12:48 pm

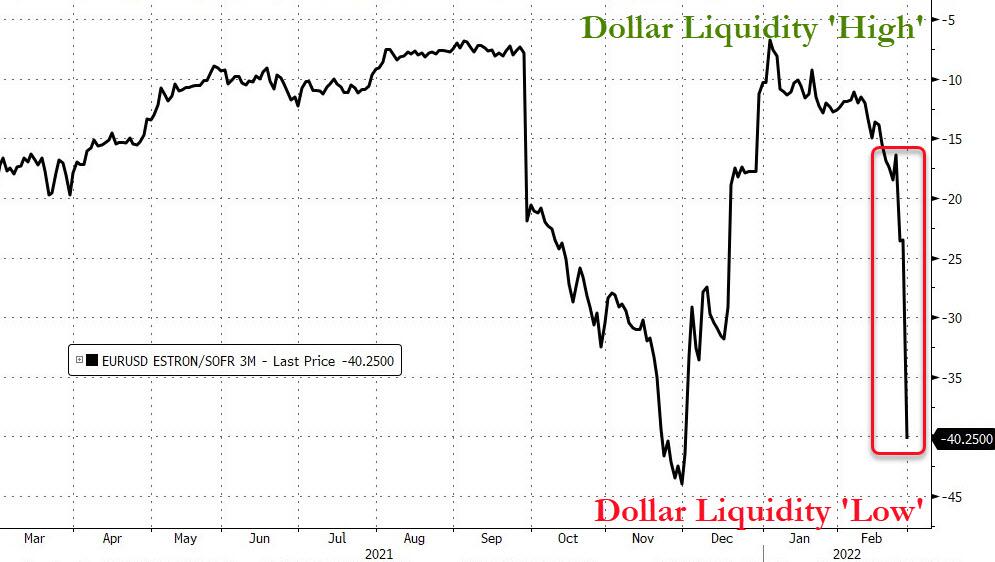

BKX is descending toward the Neckline of its Head & Shoulders formation at 126.25. As a proxy for liquidity, BKX shows cash exiting the markets to the point of being critical.

11:42 am

TNX has completed its correction down to the Lip of the Cup with Handle, making a bottom at 17.05. In doing so, it has bloodied the bond shorts. Today is day 263 of the Master Cycle, so there is not a lot more to be expected in this correction.

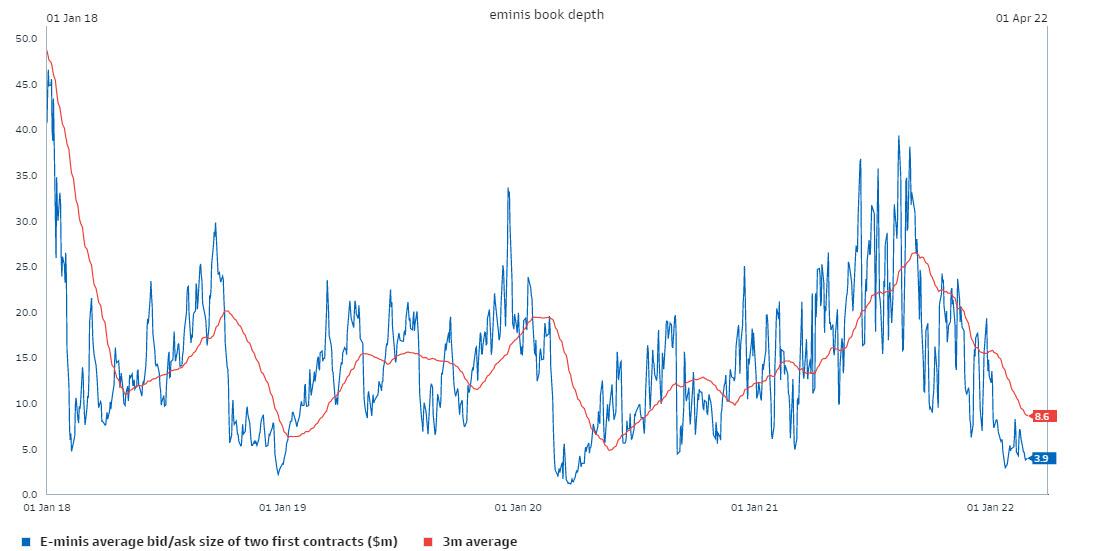

Zerohedge remarks, “With most traders glued to screens and following every tick in the chaotic mess that is the Emini, where liquidity has collapsed to levels not seen since the March 2020 crash…

… the real action is in bonds, where as Nomura’s Charlie McElligott writes in his morning note that we are seeing a “paradigm shift” in rates as a result of the spike in “unknown unknowns” from the Ukrainian war, which has prompted comments such as this one from the ECB suggesting that central bank normalization plans may have just died a gruesome death…

- *ECB SHOULDN’T EXIT STIMULUS BEFORE ASSESSING WAR IMPACT: REHN

and immediately following:

- *TRADERS DELAY 25BPS ECB HIKE BETS TO MARCH 2023 FROM JANUARY

… and which means that the market’s massive front-end short positioning – where “six or seven” rate hikes had become the market’s flawed baseline – is being VaR-shocked in full-blown stop-out fashion, leading to the EDZ2 +46 ticks from Friday low to this morning’s highs…

9:10 am

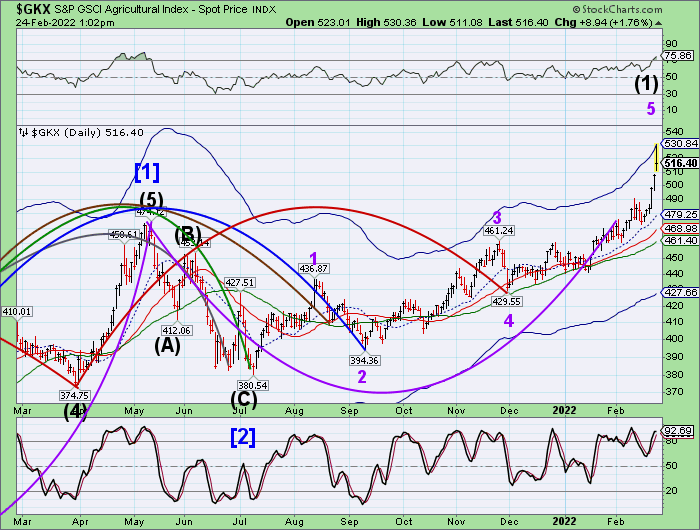

The GSCI Ag Index may present another golden opportunity to investors looking for an alternative to stocks. It is currently in a correction that has about another week to run before reversing higher. The weekly chart shows a proposed Head & Shoulders neckline at 474.00 with a proposed target at 696.00. Currently I have the corrective target at the 50-day Moving Average just beneath that. Of course, I will adjust the chart as the corrective decline is complete.

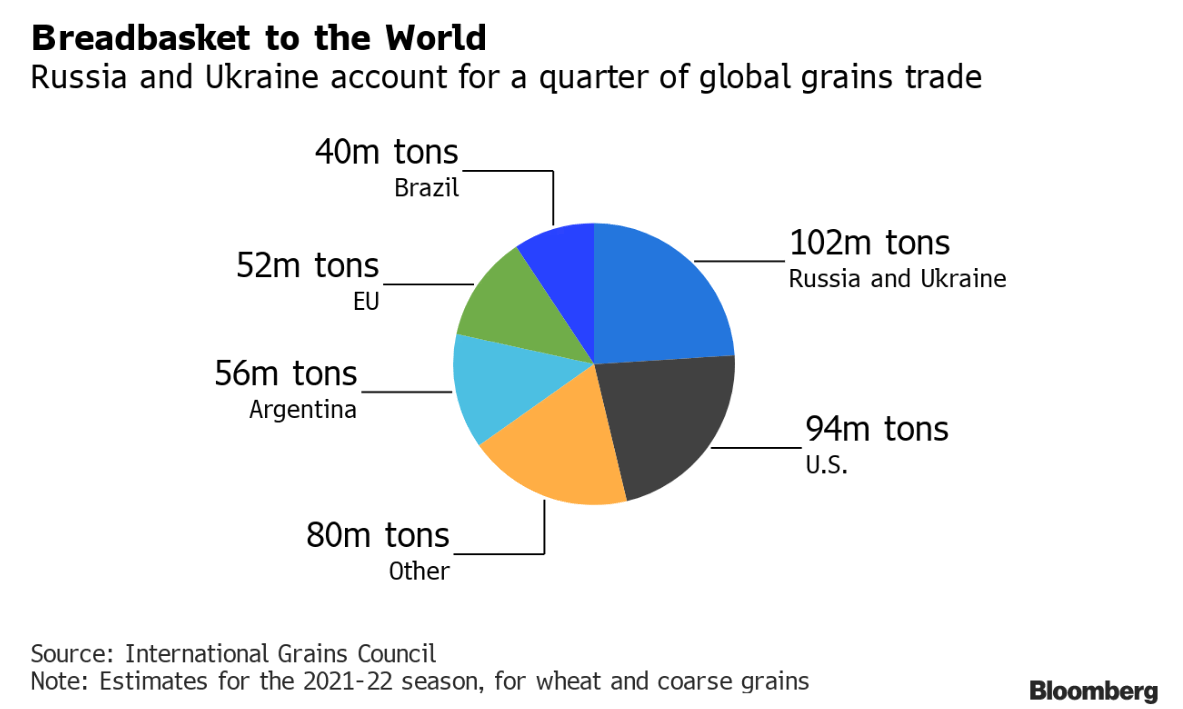

ZeroHedge reports, “Ukraine has earned the nickname “breadbasket of Europe” for its rich dark soil, vast wheat fields, and other farm goods. The Russian invasion has cut off the world from cheap and abundant wheat supplies.

Ukraine and Russia are vital to the global food supply, accounting for more than a quarter of global wheat trade, about a fifth of corn, and 12% of all calories traded globally, according to Bloomberg.

Reuters reports Ukrainian ports will remain closed until the Russian invasion ends and maritime security is restored for commercial ships. ”

ZeroHedge further observes, “China’s top economic planner, the National Development and Reform Commission (NDRC), announced Monday to “immediately” increase pork stockpiles around the country after prices fell last week, according to Bloomberg.

NDRC said the country’s staple meat stockpiles are being replenished as an index monitoring pork prices slipped below a critical threshold. The national average of pork prices against grain prices index registered 4.98 to 1 between Feb. 21 and 25, falling below the 5 to 1 ratio. The ratio signals the need for China to increase pork supplies.

Hog prices are back to levels not seen since before the African swine fever ravaged pig herds across the country, right before the virus pandemic.”

8:10 am

Good Morning!

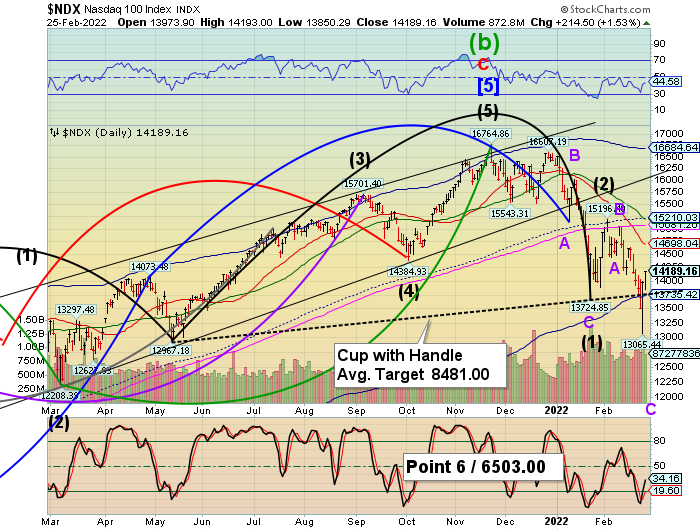

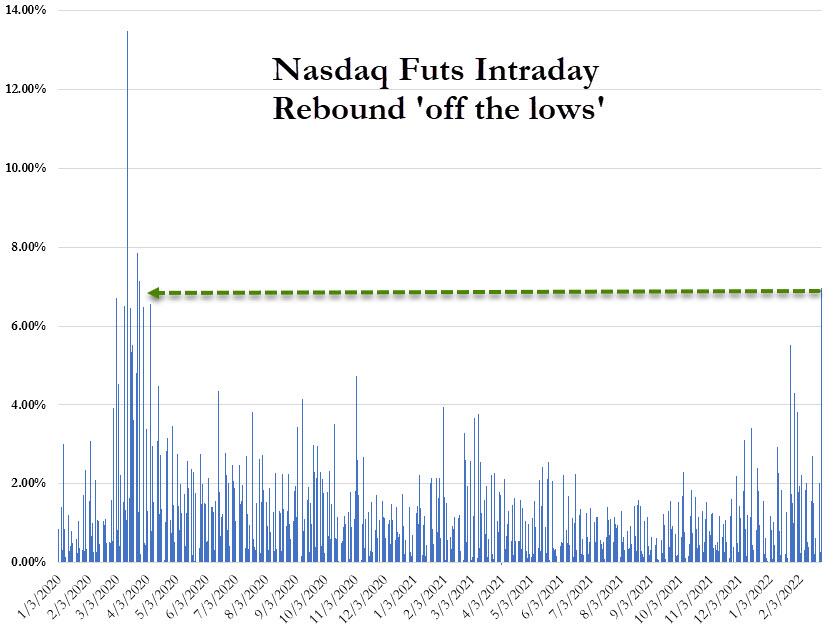

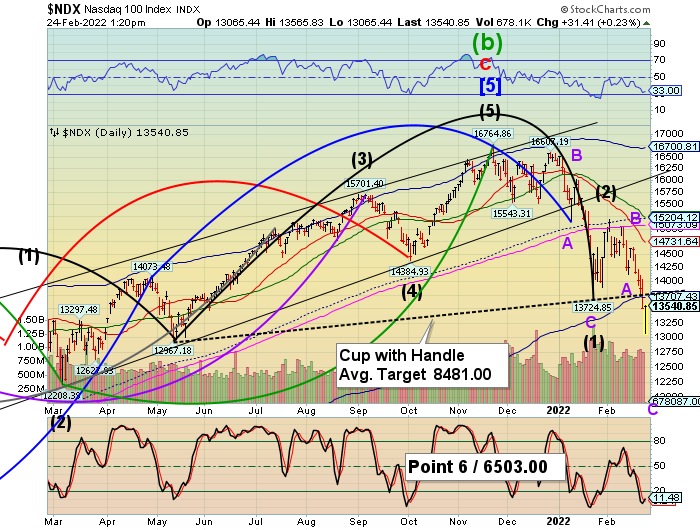

SPX futures reached a morning low of 4326.90, then mad a weak bounce. Yesterday’s melt-up at the end of the day reflected the need for dealers to close in neutral territory. Tomorrow’s Max Pain zone is at 4340.00 with expiring options being positive above 4350.00 and negative beneath 4300.00. Continued pressure from the Ukrainian conflict and with Powell on the docket tomorrow, things may get rather dicey. The Cycles Model is poised for a major low on Friday, but with follow-through over the next two weeks.

ZeroHedge reports, “In a mirror image of yesterday’s overnight bounce, S&P futures and European markets have slumped to session lows as a risk off mood prevailed as US traders got to their desks having hit overnight highs of 4,399 just before the European open, as mood soured after the conflict in Ukraine intensified amid mounting penalties against Russia, and as participants look to a heavy data-docket ahead and Fed speak including Powell later in the week.

Any residual optimism was shattered after Ukrainian President Zelensky said that negotiations with the Russian side have not achieved required results while Russian Defense Minister Shoygu says Russia will continue operations in Ukraine until it achieves its goals. As a result, Nasdaq 100 contracts were down 0.9% as of 7 a.m. in New York after the cash index closed yesterday’s session with its second straight monthly decline, a trend not seen since October 2020. S&P 500 futures declined 0.7% or 30 points to 4,337 while Dow futures fell 0.7% or 230 points, reversing much of yesterday’s last hour ramp. Stocks trading in Moscow remained halted for a second day, and the VanEck Russia ETF plunged another 12%. Treasury yields fell for a second day to the lowest since January, and the dollar was steady. Brent crude jumped more than 5% as traders balanced the possible release of emergency stockpiles against fears of disruption to Russian energy exports.”

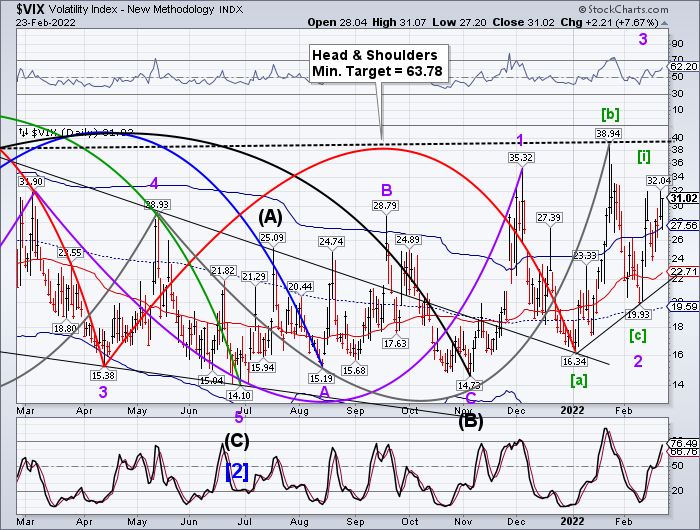

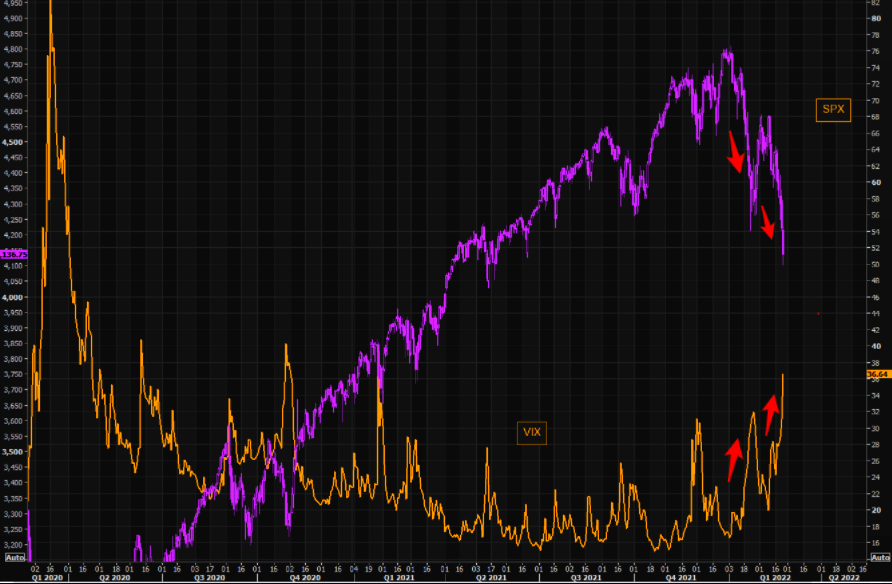

VIX futures made an overnight high of 32.42, still within yesterday’s trading range. It is using the Cycle Top support as its base, a sign that Wave [iii] of 3 of (C) of [3] may be underway. The reason I bring this up is that is a lethal combination for stocks. Sadly, no one is paying attention that the VIX may go much higher.

TNX fell to 17.31 this morning as storm cloud gather. Last week I had mentioned that the neckline would be a possible target for Wave 2. Today is day 263 of the current Master Cycle and this may be an appropriate end of Cycle. It is likely to be on a buy signal at the end of the day.

USD futures rose to 97.20 this morning, still within yesterday’s trading range. There are three more weeks left in this Master Cycle, as USD ventures toward the 61.8% retracement at 98.30. From there, it may become evident that our current powers-that-be have destroyed the USD as the world’s reserve currency.

ZeroHedge observes, “The war being waged by Russia in Ukraine shows no signs of coming to any type of peaceful end.

Meanwhile, it appears to me that a separate war on the U.S. dollar could be “officially” waged at any moment, by Russia and China collectively, as the situation in Ukraine grows more dire, as Russia’s options wane and its ties with China grow closer.

While the hope is still to avoid a World War III type scenario, escalating sanctions from the West are forcing an increasingly unhinged Vladimir Putin to consider his options for pushback.

For example, on Sunday, Putin put nuclear deterrence forces on high alert as a response to increasing pressure from NATO, in a move that the U.S. ambassador to the United Nations said “escalates the conflict unacceptably.”