8:45 am

I will be away for the next 5 days to visit my eldest son and his family. I’ll be back for commentary on March 24.

NDX futures declined to a low of 12951.50, on a sell signal beneath the 50-day Moving Average.

ZeroHedge reports, “It started off well enough, with futures initially continuing their post-FOMC ascent and lifting global markets.

However, It all reversed sharply during the Asian session driven by a sharp spike in the 10Y TSY, which initially jumped following a Nikkei report that the BOJ readied to adjust monetary policy and will look at measures that will allow long-term interest rates to move in “a slightly larger range of about 0.25%, versus 0.2% now” in order to make life easier for financial institutions. The news, which came during the Japanese trading break forced local traders to sell US paper instead.

The selloff then accelerated sharply when Europe opened, and pushed the 10Y as high as 1.75%, a level which BofA two weeks ago said was the “tipping point” for bonds…

… the highest level since Jan 2020, while the 30-year topped 2.5% a level that hasn’t been seen since August 2019

The algos took one look at the fresh surge in yields and dumped risk assets with a focus on high duration “bathwater” tech names, slamming Nasdaq 100 futures 1.7% lower….

… while Emini S&P futs were set to fade the entire post-FOMC move.”

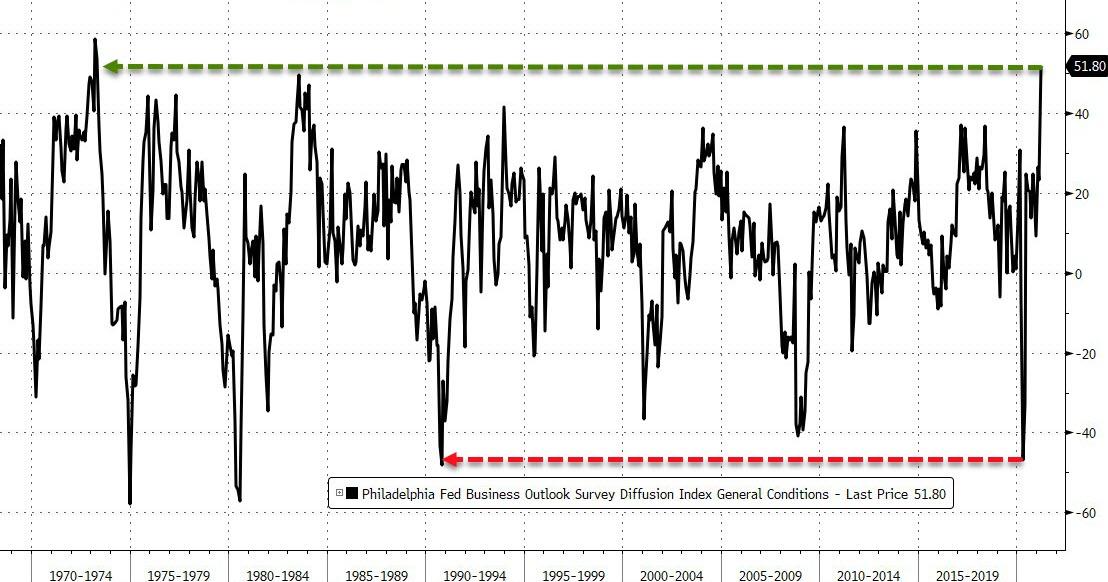

TNX rallied to a high of 17.47 (17.45 in the futures) this morning. The Cycles Model suggest a continuation of this rally with growing strength through the end of the month. A possible trigger for the spike in the 10-year yield may be the Philly Fed Index, which reported a massive increase.

ZeroHedge reports, “The Philly Fed Business Sentiment Indicator exploded higher in March. Against expectations of a rise from 23.1 to 23.3, it jumped by the most ever to 51.8…

Source: Bloomberg

That is the highest level since the Arabian Oil Crisis in 1973.

Under the hood, everything jumped except inventories…

- New orders rose to 50.9 vs 23.4

- Employment rose to 30.1 vs 25.3

- Shipments rose to 30.2 vs 21.5

- Delivery time rose to 29.5 vs 15.1

- Inventories fell to 12.1 vs 20.0

- Prices received rose to 31.8 vs 16.7

- Unfilled orders rose to 21.8 vs 12.6

- Average workweek rose to 39.7 vs 30.6

- Six-month outlook rose to 61.6 vs 39.5

But, the surge is driven by a massive spike in the prices-paid index (which rose to 75.9 vs 54.4).”

Yet another indicator of trouble ahead. ZeroHedge reports, “While much of the financial commentariat spent Wednesday afternoon focusing on the Fed’s useless dot plot (which focuses on a period that takes place about a year after Powell’s tenure at the Fed is over and he will be replaced by uber-dove Brainard), we pointed out a “huge surprise” (as Curvature’s repo expert Scott Skyrm put it) contained deep inside the statement – the Fed’s decision to hike the Reverse Repo counterparty limit from $30 billion to $80 billion.

Why was this significant? Because as Skyrm explained, “if the Fed wanted overnight rates higher, they would have raised the IOER and/or RRP. Instead, they raised the RRP counterparty limit” which also “implies the Fed is very comfortable with zero percent rates and maybe even negative rates.”

In other words, having seen the recent drops of overnight GC repo into the red…

… and 1 month bills trading as low as -0.01% this morning, the Fed decided to do nothing.

However, as that “other” repo guru, Zoltan Pozsar (formerly of the NY Fed and currently at Credit Suisse) pointed out later on Wednesday, there is another possible interpretation, a much more ominous one for those who believe that banks need an SLR exemption now, or else they will be forced to raise capital/delever/dump treasurys – in other words, lead to even more pain for Treasurys.

SPX futures declined to a low of 3932.62, testing its support at yesterday’s low. As mentioned yesterday, the EW structure is complete, and a decline beneath 3935.00 may eliminate the possibility of a new high. A decline beneath 3900.00 may turn options gamma negative, as well. The fly in the ointment is that the DJIA may have made a new (all-time) overnight high. However the DJ30 futures turned red this morning.

The social mood is shifting. People have quit wearing masks in droves. Anthony Fauci is ignored or, even worse, mocked. We are already tiring of Biden’s ineptitude. This may be showing up in the markets. Be prepared for a sudden shift in sentiment that will take many by surprise. The stimulus checks are coming, but will they be enough?

ZeroHedge observes, “The highly anticipated Fed meeting is now in the rearview mirror, but for weary traders sitting at a fresh all time high in the S&P, the week is not yet over as another major market event is on deck: we are talking about Friday’s quad-witch (quadruple expiration) when once a quarter on the third Friday, we get the simultaneous expiration of stock index options, market index options, individual stock company options and and single-stock futures.

At the 30,000 foot level, two things make Friday’s quad-witch especially notable: the relatively small size of Friday’s event, and the dismal liquidity going into it.

As Goldman writes in its latest Vol Vitals report, when measured in contracts (or percent of SPX market cap), the SPX open interest expiring this Friday is the smallest for at least a decade. The 4.0 million March contracts outstanding are just 60% of the open interest at this point in the volatile week approaching March-2020 expiration. According to Goldman, the reduced SPX open interest reflects volume continuing to spread around the calendar instead of being concentrated in just the quarterly expirations. Meanwhile, the rising SPX index level has left the bulk of March open interest (87% has strikes of 3900 or lower) below the current index level, so expect marketwide gamma to have limited impact on trading dynamics this week.

VIX futures rose to an overnight high of 20.43. While nowhere near the 50-day, VIX may have become unshackled from the short-vol trade, since futures and options expired yesterday. The rest of the market is in a fragile state, with liquidity extremely low. Quad witching may light a spark under the VIX that sends it rocketing higher.

USD futures are moving higher. Both the Cycles and Elliott Wave structure imply that USD may rally back to the Broadening Wedge trendline at 96.00. That is entirely possible due to a potential sell-off in stocks, raising the demand for USD and the massive short USD trade that may be forced to cover. The current Master Cycle ends on options expiation day in April.

Gold futures are sliding again. Despite all of the calls to buy gold, it appears that it may descend to the bottom trendline at 1500.00 before too long. The next Master Cycle is due at the end of the month. Should liquidity remain thin and the USD rally to 96.00, gold may have no other choice than to plummet.

ZeroHedge comments, “Worried about gold sentiment? Don’t be.

The mainstream view of gold right now is an open yawn, and sentiment indicators for this precious metal are now at 3-year lows despite the gold highs of last August.

Is this cause for genuine concern?

Not at all.

In fact, quite the opposite.

Most investors are totally wrong about gold, and below we show rather than argue why they are missing the forest for the trees.

Unlike trend chasers, speculating gamblers and gold bears, sophisticated precious metal professionals and historically (as well as mathematically) conscious investors are not only calm right now, they are biding their time for what is about to become gold’s perfect backdrop and, pardon the pun, golden era.”