1:45 pm

SPX has made a partial rally to the neckline at 4335.00. The balance of the rally may be finished by tomorrow morning. Its time to go short again either before the close today or early morning.

ZeroHedge remarks, “Credit spreads are vulnerable to an abrupt repricing wider as trading conditions in equity markets become more volatile from negative gamma.

An old Swedish proverb warns that what is hidden in the snow, is revealed in the thaw. Things are heating up in equity markets, threatening to lay bare the true state of credit. That risks a sharp widening of credit spreads as they rapidly adjust to worsening underlying credit conditions. With bond yields rising too, markets are in a riskier spot than they have been for several months.

The catalyst for more upset might just be negative gamma. When positive, it’s associated with more stable, less volatile equity-market behavior. But according to Goldman Sachs, S&P gamma is now at a series low, opening up a veritable Pandora’s box of risk and the potential for much higher equity volatility and considerably wider credit spreads. The move is perhaps now getting started, with both the VIX and spreads higher in recent days.”

8:00 am

Good Morning!

SPX futures are consolidating above the 200-day Moving Average at 4296.15 and beneath the Head & Shoulders neckline at 4335.00. That will remain the trading range until the bounce is complete. Once accomplished, the decline resumes with more vigor as the most intense part of the Cycle takes its position over the next three weeks.

Today’s op-ex shows Maximum investor pain at 4310.00. Long gamma begins at 4315.00 wile short gamma rules beneath 4250.00.

ZeroHedge reports, “US equity futures reversed initial gains following Wednesday’s surprise reversal that helped US stocks close green, and were trading marginally lower as global bonds resumed their selloff, sending 10Y yields to a new 16-year peak as soaring Brent oil prices hit $97 overnight before reversing as the US Dollar dipped. At 7:45am ET, S&P futures traded down 0.1% and Nasdaq 100 futures were down -0.3%. As 10-year yields rose 4bps to 4.65% the yield curve flattened and the 2s10s was inverted by less than 50bp for first time since May. 1Y breakeven had its largest move since late July as oil surged on constrained supply. Commodities are mixed with metals and natgas leading with USD lower pre-mkt. Today’s macro focus is on GDP, Consumption, Jobless Claims, Pending Home Sales, Kansas Fed, and updates on economic revisions. We also get four Fed speakers, including Powell at 4pm. Financial conditions have tightened since the Fed meeting and mortgage rates are at multi-decade highs. Keep an eye on the 4200 level as we reach expiration on Friday and the JPM collar is rolled.”

VIX futures made a possible Master Cycle high yesterday, on day 257. Circumstances suggest that the high may extend another day or two while the SPX tests its 200-day Moving Average. Many analysts claim that the VIX may head even lower, as recency bias sets in. Another argument is that seasonality indicates that the decline in stocks may be over, leading one to believe that VIX will suffer for it. A reminder that seasonality (calendar patterns) is not the same as Cycles. The Cycles Model indicated a continued rise in VIX through late November.

Wednesday’s op-ex shows Max Pain at 16.00 in the VIX. There is no short gamma. Long gamma begins at 17.00 and extends to 40.00.

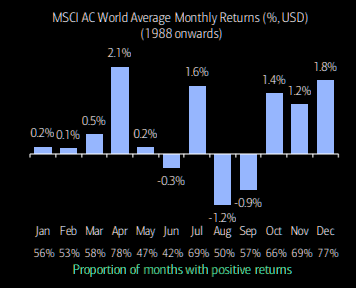

ZeroHedge remarks, “Seasonality – headwinds turning into tailwinds

“…the last 10 days of September being the worst 10-day period of the year. However, the headwinds turn into tailwinds as we step into the final quarter, with an average rise of 4.5% at a hit rate of 80% in the global equities since 1987.” (BofA)

TNX futures hit a new high at 46.90. The Head & Shoulders target appears much more attainable than before, as the current Master Cycle has three more weeks to go.