8:00 am

Good Morning!

A weekly chart serves us best at this juncture. The reason is that NDX just rose to the 61.8% Fibonacci retracements level (14324.71) of the 2022 decline on May 26. To that extent, it has met a common retracement level for a Primary Wave [2]. In addition, on Wednesday it will have complete 18.5 months since its November 22, 2021 high on Wednesday.

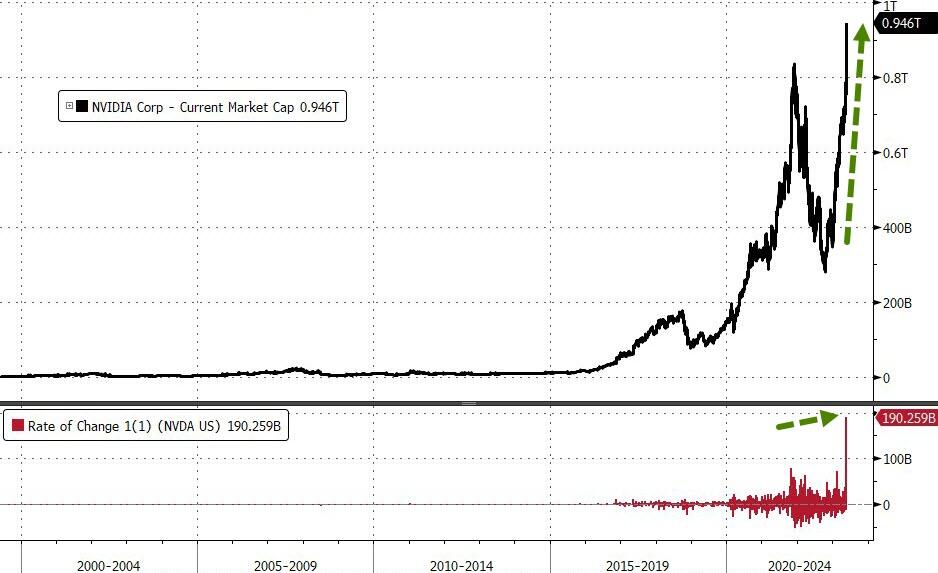

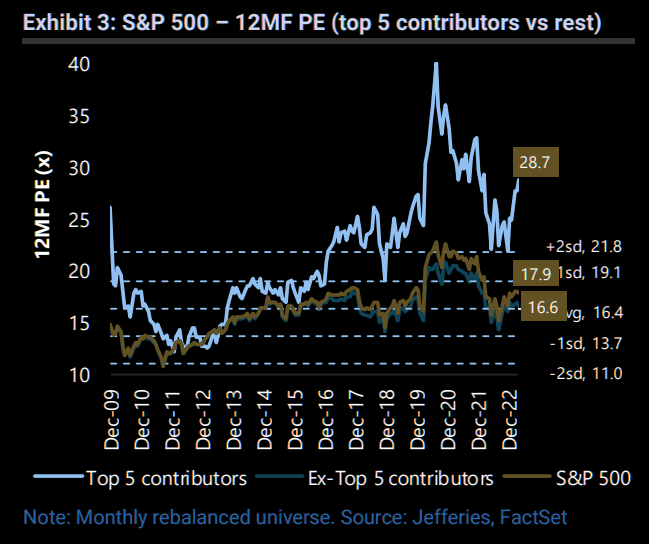

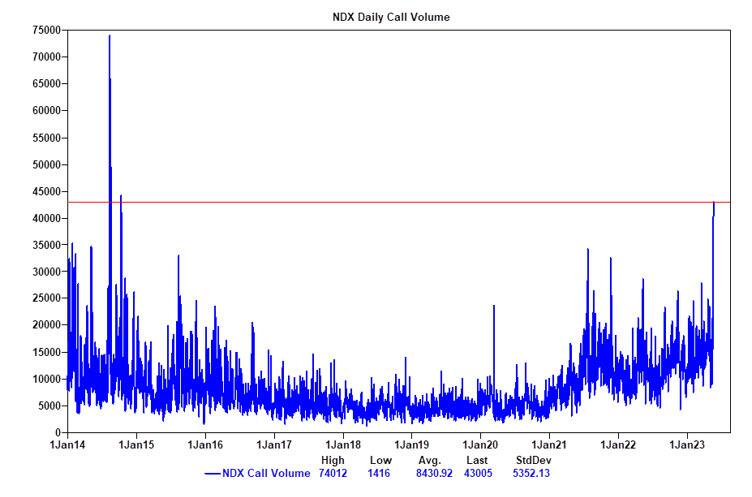

NDX futures are lower this morning, but within Friday’s trading range. Having met its 61.8% retracement level, it may simply go higher until the Cycle is complete later this week. NDX is in throw-over, due to a very small number of AI “generals.”

ZeroHedge remarks, “Extremely narrow breadth has historically led to further index upside.

As discussed in my previous post, it is not inconceivable (but still unlikely) that the recent zeal for AI could avert a US recession.

Whether it does or not is really moot as an investor, what’s important is asset performance.

And on that basis, the AI rally is on more solid ground.

In short, narrow leadership often creates its own reality and ends up dragging the rest of the market along with it.

That’s may happen this time too.”

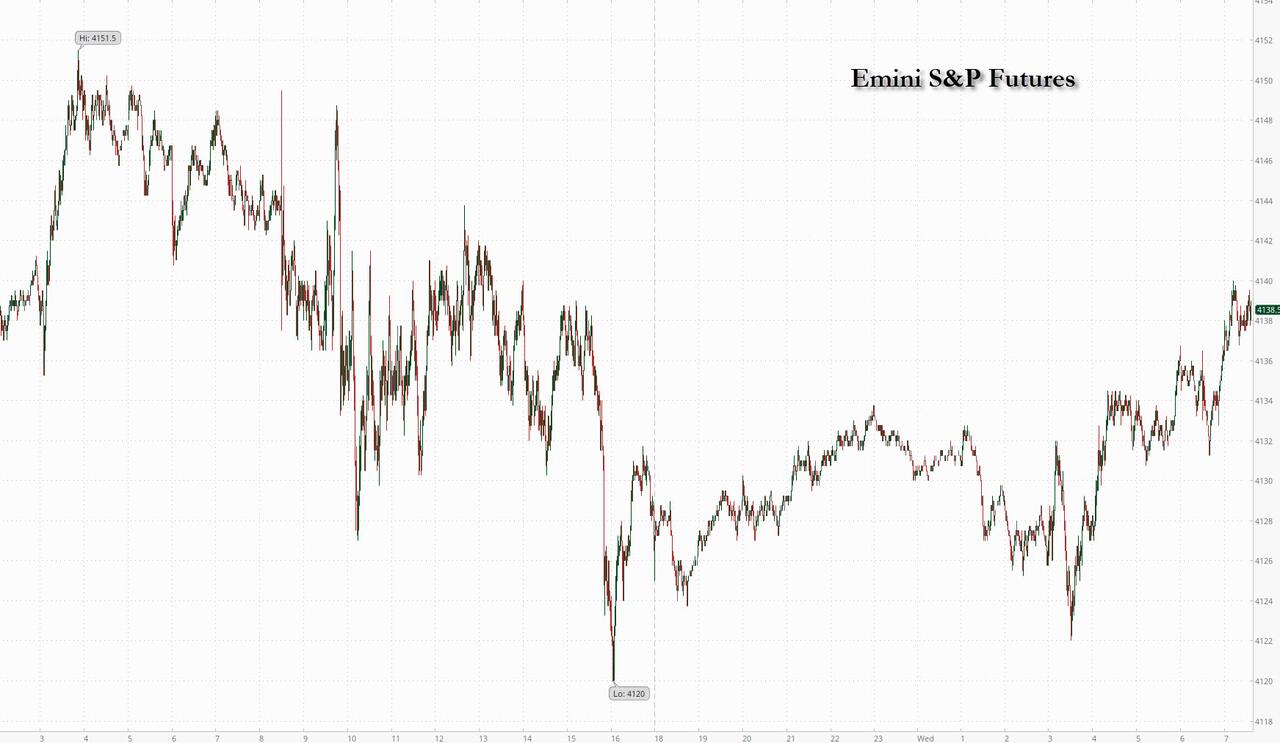

SPX futures are flat this morning. The 17.2-month Cycle from January 4, 2022 may complete by Friday. The 61.8% Fibonacci retracement level is at 4311.00. A reversal from the cycle Top at 4280.00 may produce an aggressive sell signal. Confirmation of a sell signal lies at Intermediate-term support at 4147.43 or the 50-day Moving Average at 4121.67.

In today’s op-ex, Maximum Pain for options investors is at 4265.00. Short gamma may begin at 4260.00. Long gamma may begin at 4285.00.

ZeroHedge reports, “Futures are flat with oil jumping after OPEC+ cut output by an extra 1mm bpd in a unilateral move by Saudi Arabia taking its production to the lowest level for several years.At 7:30am ET, S&P futures were flat, while Nasdaq futures were down 0.2% with some artificial-intelligence exposed stocks like Nvidia Corp. and C3.ai Inc. trading down. In contrast, Apple Inc. surpassed its previous closing record in premarket ahead of what’s expected to be its most significant product launch event in nearly a decade. Oil rose 2%, with oil giants such as Chevron and Exxon up in premarket trading. The Bloomberg dollar index is up as are 10Y yields now that the market’s attention turns to the $1+ trillion deluge in new debt issuance. Gold dropped, as did bitcoin after the crypto currency got its usual Asian session rugpull.”

VIX futures rose this morning after potentially making its Master Cycle low on Friday, on day 266. The new Cycle low came through a rare and complex W-X-Y-Z extension adding a full month to the already massive Triangle formation, creating a 17.2-month Cycle. VIX short players are ecstatic while commentators are viewing this as bullish for equities.

In Wednesday’s op-ex, Maximum Pain is at 16.00. Short gamma is virtually non-exixtent, while long gamma begins at 17.00 and rises to 50.00.

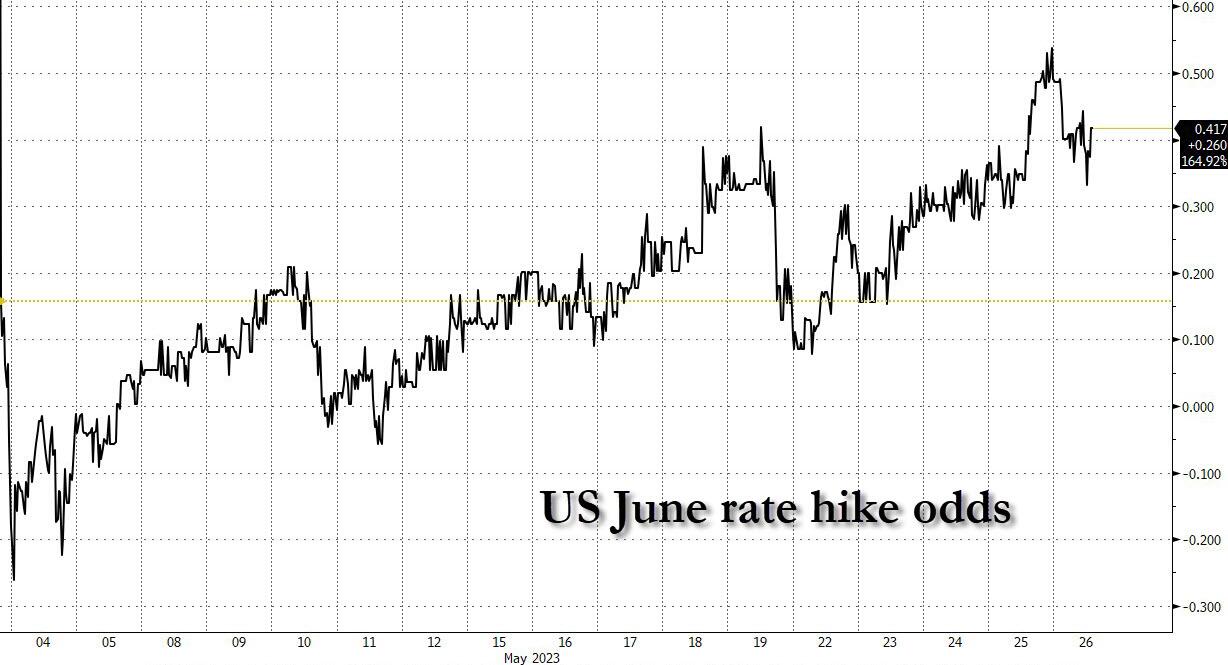

ZeroHedge notes, “It turns out the bulls had every right to be Dancing in the Street as stocks posted a very strong week (even the Russell 2000 and Regional Banks participated). Friday’s jobs data seemed to put the nail in the coffin on rate hike fears. The market has decided, rightfully so, that we are almost done with rate hikes and unless we get disastrous inflation data, any future hikes will be small enough not to act as a headwind.”

TNX leaped above the mid-Cycle resistance at 36.77 this morning, on its way to the Cycle Top resistance at 41.23 in the next month.

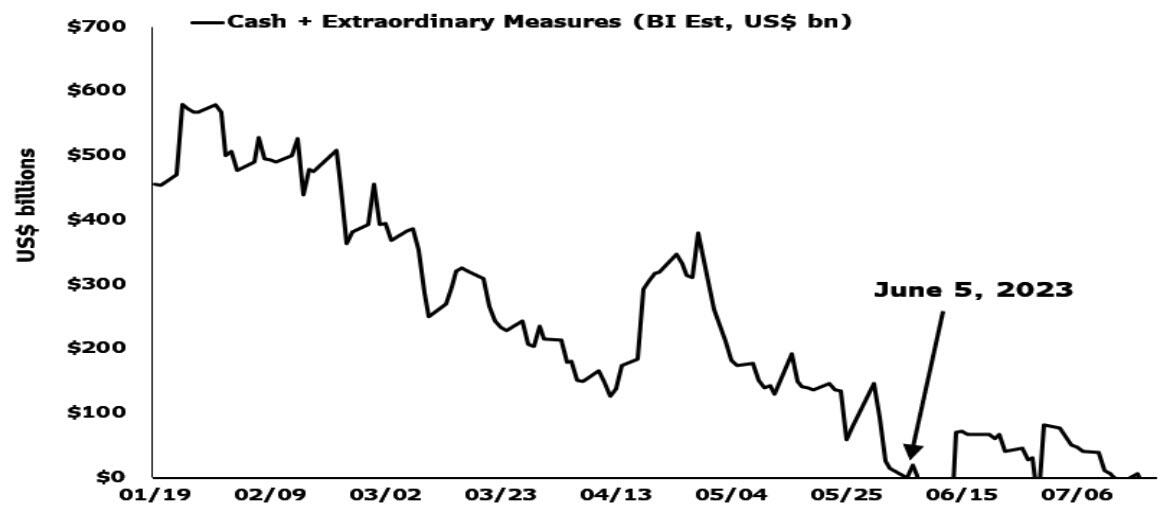

ZeroHedge comments, “As the latest debt-ceiling drama winds down, Americans are varyingly exasperated, angered, anxious and maybe even a little bit entertained by the spectacle.

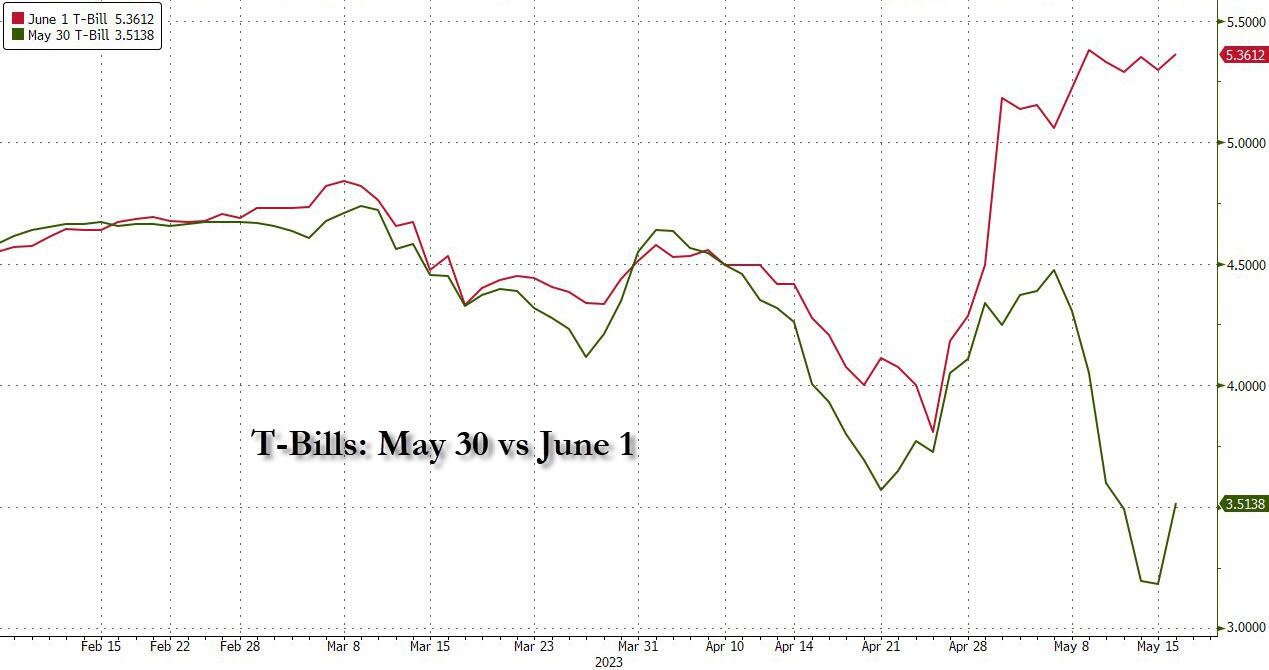

While their emotions vary, most citizens have something in common: They don’t realize they’re being misled about the actual depth of their government’s financial disorder. Despite all the talk of the federal government hitting a Congressionally-set $31.4 trillion debt limit, the truth is that DC’s actual liabilities are far higher than even that disturbing number.

Estimates by the relatively few scholars and organizations who venture to expose Washington’s charade vary, but they overwhelmingly place the federal government’s true total obligations at over $100 trillion. For example, Truth In Accounting’s latest tally puts Uncle Sam’s total IOUs at $156 trillion.”

USD futures rose to 104.35 this morning. The Cycles Model suggests another week of rally prior to a retracement. The immediate target appears to be the mid-Cycle resistance at 105.31. While USD may overshoot its target, it may end up back beneath it in the next few weeks.

WTIC futures may bise to test the 50-day Moving Average at 74.54 this morning, adjacent tot he trendline. Should it succeed in overcoming that resistance, the trend may change to the positive. However, should it be repelled, the decline may resume for as long as seven more weeks. Thus far in the current Cycle, the daily Cycle bottom at 67.06 is holding. However, a resumption of the decline may send Crude Oil to a possible low of 54.00.

Gold futures are lower this morning, caught in a corrective pattern that may end back near the 50-day Moving Average at 1999.70 in the next week or so. The Cycles Model then calls for the decline to resume with the next Master Cycle going to the end of July.

ZeroHedge observes, “Most politicians have used the “Ukraine invasion card” to justify the massive inflationary burst in 2021-2023.

It does not matter if inflation was already elevated prior to the war.

Supply chain disruptions, demand recovery, wage growth… Many excuses were used to justify inflation, except the only one that can make aggregate prices rise in unison, which is the creation of more units of currency well above demand.

Inflationists will blame inflation on anything and everything except the only thing that makes all prices, which are measured in monetary units, rise at the same: Money supply growth rising faster than real economic output.”