1:29 pm

SPX has bounced near its 50-day Moving Average at 4037.78 and has tested the trading channel at 4082.61. It is now headed lower. The first support that may halt the decline is the 200-day Moving Average at 3962.31. Another support just as likely to create a bounce is the 2-hour Cycle Bottom at 3931.41. Those two supports provide the likely range for the next installment of the decline.

10:40 am

VIX is now on a confirmed buy signal, having exceeded the 50-day Moving Average at 19.89. The rally may continue until mid-June.

10:20 am

The Ag Index made a probable throw-under yesterday, having met its long-term target of 424.00. It may be on an aggressive buy signal with probable confirmation above the Cycle Bottom at 436.98. Should that be so, GKX may be on a likely rally to the end of June. Trending strength comes into play this weekend and may last all next week.

The Netherlands are under intense pressure to curtail their highly productive farms to reduce dubious emissions.

ZeroHedge reports, “Rice is the primary food source for over half of the global population, especially in emerging markets, where it plays a crucial role in feeding people. Last year, we highlighted the potential for a severe global rice shortage. A new report reveals that rice production this year could be at its lowest in decades.

A report by Fitch Solutions forecasts this year’s global rice production will log its biggest shortfall in two decades. The deficit will be a major headache for countries relying on grain imports.

“At the global level, the most evident impact of the global rice deficit has been, and still is, decade-high rice prices,” Fitch Solutions’ commodities analyst Charles Hart told CNBC.

ZeroHedge infers, “Dozens of experts were asked to look into the science behind claims that meat eating causes disease and is harmful for the planet in a special issue of a journal called Animal Frontiers. They have warned against a widespread societal push towards plant-based diets, arguing that poorer communities with low meat intake often suffer from stunting, wasting and anemia driven by a lack of vital nutrients and protein.

Thousands of scientists across the globe have also joined The Dublin Declaration, a group stating that livestock farming is too important to society to “become the victim of zealotry.” They say that many of the negative claims about meat in our diet are simply not true.”

9:57 am

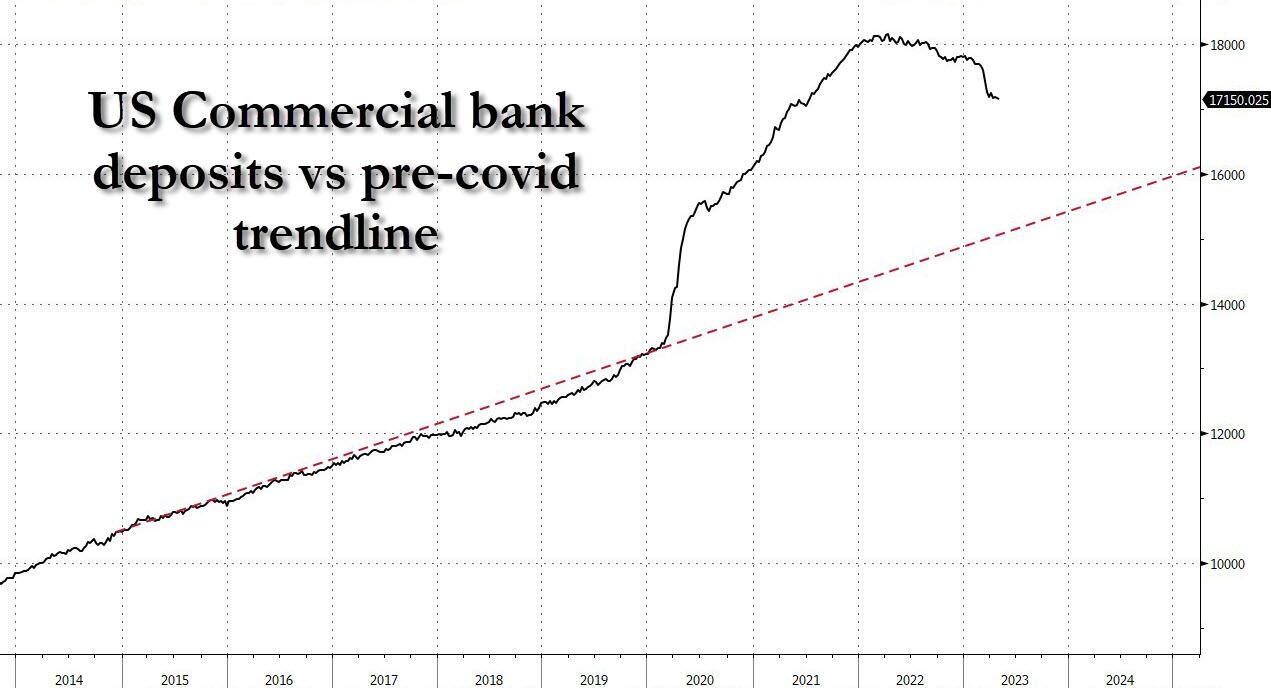

BKX, our liquidity proxy, is making a deeper low this morning. The Cycles Model suggests the downtrend may continue to mid-June. Trending strength may intensify this weekend, adding to a n already panicky trend.

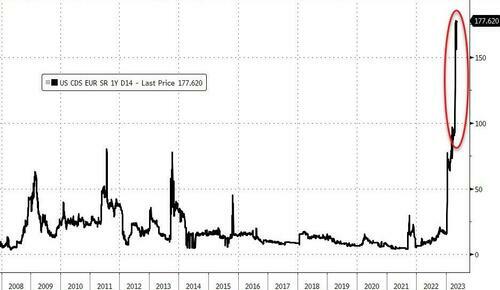

ZeroHedge observes, “First Horizon Corp. shares crashed in premarket trading after Toronto-Dominion Bank published a statement outlining how a deal to purchase the Memphis-based bank has been “terminated.” The announcement comes after multiple regional banking failures.

The lenders said they both “entered into a mutual agreement” to terminate their originally announced merger agreement, announced on February 28, 2022. TD said it “does not have a timetable for regulatory approvals to be obtained for reasons unrelated to First Horizon. Because there is uncertainty as to when and if these regulatory approvals can be obtained, the parties mutually agreed to terminate the merger agreement.”

Under the terms of the termination agreement, Canada’s second-biggest bank will make a $200 million cash payment to First Horizon on top of a $25 million reimbursement payment.

As a result of the termination, shares of First Horizon plunged 52% in premarket trading.”

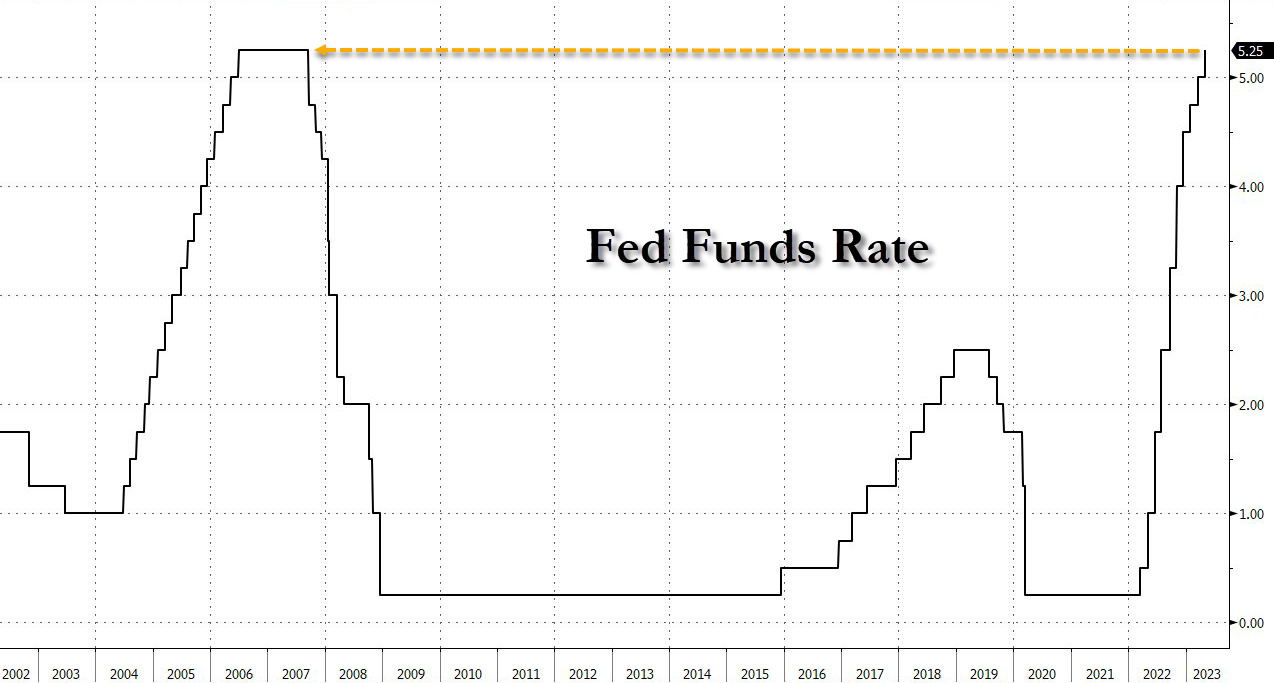

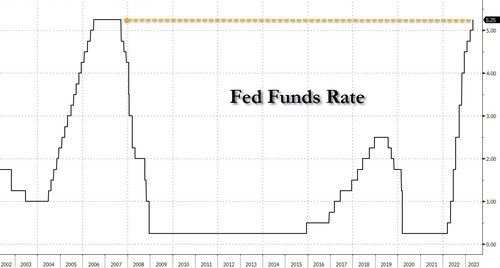

ZeroHedge exclaims, “Earlier today, when Jerome Powell openly lied to the American People during the FOMC press conference stating without a hint of irony that the US banking system is “sound and resilient”…

…we balked: how could this former lawyer lie so brazenly to the American people, the narrator wondered, when in just the past few weeks we had seen over half a trillion in bank failures, making the current bank failure episode even worse than the global financial crisis?”

8:00 am

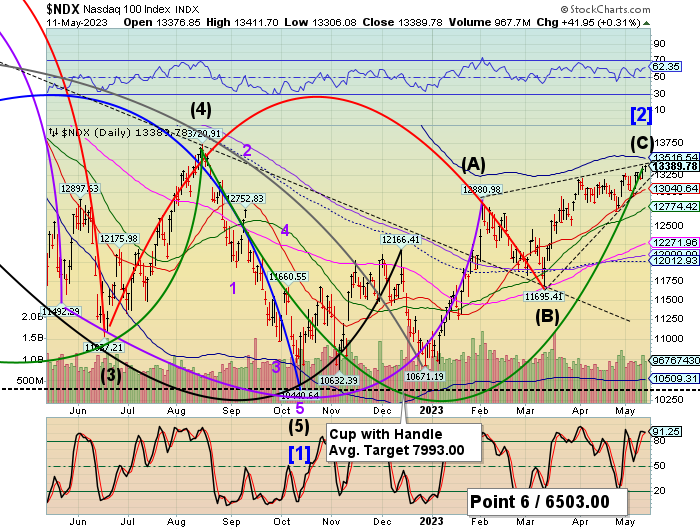

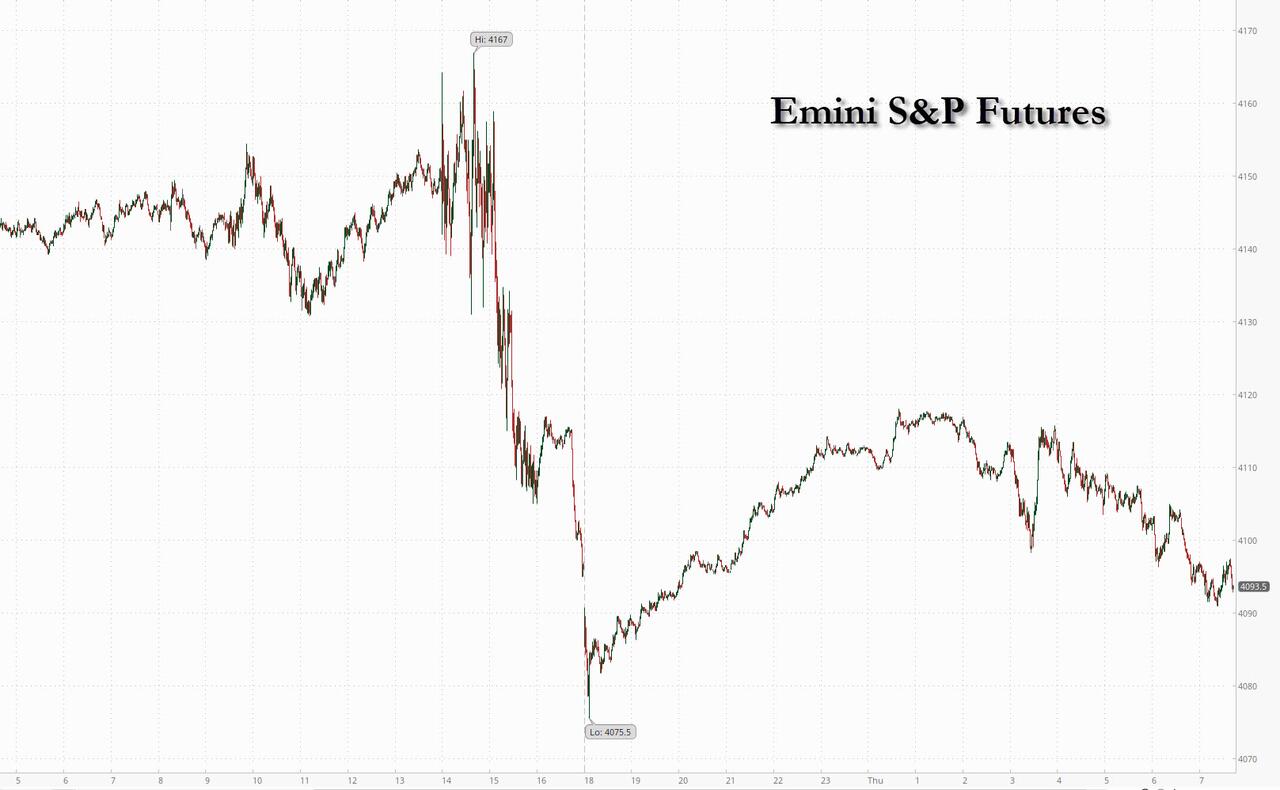

NDX futures probed lowser to 12978.70 before rising back to the flat line. While dealers and hedge funds do their best to maintain a tight trading range in NDX, bad news may jolt it off its perch. Once the decline gathers momentum, it may continue to the end of June. The decline may have the same magnitude as the August-to-October decline, starting with a lower top.

In today’s options expiration, 13000.00 is a hotly contested strike. Long gamma begins in earnest at 13120.00, while short gamma starts at 12930.00 and runs to 12800.00. The options market appears to be teetering toward short gamma.

ZeroHedge notes,”Fed raises rates by 25 bps as expected.

Policy statement softens the rate guidance in a way consistent with past pauses and The Fed deletes reference to “some additional policy firming may be appropriate.”

A clear hat-tip to the banking crisis:

“Recent development are likely to result in tighter credit conditions” removed and replaced with “Tighter credit conditions”

The decision was unanimous.

As WSJ Fed Whisperer Nick Timiraos notes: “The FOMC statement used language broadly similar to how officials concluded their interest-rate increases in 2006, with no explicit promise of a pause by retaining a bias to tighten.”

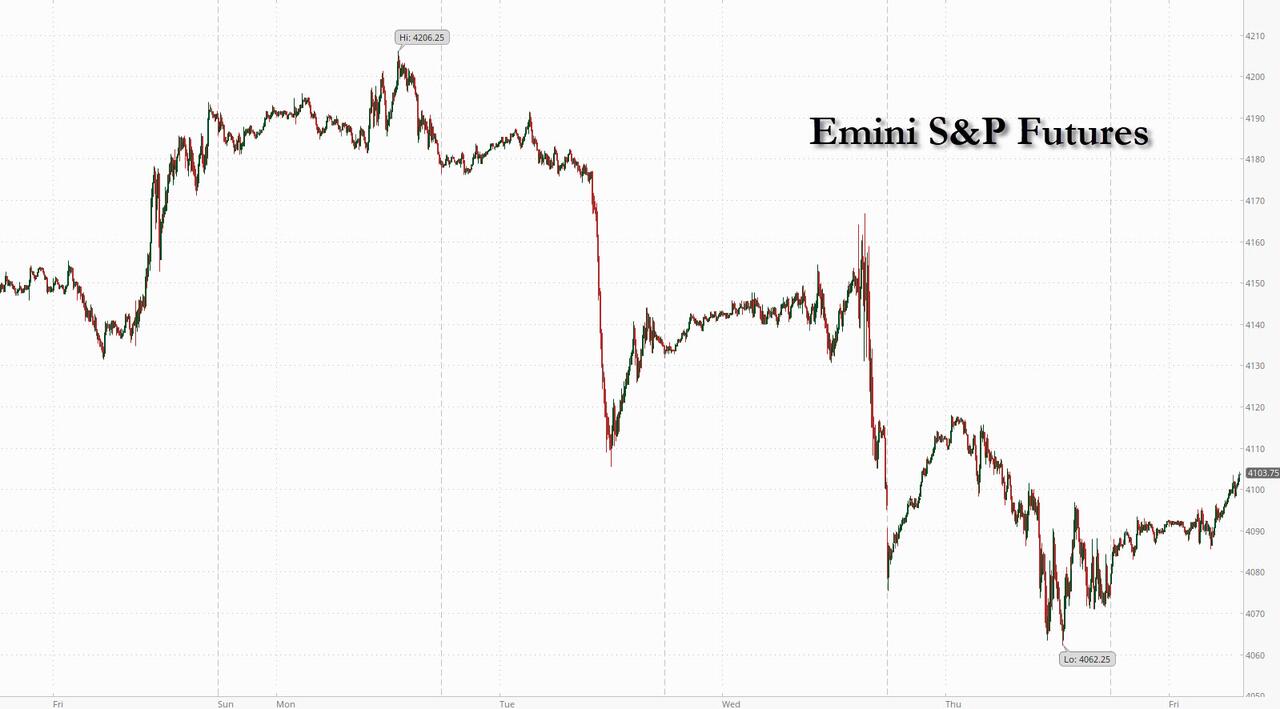

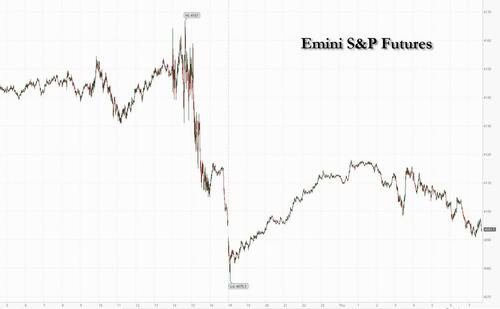

SPX futures declined through Intermediate-term support at 4073.95 this morning, testing short gamma and potentially confirming the aggressive sell signal made on Tuesday. The Cycles Model shows a probable sell signal until the end of June, with rising volatility along the way.

Today’s op-ex shows the 4110.00 strike hotly contested. Long gamma begins at 4130.00, while short gamma is in control beneath 4075.00.

ZeroHedge reports, “US stocks were set to open lower, reversing a modest gain earlier and extending a three-day selloff as investors weighed the possibility of more bank failures against a pause in rate hikes by the Federal Reserve as growth slows. Contracts on the S&P 500 were down 0.3% as of 7:45 a.m. ET while Nasdaq 100 futures were flat. The benchmark S&P 500 had slid on Wednesday, marking its longest losing streak in nearly two months even as the Fed signaled a possible pause in its most aggressive tightening campaign in decades. Sentiment was routed as US regional banks tumbled further even after PacWest said its deposits rose since March and confirmed a Bloomberg report that it’s talking with potential investors in a bid to calm markets. The stock slumped as much as 45% premarket. And Western Alliance was down 23%, though it claimed it hasn’t seen unusual deposit flows.

VIX futures rose to 19.63 this morning, with a likely test of Tuesday’s high at 19.81. The new Master Cycle may run to mid-June, with a possible extension through the end of June.

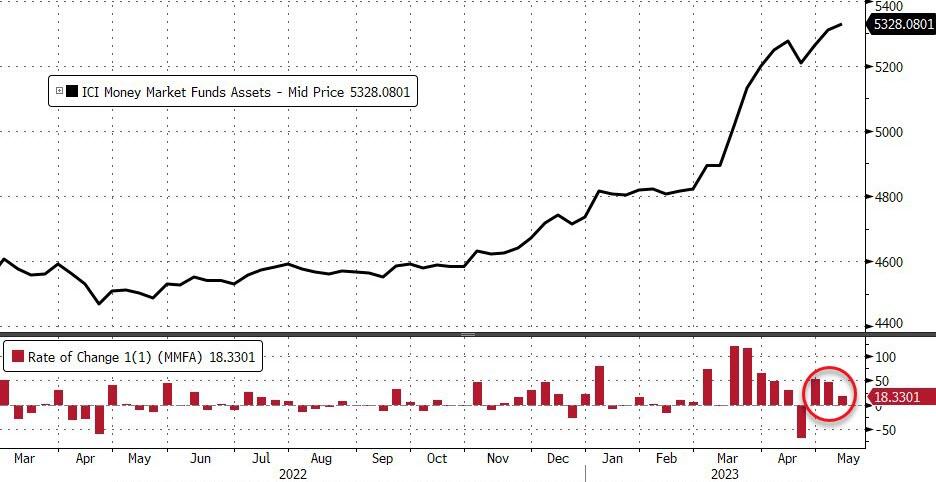

YahooFinance observes, “(Bloomberg) — For all the angst over US banking stress and a profit recession, none made it to the surface of the stock market in April.

Most Read from Bloomberg

Calm prevailed, with the Cboe Volatility Index ending the month below 16 for the first time since November 2021. The gauge, a measure of options costs also known as the VIX, slipped for six straight weeks as the S&P 500 endured its least turbulent month in almost four years.

As eerie as the market peace looked, it was the result of aggressive forces balancing each other out beneath the surface. Examples included the violent rotation between technology and financial stocks, and the collapse in lockstep moves among individual shares that sent correlation to a 17-month low.”

TNX made a brief throw-under of the trendline at 34.00 this morning as it seeks to rise back above it. Should it succeed, the uptrend may resume, confirmed above the 50-day Moving Average at 36.12. The new Master Cycle may continue to early July.

ZeroHedge warns, “The full force of the rate-hiking cycle is about to be felt across the economy as the Federal Reserve pulls back from warehousing duration risk, leaving the private non-bank sector acutely exposed to higher rates, and credit spreads prone to significant widening.

There has been no shortage of surprises in this cycle. For one, it is remarkable that despite the fastest series of rate hikes for decades, equities are less than 15% off their highs, the VIX is little changed from when the bear market started, and credit spreads are not wider.

But, like a cyclist at the front of a peloton, the Fed has been shielding the economy from the full, and mounting, headwind of higher rates.”

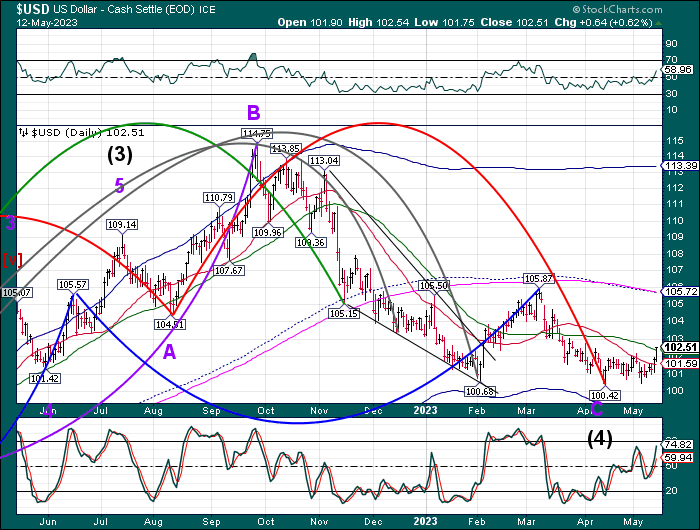

USD futures made a marginal new low at 100.80 before reversing higher this morning. A rise above Intermediate-terms resistance at 101.88 confirms the buy signal that may last to mid-June.

Crude oil futures plummeted through the Cycle Bottom support at 68.20, to a morning low at 63.70. he next target may be the weekly Cycle bottom at 53.11, just beneath the 61.8% retracement of the rally from April 2020 to March 2022, potentially also completing a 12.9-month declining Cycle. The Cycle may be done in 2-3 weeks. Traders are already calling for a bottom. It won’t likely happen until those voices are silenced.

ZeroHedge observes, “Oil – keep it simple?

Trading the range in oil requires a mean reverting mind. Buy when it feels like oil is breaking down, and sell/short when it feels like things are about to break up. We are in the lower part of the range and seeing the first up candle in a while…

Source: Refinitiv

Oversold

Oil is very oversold here. Last time we had similar readings of the RSI, things bounced aggressively…

Gold futures extended their Master Cycle high to 2082.80 this morning, on day 267. It did not exceed the August 2020 high at 2089.20. A further challenge may be possible, but time is running short for a new high. Should the current Master Cycle be complete, the new MC may produce a decline to the middle of June.