8:15 am

Good Morning!

NDX futures bounced from the Intermediate-term support at 12948.00 to the 38.2% retracement level this morning at 13073.60 thus far. The Cycles Model and Elliott Wave structure both agree that a much larger decline is now due. The next support is the 50-day Moving Average at 12656.05.

Today’s op-ex shows Maximum Pain at 12825.00. Long gamma starts at 12850.00, while short gamma begins at 12800.00.

ZeroHedge anticipates, “After a tsunami of earnings and major economic and policy releases, including rate hikes by the Fed and ECB, a barrage of earnings culminating with Apple, the week is almost over, we just have one more event to go: Friday’s jobs report. So here is a look at what street consensus expects.

- Nonfarm Payrolls: +185k median headline, down from 236k, analyst forecasts range from 125k-270k. This compares to the 3-,6-, and 12-month averages of 345k, 315k, and 345k, respectively. According to Newsquawk, 185k would mark a cooling in the growth of the labor market to levels more consistent with pre-COVID trends, coming down from extremely hot levels.”

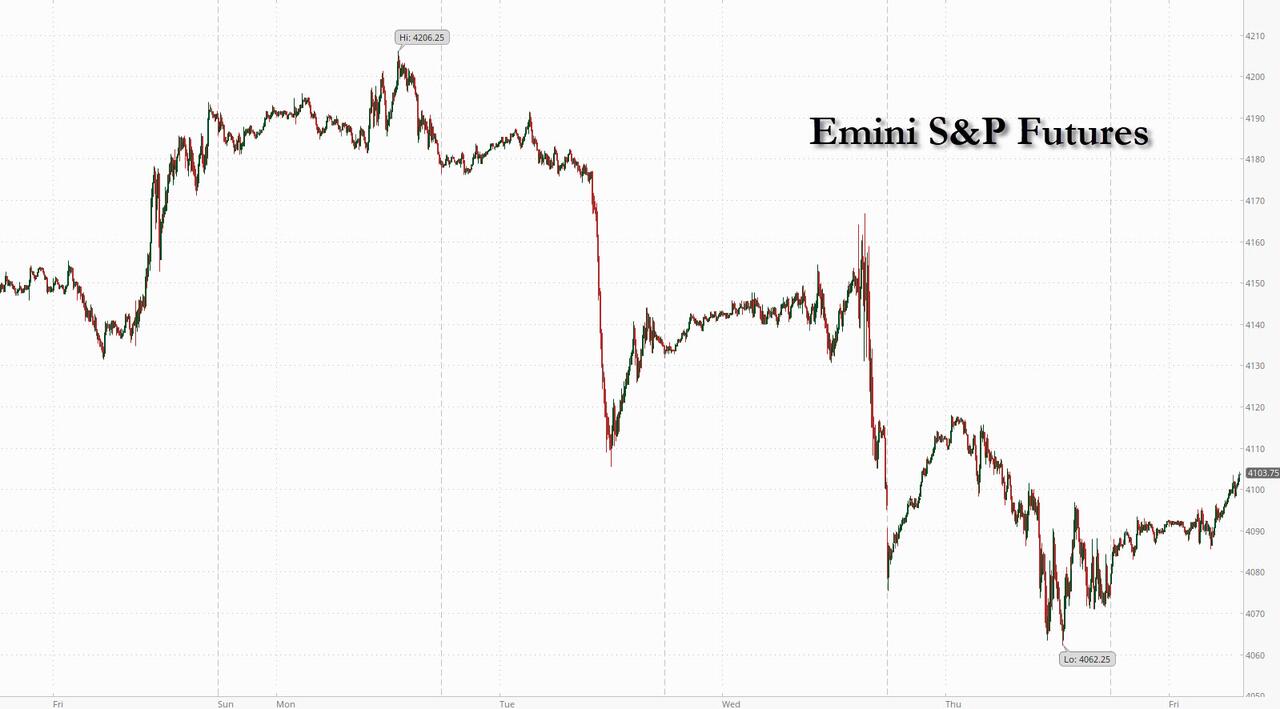

SPX futures rose to a morning high of 4092.00 thus far, a 32% retracement. So far, the retracement has met the short-term trendline (not shown), but no further.

In today’;s op-ex, the 4100 strike is hotly contested, with over 7000 puts and calls contracts. Long gamma begins at 4120.00, while short gamma may start at 4075.00.

ZeroHedge reports, “US futures entered the last day of a brutal week in the green ahead of key US jobs data, as regional banks clawed back some of their recent selloff, even as the S&P 500 benchmark was still poised for its worst weekly performance in almost two months. The S&P 500 contracts climbed 0.7% as of 7:30 a.m. ET while Nasdaq 100 futures gained 0.6%. European stocks were higher but on pace for their biggest weekly drop in 7 weeks. Treasury yields are ticking higher amid a more risk-on day, while the dollar is still weakening on recession risks and a potential pause in interest rate hikes. Oil is staging a rebound, though is still set for the worst week since mid-March, continuing its third weekly decline. Meanwhile, gold is headed for its biggest weekly advance since the middle of March, up around 2% this week, as traders look for havens. Iron ore slides, while copper is little changed.”

VIX futures declined to a morning low of 18.39 as it retraces 50% of its rally. The retrace may be short-lived as trending strength comes back next week.

The May 10 op–ex shows long gamma starting at 15.00 and extending to 47.50.

ZeroHedge comments, “Ahead of today’s jobs report, which we previewed earlier and where median consensus expects a drop in payrolls to 185K (which would be the lowest since 2021) with unemployment rising to 3.6%, many joked that at this point the job report is so rigged and “adjusted” that Biden’s Dept of Labor may as well just keep going with fabricated numbers until the 2024 election. After all, one look at the chart below which shows the number of consecutive beats confirms what a farce the “data” has become: everything in the name of a beat and a favorable press conference soundbite.

Well, the cynics were right once again because moments ago the BLS reported a record 12th consecutive month of payrolls beating expectations…”

TNX jumped this morning, reversing the probe beneath the trendline and testing Intermediate-term resistance at 34.73. The reversal above the trendline has created an aggressive buy signal for TNX and a sell signal for UST. The Cycles Model suggests the new trend may continue until early July. Economists are projecting the future with rulers again.

ZeroHedge observes, “There’s nothing quite like a non-farm payrolls report to stir the markets’ imagination. But the April edition will be largely beside the point for traders who are focused on the banking sector, where the angst of March is, to some degree, being rekindled.

Economists reckon that US employers continued to expand their payrolls, an unbroken run since the start of 2021, but at a far slower pace than in March. If the number comes in anywhere near the forecast 185k and the jobless rate is somewhere around the estimated 3.6%, the Fed would take it as confirmation that the labor market continues to be strong and withstanding the stress from the more-vulnerable pockets of the economy.

A number that is somewhere around the consensus is unlikely to persuade the Fed, which has already raised rates by 500 basis points in this cycle, to tighten again in June.

In other words, Treasuries are unlikely to move a whole lot even on a glowing report.”