10:05 am

BKX, our liquidity proxy, may be attempting a correction. A likely target may be near the Intermediate-term resistance at 79.91. I am dubious that it will make it, but the Cycles Model suggests the uptick may last through Friday. Hmmm.

ZeroHedge comments, “Despite today’s modest pullback in rates which took place after the 30Y briefly rose above 5% for the first time since 2007, and was catalyzed by the worst (and most realistic) ADP report since 2021, the reality is that rates have seen unprecedented moves in recent months, including a +73.5bps rise in 10yr US yields during Q3, while 30yr yields soared +83.9bps, the largest move since Q1 2009.

It is therefore not a surprise that there has been a frenzy of inquiries into whether the spike in yields will lead to another round of “accidents” something which both Goldman and JPMorgan warned is increasingly likely… and in the case of the latter even welcome, since any regional bank failure would mean that JPM would just become even bigger as it assumes (and with some luck, is paid by the FDIC to do so) the deposits of yet another failed bank(s) – just see what happened in March when every regional bank failure meant JPM would just soak up its good assets while leaving the toxic stuff to US taxpayers.”

8:10 am

Good Morning!

NDX futures made a new high during the overnight session to 14810.80, then pulled back to Max Pain. The correction is underway to a possible high near the Intermediate-term resistance at 15044.56. You may hear sighs of relief that the decline may be over, but don’t believe it. The worst part of the decline is yet to come.

In today’s op-ex Maximum Investor Pain is at 14770.00. Long gamma starts at 14800.00, while short gamma may begin at 14750.00.

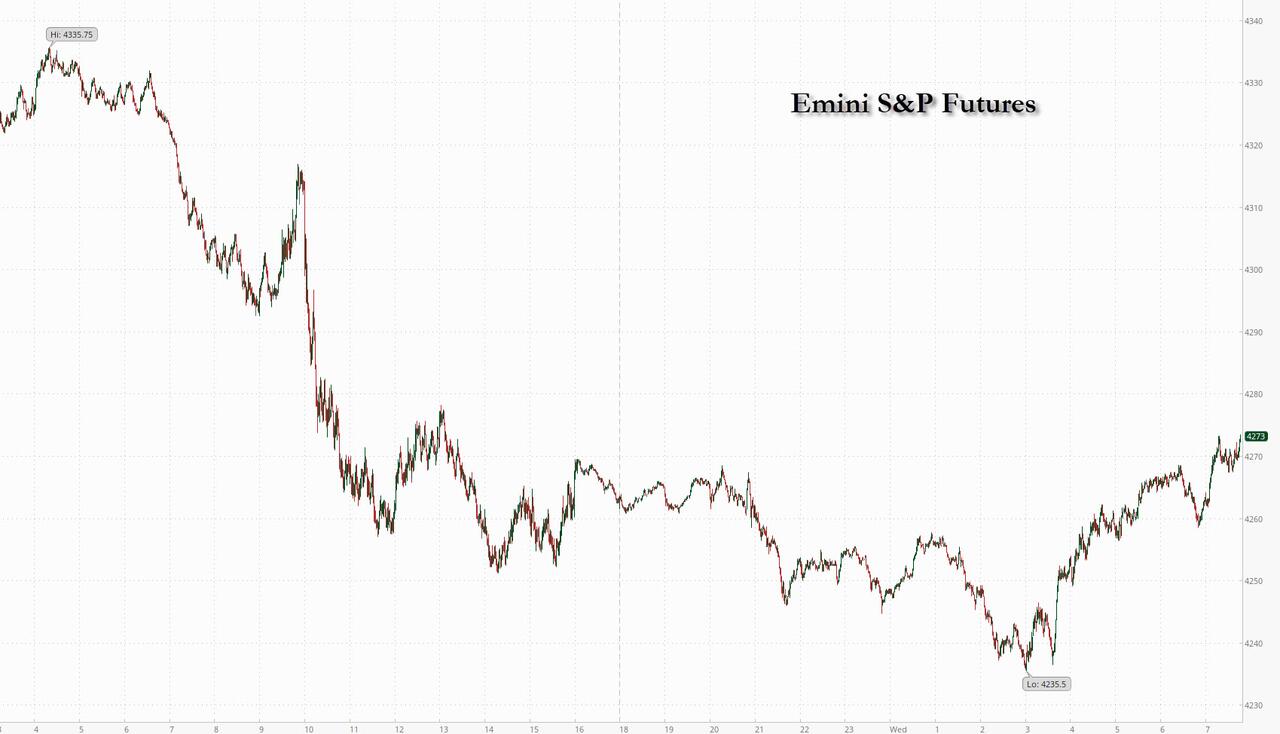

SPX futures tested yesterday’s high in the overnight market, then eased back down to a low at 4242.60. Today is resumes its zigzag journey to resistance at 4335.00. That journey may take another day to complete.

Today’s op-ex shows Maximum Investor Pain at 4255.00. Long gamma may begin at 4260.00 and extends to 4350.00. Short gamma starts at 4235.00 and has support to 4150.00.

ZeroHedge reports, “US equity futures were flat on Thursday, reversing earlier modest losses, with Asia and Europe both solidly in the green after days of losses as global markets steadied thanks to bonds halting their rout as investors looked ahead to more weak labor market data tomorrow. As of 7:45am, S&P 500 futures were unchanged at 4,298 and the yield on 10-year Treasuries was flat 4.71%. The dollar was steady while commodities extended their losses dragged by Energy. WTI has lost ~$10 in six trading sessions, -10.8%, and is virtually unchanged on the year after breaching $95 late last week. Today’s macro data focus includes Jobless Claims and Job Cuts; there are two Fed speakers and announcements on the next wave of bond auctions. Tomorrow we get the Sept NFP which according to JPM “may mean more than next week’s CPI.””

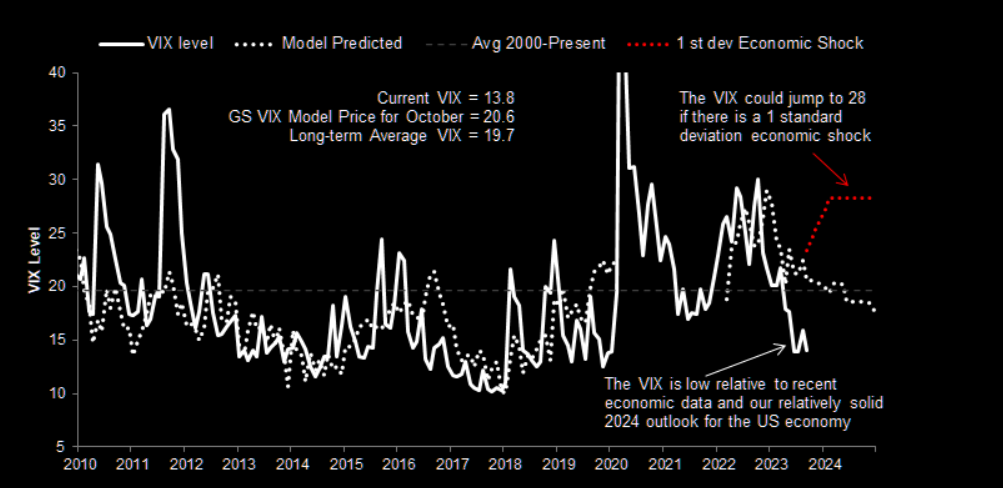

VIX futures traded inside yesterday’s range above the trendline at 18.50. The Cycles Model offers no indication whether the correction may continue lower in the next couple of days, but that is the base case.

Next Wednesday’s op-ex shows Max Pain at 18.00. Short gamma extends from there down to 15.00, while long gamma begins at 19.00 and extends to 42.50.

The October 18 (monthly) op-ex shows Max Pain moving up to 18.00. Short gamma starts at 17.00 and extends to 12.00. Meanwhile, long gamma begins at 20 and extends to 70 with 70,000 contracts at that strike.

TNX has eased back from yesterday’s high, but not for long. While the next couple of days may be quiet, trending strength comes roaring back over the weekend. In July the Cycles Model predicted that TNX would exceed 50.00 by the end of October and it appears that it may come to pass.

ZeroHedge remarks, “Today’s modest normalization notwithstanding, the recent move in rates has been historic: as noted earlier, we have seen a massive +73.5bps rise in 10yr US yields during Q3, while 30yr yields soared +83.9bps, the largest move since Q1 2009. This staggering parallel shift has resulted in huge unrealized losses on bank’s fixed income portfolios (which amount to $5.4 trillion in debt securities), and which according to DB calculations will reveal another $140 billion in unrealized losses, pushing the cumulative total to a new record at or above $700 billion.

USD futures sank to 106.25 in a brief correction, possibly to test the Cycle Top at 105.95. The correction may last to the weekend, but trending strength may resume by mid-week.

ZeroHedge observes, “wo weeks ago, we laid out the various reasons why – according to JPMorgan and Goldman – sentiment on US consumer stocks had cratered, and would continue to worsen.

After a brief short squeeze at the end of September, the XRT retail ETF is at the lowest level since June after peaking on the “last Fed hike” in late July, and as we enter into 4Q, there is a lot on the line in the consumer space, something that has not been lost on the market. Indeed, as Goldman’s Prime Brokerage recently noted, shorting in the consumer discretionary space is at YTD highs as a result of a growing multitude of macro issues.”

Gold futures made a new low at 1826.25 this morning as the decline continues. Gold may consolidate near the Cycle Bottom at 1836.25, but may resume its decline over the weekend. The next threat to investors is breaking the March low at 1810.80. The outcome of that action may cause a “limit down” day to follow.

ZeroHedge observes, “Central bank gold buying continues to sizzle.

Central banks globally added a net 77 tons to their reserves in August, according to the latest data compiled by the World Gold Council.

It was the third straight month of net purchases. Over the last three months, net gold buying by central banks totaled 219 tons.”

Crude Oil futures tumbled to a deeper low at 82.36 this morning as the decline extends beneath critical supports. The next support may be the mid-Cycle line at 77.51. Panic is about to set in as the decline becomes unrelenting.

ZeroHedge observes, “Oil “well” below the 50 day

Despite all the explosion narratives, oil is actually trading at the same levels we traded at in mid November. Oil continues puking below the 50 day, while the 200 day remains way lower. Mean reversion minds remain winners in oil…

Source: Refinitiv

Oil – long and wrong

CTAs were massively long oil into this latest sell-off. We do not have any recent updated data on how much they have sold as price is collapsing, but GS says that it is safe to blame the CTA crowd for the move lower in oil yesterday.”