12:16 pm

BKX made its Master Cycle high Thursday, on day 258. It may be in decline toward its 50-day Moving Average at 83.38, where it may bounce. I had commented earlier on a possible probe higher, but the odds of that are dramatically diminished. Investors may sell/short WTI or wait for the bounce to take action.

11:55 am

TNX may have reached its Master Cycle high today on day 259. The cash market high is 41.26 (futures high is 41.29). This is a confirmation of my trendline analysis, suggesting that 50.00 may be reached by mid-October.

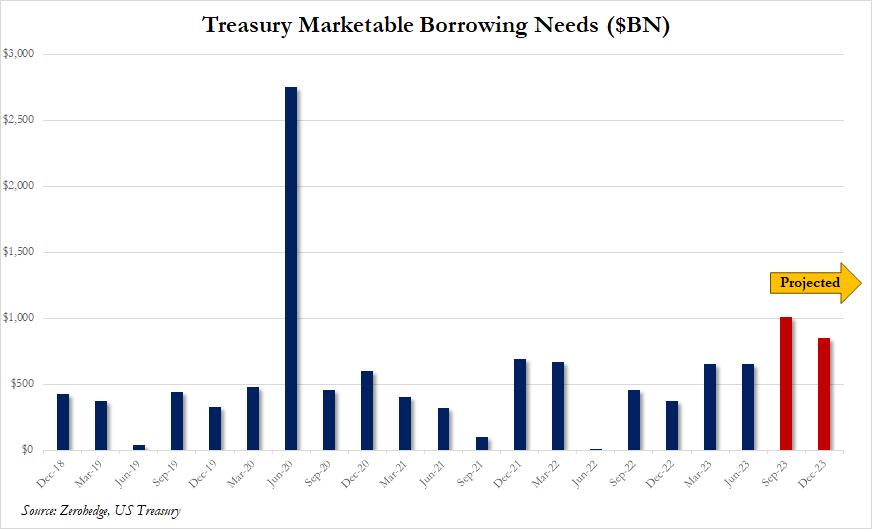

ZeroHedge reports, “We gave a big picture preview of the debt flood (and fiscal crisis) that is coming to the US this past Monday when, looking at the latest Treasury debt estimates, we showed that the US predicted a near-record $1 trillion in debt sales in the current quarter (up from $$733BN forecast previously) and $852 billion in Oct-Dec quarter, numbers so staggering they are usually associated with economic crises…

… but in this case a surge in debt issuance meant to sustain the illusion of the deficit-busting Bidenomics, which has managed to keep the US economy from imploding only thanks to massive new debt and deficit spending, or what BofA’s Michael Hartnett called “The Era Of Fiscal Excess”, something which Fitch finally realized last on Tuesday when it became only the second rating agency in history to downgrade the US AAA rating.”

10:17 am

GKX has broken its lower trendline, implying more decline is to come. The Master Cycle has another three weeks to complete it. The two possible targets are the 61.8% retracement at 387.76 and the Intermediate Cycle Wave (4) low at 380.54. While decreasing liquidity may be causing all asset classes to decline, the Ag Indes is the most likely to be the first to recover. It may be time to start accumulating shares of Ag-related commodities and businesses, even while the decline is in progress.

ZeroHedge observes, “In February of last year, the International Journal of General Medicine published a study that was easy to miss, as no major media publication reported on “Total Meat Intake is Associated with Life Expectancy: A Cross-Sectional Data Analysis of 175 Contemporary Populations,” by Wenpeng You and his team of researchers.

For years we have heard that the secret to a long life is to cut back on meat consumption and increase our intake of carbs—advice that is enshrined in the USDA’s Dietary Guidelines for Americans. But that’s not what these researchers found.”

ZeroHedge further reports, “Wednesday has witnessed major airstrikes on Ukrainian ports and the war-ravaged country’s food export infrastructure, which comes in the wake of Russia refusing to renew the UN-brokered Black Sea grain initiative at the end of last month.

Drones hit several sites before sunrise and through the early morning hours on Wednesday, including a major attack on Ukraine’s Danube port, sending global grain prices higher. A large fire engulfed some 40,000 tonnes of grain at the Danube location, according to Ukraine government sources.”

8:15 am

Good Morning!

NDX futures declined down to 15497.30 this morning, breaking beneath its 4-month trendline near 15700.00 and now being supported by Intermediate support at 15276.08. It remains on an aggressive sell signal with a confirmed sell signal Intermediate support. Most analysts consider a decline beneath the 50-day Moving Average at 14899.81 as a sell signal. The Cycles Model gives a higher confidence in an “earlier” signal.

Today’s op-ex shows Maximum Pain for options investors at 15760.00 with short gamma beginning at 15750.00. long gamma is fading fast. Sentiment has finally turned berish in the options market.

RealInvestmentAdvice observes, ““Bullish measures are getting really bullish.”

This is an interesting statement, given how “bearish” sentiment was in 2022. As I noted then:

“Investor sentiment has become so bearish that it’s bullish.

One of the hardest things to do is go “against” the prevailing bias regarding investing. Such is known as contrarian investing. One of the most famous contrarian investors is Howard Marks, who once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while.”

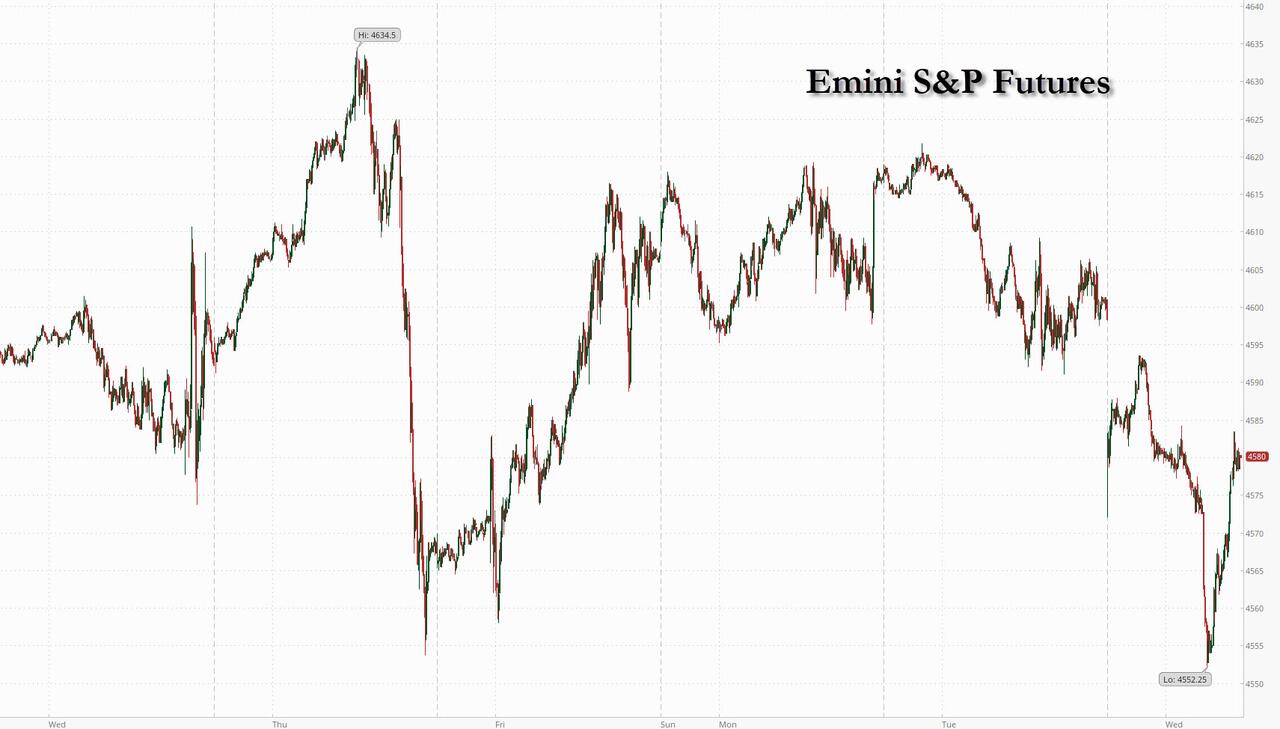

SPX futures dov to a morning low of 4529.20, beneath the 2-month trendline, but still above the Cycle Top support at 4519.96. Declining through the trendline puts SPX on an aggressive sell signal with further signal confidence beneath the Cycle Top. A confirmed sell signal lies beneath Intermediate support at 4462.67. The final Master Cycle high was on July 27 and day 266.

Today’s op-ex shows Max Pain at 4580.00 with long gamma beginning at 4600.00. Short gamma may start at 4575.00 while shorts are well populated beneath that level. Short gamma dominates beneath 4530.00.

ZeroHedge reports, “US futures slumped as part of a global risk-off tone (but were well off their lows, which were down as much as 1%), after the US was stripped of its AAA top-tier credit rating by Fitch (which joined S&P in doing so back in 2011), due to growing fiscal deficits and an “erosion of governance” even as Treasuries yields and the Dollar were steady. And in a complete coincidence, at the exact same time, Donald Trump was indicted for a record third time on federal charges over his efforts to overturn the 2020 presidential election, and has a court date set for Thursday.

As of 7:45am, emini S&P futures were down 0.5%, while Nasdaq 100 futures slid 0.8%, signaling a pullback later Wednesday for a market that has surged 44% in 2023. Broad losses in Europe dragged all industry groups in the benchmark regional index into the red. Asian and European stocks slumped, while the Treasury curve steepened with two-year TSY yields falling 4bps to 4.86%; the Bloomberg Dollar Spot Index was barely changed, up 0.1%.”

VIX futures vaulted to a morning high of 16.23 as it confirms its buy signal. The next resistance is the long-term trendline where it will celebrate its 5-year anniversary this weekend. Trendlines are ubiquitous. Their presence often defines upper and lower boundaries for market movement. A broken trendline may imply a change of trend or the presence of unusual activity, such as the recent liquidity injections by the Fed and the Bank of Japan.

TNX is challenging its Cycle Top resistance at 40.76 this morning. That gives the 10-year yield a better-than-even chance of going higher, potentially breaking out above the July 3 high at 40.94. Today is day 259 of the Master Cycle. However, it is also a day of trending strength. The outcry about the Fitch rating downgrade being “unfair” is growing, but may be silenced as the 10-year yield may exceed 5% in the next 2-3 months.

ZeroHedge remarks, “Treasury Secretary Yellen is pissed, calling the downgrade “arbitrary” and “outdated.”!

“I strongly disagree with Fitch Ratings’ decision. The change by Fitch Ratings announced today is arbitrary and based on outdated data. Fitch’s quantitative ratings model declined markedly between 2018 and 2020 – and yet Fitch is announcing its change now, despite the progress that we see in many of the indicators that Fitch relies on for its decision. Many of these measures, including those related to governance, have shown improvement over the course of this Administration, with the passage of bipartisan legislation to address the debt limit, invest in infrastructure, and make other investments in America’s competitiveness.

Fitch’s decision does not change what Americans, investors, and people all around the world already know: that Treasury securities remain the world’s preeminent safe and liquid asset, and that the American economy is fundamentally strong.”

USD futures are up to 102.30, challenging the 50-day Moving Average at 102.29. This suggests that USD may go higher, but today is day 260 in the Master Cycle, so we must assume the breakout may be on borrowed time. Should the Master Cycle end today, USD may fall back to its trendline at 100.00 before advancing higher. The alternate view is that the Master Cycle may have made its low on July 18.

Crude Oil futures are pulling away from their Master Cycle high on day 266 as it begins the last decline of its correction from its low over 3 years ago. There are two possible targets given in the weekly chart. The first is the Cycle Bottom at 56.48, while the second is the 61.8% Fibonacci retracement at 53.82. Take your pick. The final decline may last until mid-October. Oil investors may not be happy campers during the coming liquidity crisis. And to think that hedge funds have liquidated their short holdings in July…

ZeroHedge remarks, “Benchmark crude oil prices have risen to the highest level for three months after the extension of production cuts by Saudi Arabia and its allies in OPEC+ sparked a rush to cover bearish short positions by investors.

Hedge funds and other money managers purchased the equivalent of 52 million barrels in the six most important petroleum futures and options contracts over the seven days ending on July 25.”

ZeroHedge updates, “Oil prices jumped overnight (near YTD highs) after API reported a massive (record) crude inventory drawdown, but have tumbled this morning as the dollar rallies and bonds & stocks are dumped.

“The OPEC+ Joint Ministerial Monitoring Committee will meet online on Friday, providing Saudi Arabia an excellent opportunity to roll its voluntary 1 million bpd production cut announced on June 3 for July production for another month to September. It would be the second time the Saudis have extended the voluntary 1 million bpd production cut. There is speculation that another 1 million roll forward could slow the global war on inflation, and kill the “golden goose,” especially heading into the end of summer driving season, and the beginning of shoulder season,” Robert Yawger, executive director of energy futures at Mizuho Securities USA, wrote in a Monday note.”