10:40 am

TNX has made a new high at 10.39 this morning, increasing the jitters in equities. There are two possible patterns hare, both ultimately leading to higher yields. The first is that the Master Cycle, which corresponds with Primary Wave [3], ended on February 28 at the 16.14 high. The subsequent rally may be a Wave (B) in the correction, leading to an immediate decline back to one of the underlying supports. The second (less favored) view is that Intermediate Wave (5) of Primary Wave [3] still has room to run and may hit 17.00 before it is over. I view this as less favored due to the lack of strength being exhibited in next week’s Cycles Model.

ZeroHedge observes, “Treasuries are under meaningful pressure as the 1.624% yield peak in 10s comes into range. There was no definitive trigger other than the usual suspects of reopening optimism, supply indigestion, and SLR expiration jitters. To this latter concern, the most recent primary dealer holdings data as of March 3rd revealed a record $64.7Bn decline in Treasury holdings to $185.8 bn. It’s worth noting that -$23.5 bn of this was in the bill sector and -$3.7 bn in floating rate notes; that said, notes and bonds were also reduced. However, given the preceding spike in yields and the fact these figures are reported in market value rather than par terms, the drop reflects more than simply dealers aggressively shedding Treasuries as the extension of SLR became less certain. Nonetheless, dealers selling into the downtrade is consistent with the choppy price action seen during the last several weeks and concerns that ballooning net issuance could be problematic for liquidity conditions; particularly in the event the preferential treatment for Treasuries is lost.

It’s with this backdrop that today’s trading session takes on particular relevance in gauging investor sentiment as the weekend approaches. While last week saw a meaningful challenge to the ‘Friday afternoon bears’ pattern which has been evident throughout much of this year, as we ponder the information on offer, there is little to dissuade the drift higher in yields aside from residual price action in other markets. PPI and the University of Michigan’s confidence figures won’t meaningfully influence the outlook for the recovery and as such we anticipate the reports will be largely ignored in favor of anxiously watching the response in risk assets as the path of least resistance appears toward higher yields as the US comes online.”

ZeroHedge advises, “The 10Y just tagged the March 5 high yield of 1.625% – a key stop loss level – and steamrolled higher amid a cascade of short covering, because as noted earlier, once the momentum kicks in nobody knows where and how it stops.

And unfortunately for TSY bulls, the pain could be just starting because as BMO’s Ian Lyngen noted, those hoping for a contrarian buying signal from the banks/dealers will have to wait a long, long time. That’s because the latest weekly data (ending March 3), showed that the primary dealer holdings data revealed a record $64.7Bn decline in Treasury holdings to $185.8 bn!”

7:30 am

Good Morning!

SPX futures declined to a low of 3910.12 this morning. Whether bullish or bearish, there is likely to be a bounce off 3900.00 going into the weekend. Today is day 259 of the Master Cycle for the DJIA and 256 for the SPX. While the high may have been made yesterday in the DJIA and the SPX, more work needs to be done to done to confirm the turn. It may seem that I am skittish after having had a perfectly bearish pattern blow up with an extension. True. But I will point out that the new Master Cycle will not end until options expiration week in MAY. So there may be plenty of time to position for a bearish outcome.

NDX futures are bearish after being repelled at the 50-day Moving Average at 13128.54. The low was 12786.38 before a bounce, but the NDX needs yet another probe lower to confirm the possible change in the Elliot Wave structure of the Cycle. I will point out, however, that this is a very bearish structure. The Cup with Handle gives the potential target for Primary Wave [3]. The average target for Cycle Wave I is 6500.00.

I recall discussing a very similar situation in March 2000 with Sir John Templeton, who was down $600,000.00 when the NDX bounced against his bearish speculation. I asked him if he was taking the loss. He said, “No. I am adding another $600.000.00 to my short position.” The NDX then proceeded to decline 65%. One of his oft-quoted sayings is, “The best time to invest is when there is blood on the streets, especially when it’s your own.” The shorts have been bloodied in this week’s move. The lack of shorts at the top of this Cycle practically guarantees a massive decline, since there will be no buyers for a long way down.

ZeroHedge reports, “Nasdaq futures fell as much as 2% on Friday after rebounding more than 6% in the past three sessions, after a new spike in U.S. bond yields restarted inflation fears and sent investors scurrying to the perceived safety of the dollar, while hammering global stocks. A Bloomberg report that Beijing is expanding a crackdown on Tencent Holdings also weighed on the technology sector. S&P 500 futures were also dragged down after ending at record closing highs, and we last trading just above 3,910, down 16 points, or 0.4%, while Dow E-minis were up 12 points.

Friday’s selloff was sparked after the yield on the benchmark 10-year notes rose back above 1.60% on Friday to approach the one-year highs touched last week (more below).”

VIX futures challenged the 50-day Moving Average at 22.98 in the overnight session. Should equities venture lower, the VIX may respond by going higher. However, the setup near the close of the day may be most telling.

TNX surged above 16.00 in the futures while making a cash market high of 15.93. This is raising anxiety about the resurgence of inflation and the concern for the expenditures in the stimulus, which are being fueled by more debt. However, today is the last day of trending strength.

However, it appears that the 10-year Treasury Note may be bought, at least through March options expiration, causing a test of the supports below.

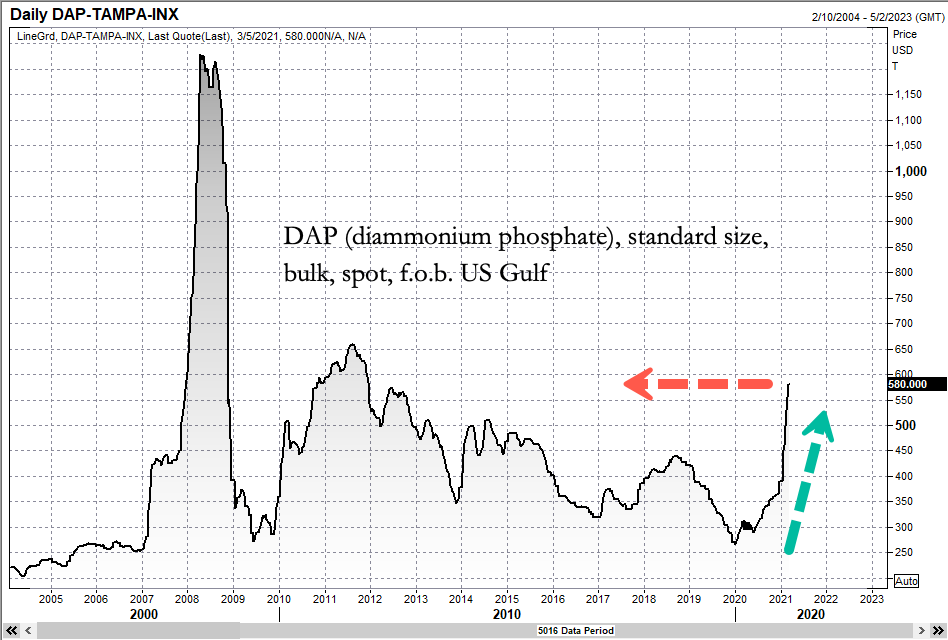

The Ag Index may be taking a breather, as prices decline into the next trading Cycle low later this month. The Elliott Wave structure points out a probable Expanded Flat formation, where Intermediate Wave (C) declines to the low of Intermediate Wave (A). Once accomplished, Primary Wave [3] may get underway with a probable target near 1000.00.

ZeroHedge reports, “US wholesale fertilizer prices have been on a tear since December 2020 due to rising commodity prices, tight supplies, and strong demand.

Last fall, Rabobank forecasted that phosphate and other fertilizer prices would remain elevated in the first half of 2021 because commodity prices were accelerating. Now Rabobank reports phosphate prices have nearly doubled.

“With the increase in commodity prices, there has been an increased demand for fertilizers since last fall. This increased demand, coupled with reduced fertilizer imports is – according to forecasters – predicted to keep fertilizer prices elevated through fall and potentially into next year,” Jamie Patton, senior Outreach Specialist for the UW-Nutrient and Pest Management Program, told Wisconsin State Farmer.

DAP Tampa Fertilizer Index has nearly doubled since the start of the year. ”

USD futures bounced to a high of 91.95 in the overnight session. There is a distinct possibility of a retest of over head resistance at 92.59 to 93.03 in the next few days. A breakthrough may power the USD toward the Broadening Wedge trendline at 96.00 by mid-April. This may be a pain trade, as there is still an overwhelming short USD position.