2:34 pm

VIX appears to be on the rebound after making a new low at 18.68 on its Trading Cycle. This was unexpected and caused me to rethink the Cycles structure. While today’s low may be the basis for a new Master Cycle pattern, the Cycles Model is not so clear. The high on March 4 was on day 262 of the Master Cycle. It appears that I will have to stick with it until further evidence tells me otherwise. In the meantime, the Cycles Model shows strength beginning in early April and continuing through mid-May.

2:18 pm

NDX remains on its sell signal after being repulsed at Short-term resistance at 12866.05. It appears to be read to cross the Lip of its Cup with Handle, setting a course for its long-term trendline just above 7500.00. Should this take place, the rest of the market will follow.

ZeroHedge observes, “Something odd is going on.

During today’s US session we noticed an unusual number of large block trade headlines.

- Shopify – SHOP 762k @ $1,000

- FarFetch – FTCH 26mm @ $45

- Discovery – DISCA 16mm @ $45-50, DISCK 32mm @ $40-44″

8:15 am

Good Morning!

SPX futures were as high as 3921.38 this morning before fading lower. The Elliott Wave Model suggests a brief surge at the open to 3935.00, if it can achieve it. The Cycles Model suggests a breakdown may be in order. The question is how fast the SPX may tumble beneath all the supports that have held it thus far.

ZeroHedge reports, “US equity futures and global markets rose this morning, continuing yesterday’s torrid late day surge, as investors looked past supply chain disruptions and focused on the optimistic targets for vaccinations and economic re-openings, after Joe Biden doubled the goal for his vaccination drive even though Covid-19 cases keep rising, and the Federal Reserve freed banks from pandemic restrictions on dividends. Oil rebounded and pushed Treasury yields higher, prompting investors to buy undervalued energy and bank stocks ahead of what is expected to be the fastest economic growth since 1984. Investors awaited key income, spending and inflation data later in the day.”

NDX futures rose to 12880.00 in the overnight session before plunging into the red as the morning wore on. It is currently challenging the Lip of the Cup with Handle formation at 12700.00.

The following may explain why the stimulus checks may not end up in the market. ZeroHedge reports, “After the extreme surge in income and spending in January (as government handouts gushed across the nation), analysts expected February to see some give back (more on the income side than on the spending side) – they were right.

Americans’ income fell 7.1% MoM in February (-7.2% exp) vs the 10.1% (revised up) rise in January.

Americans’ spending fell 1.2% MoM in February (-1.0% exp) vs the 3.0% (big upward revision) jump in January.

Source: Bloomberg

That is the largest MoM decline in Americans’ income on record.”

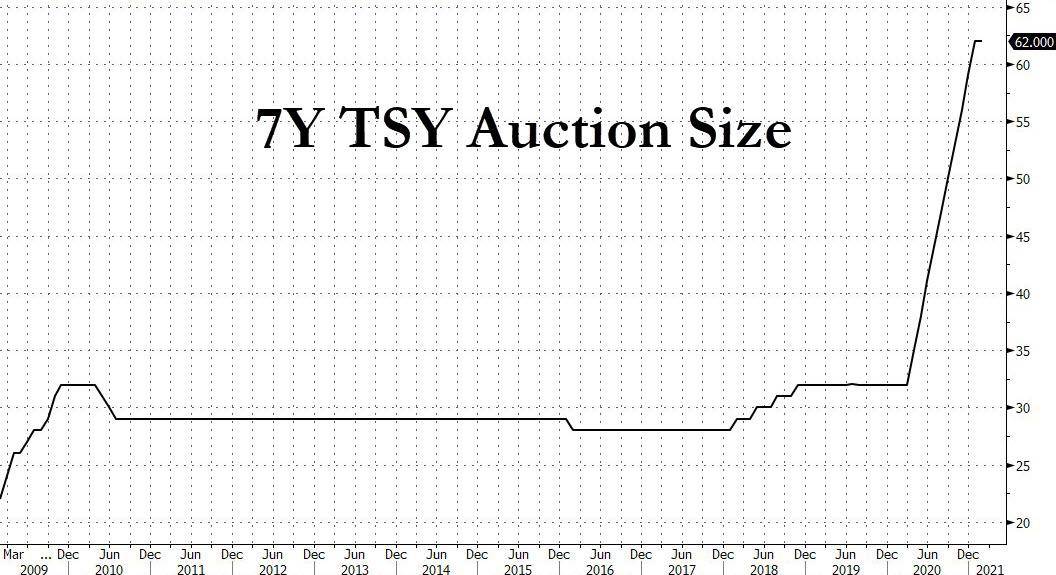

TNX jumped higher this morning, sending yields as high as 16.81 and jitters up the spines of traders. Yesterday’s 7-year Treasury auction was a bust. The next 10-year auction is scheduled for April 8. In the meantime, the Cycles Model suggests a painful month ahead for bond investors.

ZeroHedge reports, “It wasn’t nearly last month’s catastrophic 7Y auction but it wasn’t all that much better either.

Moments ago the Treasury sold $62BN in a closely watched 7Y auction (previewed here), which matched the record size for the tenor.

And while sentiment was far more positive heading into the 1pm deadline, traders were surprised to learn that the high yield on the auction was a rather dismal 1.30%, which tailed the When Issued 1.275% by a sizable 2.5bps and was the highest yield since Jan 2020.”

VIX futures drifted lower in the overnight session, hitting a low of 19.24. Yesterday’s breakout above the 50-day suggests the pullback won’t last. There appears to be an attempt at a Trading Cycle low, which may match, but not trump the Master Cycle low of Tuesday.

The NYSE Hi-Lo Index closed at a deeper low yesterday after venturing to a high of 71.00 intraday. This is an unequivocal sell signal, showing the internal deterioration inside the markets. This is telling us that the decline will not be normal, but an avalanche, taking everything with it.

USD futures appear to be consolidating after rising above the 200-day Moving Average at 92.76. The Cycles Model calls for another three weeks of rally which appear to be targeting the Cycle Top and Broadening wedge trendline at 95.94. A USD short squeeze may have begun.

Investing observes, “Investors have a voracious appetite for U.S. dollars this month as the Dollar Index climbed to its strongest level in four months. Over the weekend, the Senate passed a $1.9-trillion stimulus bill that is expected to pass the House tomorrow and signed by President Joe Biden before the end of the week. The passage of this bill has been eagerly awaited and now that it is pretty much a done deal, investors are starting to think about how stimulus cheques will be spent. “