12:21 pm

SPX opened lower, but formed a corrective bounce that has come within points of a 38.2% retracement at 4256.77. The 50% retracement is at 4287.32, but I wouldn’t count on it. The decline may soon be re-established after dealers finish unwinding their shorts…only to pick them up again at the end of the day. Gamma remains short beneath 4350.00. Selling pressure may soon pick up.

ZeroHedge comments, “Picking up where he left of with his “stuff is beginning to break” magnum opus yesterday, this morning Nomura’s Charlie McElligott writes that on top of the already well-established macro supply-demand “inflation shock” catalysts of the past 2 year period, the Ukraine-linked Commodities price/collateral/dollar funding squeeze -> “margin-call exercise” (which left a prominent Chinese trading tycoon significantly poorer after billions in margin calls), further amplifies the recent price-action in pockets of Energy, Metals and Ags.”

11:30 am

It appears that my “itchy trigger finger” on the sell button (GKX) last Friday wasn’t such a bad call after all. GKX has now declined beneath the Cycle Top support at 579.25 and a massive Head & Shoulders neckline at 570.50 that appears on the monthly chart. It appears that the loss of liquidity overrides the growing food crisis temporarily. The next Master Cycle (low?) comes up during the week of March 21, only two weeks away. GKX is now on a sell signal with the potential target at the mid-Cycle support at 509.36.

I have been an avid gardener all of my life, so the following missive from ZeroHedge comes as no surprise, “Spring in the northern hemisphere is two weeks away, and interest in planting gardens could rise as the breadbasket of Europe was choked off by the Russian invasions of Ukraine, jeopardizing global food exports resulting in skyrocketing prices.

Even before the turmoil in Ukraine, American households were under pressure due to soaring food and gas prices. The invasion just made things a lot worse as commodity prices jumped the most last week since the stagflationary period of the mid-1970s.

New UN global food price, released on Friday, showed global food prices in February surpassed a previous record set in 2011. About a quarter of the international wheat trade, about a fifth of corn, and 12% of all calories traded globally come from Ukraine and Russia. Food exports in the region have been halted due to conflict and sanctions.

This leaves us with a shrinking global food supply that may further price increases. Since spring is just weeks away, Americans will be in for a shock at the supermarket as the latest round of food inflation makes it to the store shelves. To mitigate the impact of grocery bills tearing apart household finances — interest in farming and planting gardens could take off and help expand the food supply.”

7:30 am

Good Morning!

Those of you who woke up this morning to see the SPX futures higher missed an exciting night. The roller coaster went down to 4142.80 before bouncing back to 4235.40. The breadth of these moves is staggering. Within 24 hours, the SPX declined 4.3%, then rallied 2.2%. That completes Wave [i] of 3 of (3). The next decline is a triple play Wave [iii] of 3 of (3). Wave threes are never the smallest, suggesting a high probability of a limit down in the next few days.

ZeroHedge reports, “Futures rebounded from yesterday huge loss, and after touching a session low of 4,138, S&P futures bounced shortly after the European when Bloomberg reported that the European Union was set to reveal a quasi “Marshall Plan” this week to issue issue “potentially massive” joint bonds to fund energy and defense and help counter the fiscal fallout from Russia’s invasion of Ukraine (how Europe will do that at a time when QE is ending and buyers for global debt are shrinking fast amid surging rates remains unclear). S&P 500 futures gained 0.7% following the benchmark index’s biggest loss since October 2020, while Dow futures rose 0.6%. Contracts on the Nasdaq 100 were up 0.6% at 7:15 a.m. Bonds and the dollar dropped, and the euro strengthened. The commodity melt up continued: nickel was halted on the LME after soaring 250%, oil traded just shy of $130 and gold was above $2000.”

VIX futures retreated to a low of 34.40, remaining within yesterday’s trading range, the highest close since the week of October 26, 2020. Tis now has traders concerned, being the eighth close over 30.00 since February 23. This is no longer being viewed as a one-off event. The target for Wave 3 has become imminent.

The NYSE Hi-Lo Index closed at -300.00. The Hi-Lo has awakened to a new plunge with a possible target of -2450.00.

NDX futures declined to an overnight low of 13107.20. It did not take out the trendline at 13065.40. However, it only bounced to 13420.40, unable to reach the 2-hour Cycle Bottom resistance at 13483.25. The decline appears to have resumed.

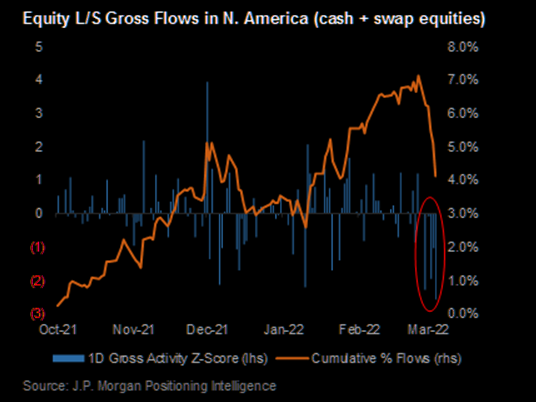

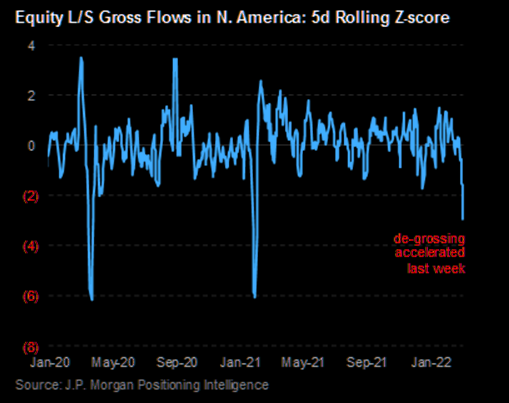

ZeroHedge observes, “Hedge Fund Panic selling (#1)

Equity L/S Flows: de-grossing accelerated last week and net selling also picked up

Source: JPM

Hedge Fund Panic selling (#2)

The L/S de-grossing in N. Am. last week was about a 3z event and the largest of the past 2 years aside from late January 2021 and mid-March 2020 (which were about 2x the current magnitude). Net flows were also negative throughout last week for this strategy—the 5-day net selling was >1.5z and the largest since the week ending December 17, 2021. Alongside the selling, net leverage for Equity L/S funds fell almost 3% last week to put it back in line with mid-December lows and the lowest since 3Q20.

USD futures pulled back to 98.88, still within yesterday’s trading range. The Cycles Model suggests a steady rally until the week of March 21, where it may make a final burst before its reversal. Depending on the strength of the final probe, the target appears to be near 100.00.

TNX gapped higher this morning, confirming yesterday’s buy signal. TNX is showing unusually large moves due to its high level of trending strength in the Cycle. This may last for the balance of the week. The rally may last until the week of April 18, leaving plenty of time for new highs.

West Texas Intermediate Crude pulled back from a high of 130.50 to an overnight low of 117.25 on the news of the prospective energy bond being floated by the EU. This has all the marks of a trend reversal on day 244 of the Master Cycle. While this is two weeks early from the average length of a Master Cycle, consider this; The Master Cycle immediately prior to this was 277 days long. The average of the two is 260.5 days, which falls in line with the Cycles Model.

ZeroHedge reports, “Confirming yesterday’s speculation that a ban on Russian oil imports is imminent, moments ago Bloomberg reported that the Biden administration is set to impose a ban on U.S. imports of Russian energy as soon as Tuesday without the participation of European allies, who as we discussed yesterday have been vocally – especially in the case of Germany – against such a blanket ban (because the import much more Russian oil and gas than the US).

The ban will include Russian oil, liquefied natural gas and coal, according to two Bloomberg sources who noted that the decision was made in consultation with European allies, who rely more heavily than the U.S. on Russian energy. In other words, the allies agreed to disagree on how important Russian oil is to them.

ZeroHedge observes, “Canada’s oil could replace American imports of Russian crude, the top officials of the oil-producing province Alberta said this weekend.

As talks about banning Russian oil imports in the United States and its European allies intensify, reports have started to emerge that the U.S. Administration could be looking to persuade Saudi Arabia to pump more oil or lift some sanctions on Venezuela to help fill the gap that a Russian oil embargo would open.

On Sunday, U.S. Secretary of State Antony Blinken said that the United States and its European allies were in “very active discussions” about banning the import of Russian oil over Putin’s war in Ukraine.

Even without sanctions on Russian oil, some of the biggest U.S. importers of Russian crude oil have started suspending their purchases of the commodity.”

Gold futures made a new panic high of 2027.80. This may indeed be the Master Cycle high, as the next one isn’t due for two months. I will keep you posted. In the meantime, the EW pattern appears complete. Consider taking profits in gold at this time.