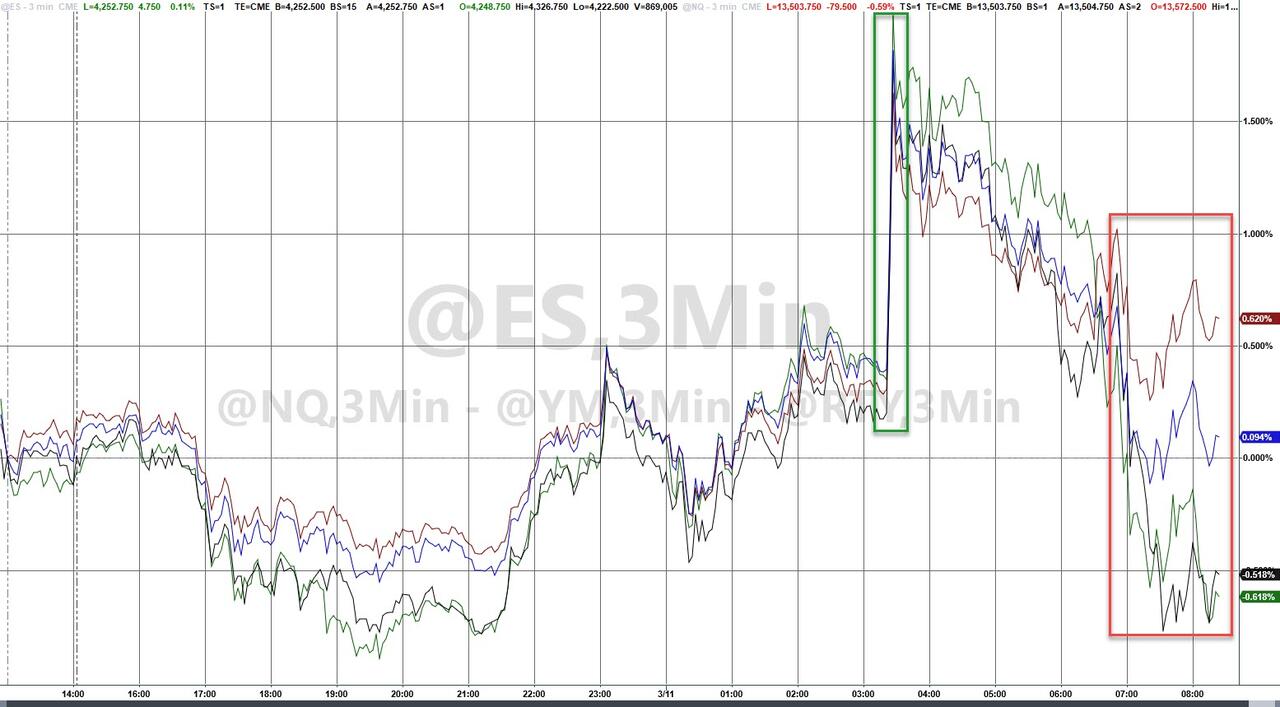

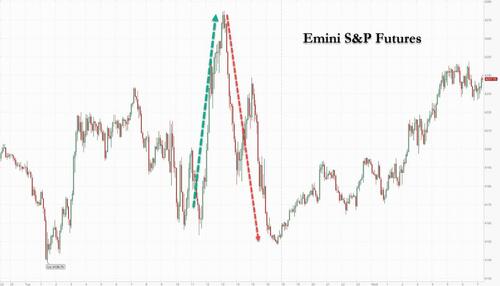

SPX futures have rallied to a morning high of 4251.70, a strong 77.5% retracement of the decline from yesterday’s high. Today’s options expiration is in short gamma beneath 4250.00. Dealers and hedge funds are attempting to gain elevation above that level, so as to cause the least damage to their book. Never mind the investors.

Equities are near the half-way point of a minimum 8.6-day decline potentially ending on March 15. The next 4.3 days are the most intense, giving way to multiple probabilities of limit down days. The key is the final and decisive decline beneath the neckline/Lip of the doubly bearish formation.

ZeroHedge reports, “After two days of sheer market insanity, including Monday’s furious plunge and Tuesday’s rollercoaster session, U.S. equity futures jumped after 4 straight days of losses, following European equities higher, as Ukraine optimism won, at least initially, over fears about high inflation and global stagflation as a result of soaring commodity prices, sparking a furious Delta squeeze (as we will show shortly in a subsequent post).

At 730am ET, Nasdaq 100 contracts were up 2.1% while S&P 500 futures gained 1.6%. The underlying benchmark fell for a fourth straight session on Tuesday to close at its lowest since June 2021. Dow futures rose 1.5%. A bond selloff extended as investor focus turned to upcoming central-bank rate decisions, while oil prices reversed a rally driven by President Joe Biden’s ban on fossil-fuel imports from Russia. . The dollar weakened for the first time in five days, as haven demand waned. Bitcoin soared more than 10% over $42,000 spurred by optimism about an impending U.S. overhaul of crypto oversight that Treasury Secretary Janet Yellen called “historic.”

VIX futures made an overnight ow at 32.38, stepping back from a steady march upward. It may be suing Short-term support (not shown) at 31.33 as a base for its continued advance. The Model suggests a high likelihood of testing the neckline in the next 24 hours.

The NYSE Hi-Lo Index made a deeper low at -392.00 at the close.

ZeroHedge comments, “What if the world survives – the VIX guy is back

We haven’t heard from the VIX guy in a while, but he called us earlier today. He hasn’t sounded this bearish pretty much ever. When you hear about nuclear wars from the VIX guy you really start thinking about whether or not fear has gone ahead of itself? To summarize: he sees all commodities surging further, the geopolitical situation spiraling out of control, Europe basically going back to stone age etc. His biggest take is that VIX and the European version, V2X, are going to the moon. We strongly disagree. It is time for a thread on fear…

What fear is the market pricing here?

Regular readers of TME know that the crowd tends to load up on protection too late and at way too rich levels as they tend to confuse direction with pace. Don’t forget that a 1% daily move translates to 16% implied volatility (approx). People have been paying very high premiums for protection lately. We find selling premium interesting plays here, both for overwriting positions, adding longs or simply selling people some rich fear. One example is the SX5E 3500/3800 strangle going for just above 200. That is collecting around 5.5% premium with “happy” to buy more at 3300 and happy to sell at 4000. We find this strategy extra interesting for people that want to add to longs, but are happy to sell a rip…”

TNX continues to make new highs off the Master Cycle low. It may be due for a pullback over the next week, especially when stocks resume their decline. However, the appears to strengthen over time, especially in April, as Wave 3 develops.

ZeroHedge comments, “The Federal Reserve has all but cemented expectations for a 25bps rate hike next week. But, events have changed a lot in the last couple weeks that raise a faint hint that the Fed may not hike, despite elevated, persistent inflation.

What makes us question whether the Fed achieves lift-off next week? Three things: 1) deterioration of growth expectations for 2022, 2) the VIX, and 3) fed funds futures.

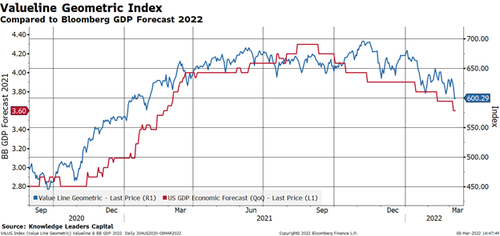

Since the peak in September of 2021, expectations for real GDP growth for 2022 has been steadily getting marked down. This helps explain the slide in the average stock this year—as measured by the Valueline equal weighted index. Does the Fed tighten into slowing growth?

USD futures retreated to an overnight low of 98.39 as it forms Wave [iv]. We may see USD decline further to its Cycle Top at 97.94 before its final push to 100.00 during the week of March 21.

Crude oil futures declined to 115.53 this morning, confirming the Master Cycle high on Monday. This may be an excellent entry point for a short position. However, the chart does not offer any support levels until the Cycle Top at 97.79. Pick our best level or wait for a bounce to place you order.

OilPrice.com reports, “IEA Chief Fatih Birol: Our members are ready to release more crude from their SPR’s to tame surging crude prices.

- Birol: “We are ready to [release] as much oil as is needed,”.

- Last week’s announcement of the oil release failed to stop rallying oil prices.

The members of the International Energy Agency are ready to release more oil from their strategic emergency reserves to tame the surging oil prices, the IEA’s Executive Director Fatih Birol told the Financial Times on Tuesday.

Gold may have made its belated Master Cycle high at day 280 yesterday, as suggested. Gold futures dropped to an overnight low of 1981.20, potentially confirming that event. Spike highs such as this are hard to negotiate at the turn, especially after being late. However, the Master Cycle immediately preceding this was 250 days, yielding an average at 265 days for the two Master Cycles. The probable target for a Wave (4) correction appears to lie near the Cycle Top at 1901.37.