Please note: This may be may last newsletter for the month of September.

12:23 pm

BKX may be completing a small retracement (short squeeze). Overhead resistance is at 83.9, if needed. The Cycles Model suggests a decline may resume to mid-October. Be aware of the Head & Shoulders formation and its minimum target.

ZeroHedge notes, “The panic that gripped financial markets in March over the regional bank bailout, which was in large part due to exposure to the foundering commercial real estate space in general and the office sector in particular, is all but forgotten even though in the six months since underlying fundamentals have only gotten worse, underlying cash flows in the CRE space have slowed further, and . In fact, the only thing that has changed is the record amount of “papering over” the Fed has enabled with the central bank’s BTFP facility hitting an all time high every week. Meanwhile, if one eliminates the impact of the BTFP program, which is scheduled to sunset in around 6 months, regional banks are effectively insolvent as the following chart showing large and small banks’ cash/assets with and without BTFP makes clear.

But not everyone has decided to just ignore the elephant in the room, which represents a staggering $2.5 trillion in debt maturities and rollovers at much higher rates, over the next five years:”

8:10 am

Good Morning!

NDX futures have fallen to 15404.00 thus far. A sell signal is generated beneath the 50-day Moving Average at 15282.50. The September 1 high remains the top of the last Master Cycle, leaving the decline in place through mid-October.Warning: Bear markets are where the strongest up-days are. However, they are book-ended by even stronger down days. It is often best for the average investor to remain at the sidelines until the Cycle plays itself out.

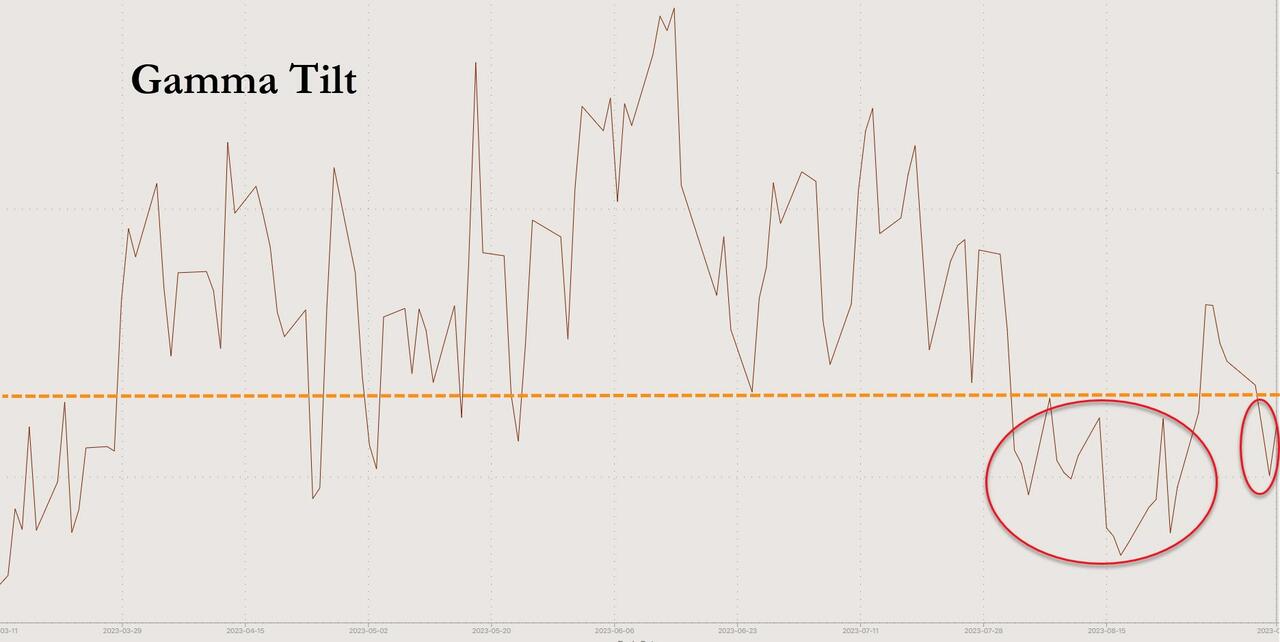

Today’s op-ex shows Maximum investor Pain at 15430.00. Long gamma begins at 15450.00 while short gamma starts at 15425.00. Sentiment has levelled out, making it difficult who has the upper hand.

ZeroHedge remarks, “Heading into Triple Witching week (which only happens four times a year), the market has been struggling in a neutral position as it dipped into negative gamma territory for the second time this year. What we learned from the recent stretch of negative gamma in August is that context of structure and flow have become proportionately more important. This is partially because 0DTE flows have been supplementing the diminished liquidity from net negative market gamma.

When we exited the first round of negative gamma that we were in for the majority of August, we saw 0DTE flows tip the scales here by moving with the trend rather than against it (as it usually does).

If 0DTE flows begins to do this when in negative gamma, and chases a downtrend, then this could become quite dangerous for the market.”

ZeroHedge observes,”The risk premium investors demand from technology stocks is now the lowest since the dotcom bubble, underscoring the extent to which valuations have run up this year — and sending a warning.

The prospective earnings yield on the Nasdaq 100 adjusted for the Federal Reserve’s benchmark rate turned negative late last year, with this year’s stunning rally taking it further south:

The magnitude of inversion was on a similar scale but less pronounced in the run-up to the financial crisis, and clearly both prior episodes didn’t end well for investors.”

SPX futures have declined to test the 50-day Moving Average at 4476.51 thus far. Should it open beneath it, a sell signal may be generated. We may see an effort to keep the SPX above its Head & Shoulders neckline at 4335.00 prior to options expiration. 0DTE traders may quickly jump on any trend, including short, so the market is at a delicate juncture.

Today’s op-ex shows Max Pain at 4475.00. Long gamma starts at 4500.00 while dhor gamma begins at 4450.00.

ZeroHedge reports, “US futures are slightly lower, but holding on to much of yesterday’s tech-driven gains, with European bourses and Asian markets mixed ahead of tomorrow’s CPI print. At 7:30am ET, both emini S&P500 and Nasdaq 100 futures slipped 0.3%, reversing yesterday’s rally. Tech stocks retreated as Oracle dropped 10% after posting slowing cloud sales, while the euro and pound weakened on concern the Europe faces a growing threat of stagflation. Tech will also be the center of attention on Tuesday, with Apple set to unveil a new product lineup including the new iPhone 15, and SoftBank-owned chip designer Arm gearing is set to price the biggest IPO of the year. US Treasuries edged lower, commodities are higher led by base metals with oil trading near its highest level this year before the OPEC monthly report. Gold fell while bitcoin redovered much of yesterday’s losses.”

VIX futures are consolidating inside yesterday’s trading range. The Cycles Model suggests (up)trending strength may build into the end of the week. A breakout may be imminent. The Cycles Model suggests the new trend may last to mid-October.

Tomorrow’s op-ex shows Max Pain at 14.50. There is a small contingent of puts at 14.00. Long gamma begins at 17.00 and currently runs to 29.00. Not much conviction here.

The September 20 op-ex shows Max Pain at 18.00. Short gamma reigns between 14.00 and 17.00. Long gamma begins at 20.00 and runs to 60.00.

ZeroHedge observes, “Never forget VIX seasonality

Will it strike again?

Source: Equity Clock

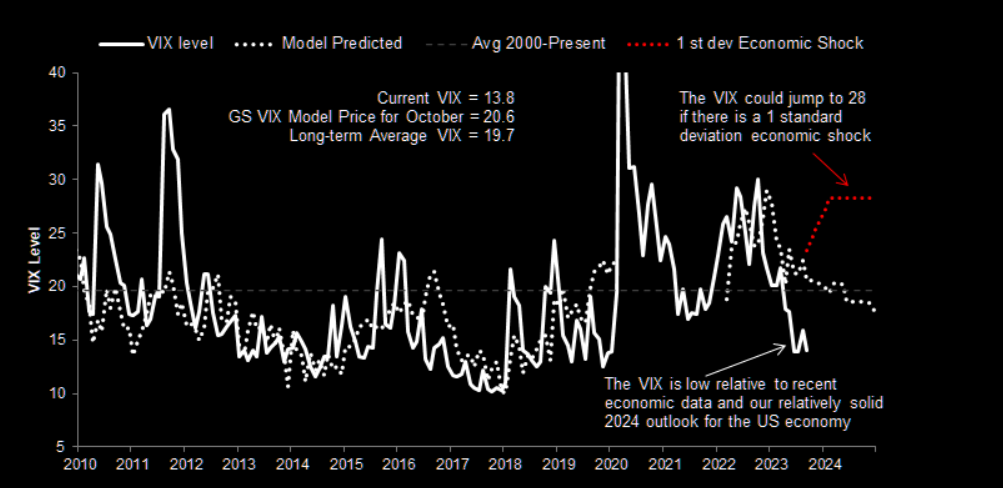

GS: VIX upside

GS: “We see upside to the VIX based on our Economists’ forecasts”. Chart shows actual vs predicted VIX levels based on the GS economic model of volatility.”

TNX may be consolidating above the Cycle Top support at 42.75. The Cycles Model calls for a rally with strength into the end of the week. Then we may see a retracement, just as traders switch to longs. Ms market can be fickle at times.

ZeroHedge reports, “The Treasury’s first coupon auction came a day earlier, and instead of the usual Tuesday offering, moments ago Janet Yellen’s department sold $44BN in 3 Year paper at a yield of 4.660%, higher than last month’s 4.398%, and the highest since Feb 2007. The auction also tailed the 4.650% When Issued by 1 basis point, the first tail since June.

The Bid to Cover of 2.751 was below last month’s 2.901 – in fact, it was the lowest since June – and just below the six-auction average of 2.788.”

USD futures are consolidating beneath the Cycle Top resistance at 105.30. The Cycles Model suggests rising strength this week, possibly extending the Master Cycle. However, that may be followed by a pullback to the trendline at 103.25. An alternate target may be the mid-Cycle suport at 102.75.

WTIC is running a strong uptrend that may bring in more investors. The unfortunate part of this equation is that The Current Master Cycle is due to end next week. The likely target is the trendline at 90.00. The normal pullback may be to the mid-Cycle support at 76.31, but it may go lower.

ZeroHedge remarks, “Oil prices had been coiling for a few days ahead of this data and are breaking out now after OPEC reports that global oil markets face a supply shortfall of more than 3 million barrels a day next quarter – potentially the biggest deficit in more than a decade.

If realized, it could be the biggest inventory drawdown since at least 2007, according to a Bloomberg analysis of figures published by OPEC’s Vienna-based secretariat.

OPEC’s 13 members have pumped an average of 27.4 million barrels a day so far this quarter, or roughly 1.8 million less than it believes consumers needed, according to the report.”