2:55 pm

It appears that the Ag Index is finally making its Master Cycle bottom. on day 262. I noticed that stores are having sales on canned foods as they move out last year’s crop and make way for this years canned goods. Prices will go up due to developing shortages of food. I was just touring the prairie in western Minnesota and the fields appear to be dried up unless they were irrigated. Rivers and lakebeds are also dry, evidence of lowered water tables. We may be in for a multi-year rally in food prices.

ZeroHedge remarks, “Our standard of living is being systematically destroyed, but for a lot of years many Americans didn’t fully understand what was taking place because it was happening so slowly. But now we have reached a stage where the purchasing power of our money is collapsing and the cost of living has become exceedingly painful. Thanks to our rapidly rising cost of living, the middle class is becoming “the impoverished class”, and the poor are increasingly being pushed out into the streets. If we do not find a way to turn these trends around, it won’t be too long before we have tremendous societal turmoil on our hands.”

10:35 am

The bounce in the Banking Index continues on thinner ice as liquidity is drained from the markets. Once the supports give way, the ensuing plunge may exceed that of the March decline. The Head Shoulders formation i s still active and awaits completion.

ZeroHedge observes, “After an unusual outflow last week, US money market funds saw a $6.3BN inflow this week, back up close to record highs…

Source: Bloomberg

Once again, retail funds saw inflows (no outflows since April) of $7.8BN while institutional funds declined $1.5BN…

Source: Bloomberg

That is the second week of institutional outflows as retail inflows send total retail funds to a new record high…”

9:30 am

Good Morning!

SPX futures reached a morning high at 4333.15 as it may have completed its retracement back to the Head & Shoulders neckline at 4335.00.

In today’s op-ex, Max Pain is at 4325.00. Gamma turns positive at 4340.00, while short gamma begins at 4315 with a massive put wall at 4300.00 with 19047 put contracts.

ZeroHedge reports, “US equity futures and global stocks rose on the last trading day of the week, month and quarter and global bonds rebounded after dovish comments from Fed officials and signs that European inflation is finally slowing when EU consumer prices rose just 4.3%, down from 5.2% in August, and the lowest since Oct 2021. Ahead of today’s closely watched “Fed’s favorite inflation gauge”, the core PCE due out at 8:30am ET, S&P and Nasdaq 100 futures were up 0.4% as longer-dated bond yields were 2-3bps lower while supportive inflation data in Europe drove European bond yields lower this morning. 30-year TSY yields are down 3bps at 4.68% but still on course for their largest quarterly gain since 2009. The US Dollar dropped and crude oil rebounded. Commodities are mostly higher led by base metals (Aluminum +1.8%; Copper +1.3%), with Brent back over $96 and approaching the 2023 high of $97. Today’s macro focus is on PCE, Personal Income/Spending, Chicago PMI, and U of Mich. survey data. For PCE, consensus sees the PCE deflator printing at 0.5% vs. 0.2% prior and Core PCE deflator rising 0.2%, unchanged from 0.2% prior.”

VIX futures opened at 16.87 and remained soft wile SPX lingered near its target. The Cycles Model shows trending strength beginning today, so the correction may not last.

Next Wednesday’s op-ex shows some short gamma between 14.00-16.00. Gamma turns long at 17.00 and remains strong to 40.00.

TNX pulled back this morning after a stellar rise over the last week. The correction may decline to the Cycle Top support at 44.29. However, trending strength may come back over the weekend as the final Wave completes the Master Cycle in the next three weeks.

ZeroHedge reports, “The last coupon auction of the week is now in the history books, and for long-suffering bond traders it couldn’t come a minute sooner.

After two solid bond sales earlier this week, moments ago the Treasury offloaded another $37BN in 7Y paper, in what was at best a mediocre affair.

Pricing at a high yield of 4.673%, this was the highest stop on record…

… up a whopping 46bps from the 4.212 in August, and also tailed the When Issued 4.670% by 0.3bps.”

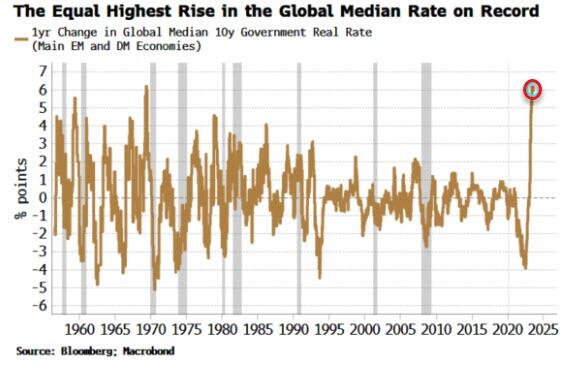

ZeroHedge further observes, “Bonds continue to look oversold after the equally-sharpest rise in the global median real yield seen in at least 60 years. More consolidation in the shorter term is anticipated as bonds continue to work off their oversold condition.

Yields across DM have hit cycle highs in recent days. They started to swing lower Thursday afternoon and are following through in the European morning.

Term premium has been rising as bonds’ efficacy as a portfolio and a recession hedge is impaired when the stock-bond correlation is positive. After most of the last two decades being negative, the correlation is positive again as inflation and inflation expectations have a greater influence on markets.

The global real yield of the largest EM and DM countries has increased by the most over one year since 1969, rising by over six percentage points.”

USD futures challenged their Cycle Top support at 105.69, declining to 105.34 prior to a bounce. The rally may soon resume as the Master Cycle has three weeks remaining to go higher.

ZeroHedge observes, “Last week we laid out what the economic consequences of a lengthy government shutdown would likely be, among them a drop in GDP and a spike in the unemployment rate perhaps sufficient to push the US economy into recession, not to mention a halt in most economic data reporting..

… but ahead of the Sept 30 midnight drop dead date, there is still some confusion so let’s recap the main points, the first of which is that a government shutdown should not be confused with the debt ceiling and its potential for a sovereign default.

As JPM writes in its latest shutdown note, if no deal is reached by Oct 1 – which is now certainly the default case – then a continuing resolution is one of the more likely paths, but should a CR remain in place by Jan 1, 2024, then there will be an automatic cut to military/defense spending.”