3:16 pm

NDX continued its decline after an 82% retracement. It has fallen back beneath its Short-term support at 12 891.92, which has made a bearish cross of the mid-Cycle and 50-day lines. If this is a short squeeze, it appears that there are no shorts who covered above the 50-day moving average. In addition, there may be a preference for put options instead of calls.

11:30 am

Are call buyers exhausted? 3950 appears to be the upper limit to this retracement in SPX.

ZeroHedge writes, “A volatile overnight session in the S&P 500 has left in the middle of a range between 3900 and 3950.

If you look at SpotGamma‘s total S&P500 profile you can see the “box” the market is in, and whats curious is that this picture has remained the same for the past several sessions. In other words, its not “filling in”.

10:00 am

The GSCI Ag Index appears to have completed a late Master Cycle low yesterday. This has been a very shallow correction, but may give a new sell signal above the 50-day Moving Average at 391.11. The next major resistance may reside at the 2010 high at 570.50. After a bumper wheat crop in Australia, an infestation of mice may not only damage the new crop, but limit grain exports to stop the infestation from spreading to other countries.

ZeroHedge reports, “New South Wales and Queensland are being overwhelmed by a biblical wave of mice, which have taken over homes, stores, farms, hospitals, and automobiles. These nasty little rodents are eating everything in sight, leaving a path of destruction.

Reuters said, “the Australian state of New South Wales is suffering their worst plague of mice in decades after a bumper grain harvest.”

“At night… the ground is just moving with thousands and thousands of mice just running around,” farmer Ron Mckay told the Australian Broadcasting Corporation.”

8:00 am

Good Morning!

NDX futures nudged up to the 50-day Moving Average at 13163.23, but pulled back. NDX is on a sell signal, but hasn’t made much progress in the past month. NDX often leads the other stock indices at major turns, but, in this case, appears to be waiting for the rest of the market to catch up.

SPX futures appear to be testing the combination Short-term support an mid-Cycle support at 3899.51. However, it has not yet made a clean breakthrough. There is known to be a significant call option position at 3900.00, which may be giving it support. One noteworthy item I should mention, the high at 3983.87 on March 17 is exactly 12.9 months from the February 19, 2020 high. Yesterday happens to be the one-year anniversary from the 2020 low.

ZeroHedge reports, “US stock futures rebounded after Tuesday’s rout as Intel’s shares surged on plans to expand advanced chip making capacity, while investors looked to business surveys for March and another day of testimonies from Yellen and Powell. Futures on the S&P 500 and Dow Jones also pointed to a rebound in the underlying indexes which dropped Tuesday amid a setback for reopening favorites. Stable bond yields and assurances by Powell on inflation risks has helped allay fears that a growth breakout will force tighter central-bank policy.

At 715 a.m. ET, Dow E-minis were up 135 points, or 0.4%, S&P 500 E-minis were up 18 points, or 0.5% and Nasdaq 100 E-minis were up 108.5 points, or 0.83%.”

Despite the positive news this morning, the NYSE Hi-Lo Index closed on an unmistakable sell signal at -46.00. The internals are crumbling while the surface appears calm. It appears that today was a good day to return from my brief vacation. This may be a good sign that quarter-end rebalancing may have started.

Yesterday’s low may be the culmination of this very stretched Master cycle at 281 days. VIX futures are hovering just beneath 20.00. This morning’s low at 19.87 happens to be the Fibonacci 61.8% retracement value of the bounce to 21.58. That suggests a high probability of a breakout above the 50-day Moving Average at 23.43, possibly today. This would give us a confirmation of the already low NYSE Hi-Lo Index.

TNX may already be recovering from a brief retracement. The Cycles Model calls for trending strength that may continue through the week after (April) options expiration.

ZeroHedge remarks, “After stocks just saw their best 12-month performance since 1936, it should not be a total surprise that Treasuries have suffered… but the extent of the bond bloodbath is almost unprecedented.

After $17 trillion of liquidity was gushed across the global markets (raising all equity boats), the recent prospect of resurgent inflation has pushed government and corporate bonds around the world to their worst start to a year this century.

Source: Bloomberg

Bloomberg reports that the notes have lost over 3.7% so far in 2021, according a Bloomberg Barclays index of investment-grade securities across currencies going back to 1999. That’s worse than for similar periods in previous years, even after dip-buying in recent days.”

ZeroHedge also reveals, “In recent weeks we have been pointing out the stark divergence between markets in various geographic time zones, most notably the variance in equity “moods” between the Europe and US, where it often appears that there are two regimes: one ending when Europe closes and another starting, with both usually mirror images.

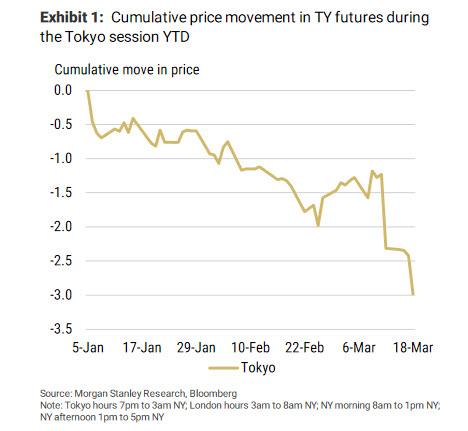

But while we mostly focused on how geography impacts stock markets, a far more interesting observation was made this week by Morgan Stanley’s chief rates strategist Matthew Hornbach, who over the weekend identified the origin, if not quite the identity, of the persistent seller of Treasurys over the past few months, who has sparked such a violent rout across not just the US rates space but also stocks and other core assets.

As the following remarkable chart from Hornbach makes very clear, the cumulative downward price movement in Treasury futures has been concentrated in the Tokyo session. Furthermore, after a brief respite in the first week of March, selling in the Tokyo session accelerated dramatically ahead of the FOMC meeting and it continued afterward.”

USD futures broke through mid-Cycle resistance at 92.45 this morning, reaching a high of 92.61. The 200-day Moving Average at 92.79 may be next, causing grief among USD short-sellers. The short squeeze has begun and may run through options expiration on April 16th. The target appears to be the combination Broadening Wedge trendline and Cycle Top at 96.14.

ZeroHedge remarks, “We’re dedicating today’s entire Data section to the value of the dollar and how this translates to US corporate earnings fundamentals. We use the Federal Reserve’s Trade Weighted Dollar Index rather than the DXY because it includes a broader and more representative basket of currencies. DXY doesn’t even have the Chinese yuan or the Mexican peso.

Three points on this topic:

#1: A long run look at the Trade Weighted Dollar Index (chart below, 2004 – present) shows how global currency markets trade through a cycle.

Global recessions/crises create safe-haven demand for the dollar. This is plainly visible in the 2008 – 2009 recession (dollar peak in March 2009, right as global equity markets troughed) and again in March 2020 (again at a low for global equities).

Now, looking across cycles (2006 – 2021); the dollar has clearly traded like a secular growth vehicle. It has, for example, appreciated 28 percent over the last decade. That is an annual compounded growth rate of 2.5 percent. Across the entire timeframe pictured here, the dollar is up 11.6 percent, for a 0.7 percent CAGR. Over the same timeframes, the euro is exactly flat to the dollar since 2006 and down 15 percent over the last decade, just to call out one major non-dollar global currency.

Takeaway: whenever you hear that the dollar is about to lose its reserve currency status or otherwise implode, remember this chart. No one would call the last 16 years the most stable or predictable in America’s history. But the dollar has done just fine. In short, if there’s a crack forming in the dollar’s secular, long run appeal we just don’t see it in this chart.”

WTI futures bounced this morning back above the 50-day Moving Average at 58.40, reaching an overnight high at 59.76. WTI has given a sell signal, so the time to go short or sell longs is on the bounce. It is difficult to determine whether it will be involved in the quarter-end rebalancing, since there appear to be anomalies in the Current Cycle through the first week of April.

ZeroHedge reports, “Crude prices crashed today, extending recent losses with WTI back below $58 at six-week lows amid dimming prospects of a steady recovery in demand from Europe to India.

“The weakness in crude prices isn’t likely to go away in the coming weeks, even as U.S. refinery utilization recovers to pre-storm levels,” said Fernando Valle, a Bloomberg Intelligence analyst.

“There is still the resurgence of Covid-19 in Europe and Asia, and refinery maintenance in China and these are likely to keep international demand weak for U.S. crude.”

Tonight’s API-reported inventory data will give us the next trend direction

API

- Crude +2.927mm (-900k exp)

- Cushing -2.282mm

- Gasoline -3.728mm

- Distillates +246k

After four straight weeks of builds, analysts expected crude stocks to draw this week, but once again (if API is right) we saw a crude build. Gasoline stocks drew down once again.”