3:16 pm

SPX made a marginal new all-time high at 3983.87. It may go even higher, as I mentioned this morning. However, it has made the requisite number of Waves within the time allotted in the Master Cycle (261 days). Be on the alert. Should SPX decline below 3935.00, it would constitute an aggressive sell signal.

VIX made a new low at 19.24 on day 275 of its Master Cycle, making it a very stretched one. The NYSE Hi-Lo opened at 24.00, the lowest since February 26, and showing weakness. Tomorrow will give us the official close, as the data generally lags the market.

ZeroHedge remarks, “Neil Dutta at Renaissance Macro sums up today’s nothingburger from The Fed:

“Passive easing continues. GDP has been revised up. Inflation has been revised up. Unemployment revised down. Despite all this, the median dot still at zero through 2023 though a few more see a hike. Chair Powell probably has time to help these folks understand the new policy framework.”

* * *

Today’s market chaos is brought to you by the word “SLR” and the number “2023” – whether The Fed will mention its thoughts on the now-politicized Supplemental Liquidty Ratio exemption decision (which will spark turbulence in bank stocks and Treasuries); and whether the Fed’s forward-looking dot-plot of rate expectations is adjusted hawkishly for 2023 (if no adjustment, stonks will soar).

Going into the event, there was no fear.”

6:30 am

Good Morning!

Today the FOMC makes its news release on their outlook and critical decisions going forward (or not).

ZeroHedge observes, “It could be time for Jay Powells “taper tantrum” as SLR-stakes are high ahead of the FOMC meeting on Wednesday. The political pressure is building and the SLR-relief may not be prolonged. We enter the meeting leaning short in EUR/USD and bonds.

“The temporary exclusion to the SLR is a mistake that should not be perpetuated after it expires at the end of this month”

– House Financial Services Committee Chairwoman, Maxine Waters (D)

We have a big central bank week ahead of us, with scheduled monetary policy decisions from the Fed, Norges Bank, BoE and BoJ, and it could prove to be one of the most important weeks in the life of Jay Powell.”

SPX futures are holding steady, awaiting the 2:00 announcement. While having the appearance of being complete on day 261, the Cycles Model and Elliott Wave guidelines offer some further guidance. As seen on the daily chart, The Cycle Top is at 4032.24. Minute Wave [v] equals Minute Wave [i] at 4034.32. The Wave structure may have a maximum height near 4050.00.

NDX closed just above the 50-day Moving Average at 13146.41 but futures have weakened in the overnight session. Options gamma in the NDX are negative, but a large block of puts that are soon to expire may neutralize the bearish pressure on the NDX. A lot will depend on Jay Powell’s outlook. A simple “status quo” statement may ignite a taper tantrum that may propel stocks lower.

ZeroHedge reports, “S&P futures edged lower, European and Asian markets were mostly lower and Treasury yields climbed sharply ahead of a key Federal Reserve meeting at which officials will deliver their outlook for the economy amid an overheating recovery that risks stoking inflation, and where all eyes will be the median 2023 dot for a potential hawkish signal that sends yields soaring.

At 0715 a.m. ET, S&P 500 E-minis were down 14 points, or 0.34% and Nasdaq 100 E-minis were down 148 points, or 1.13. The FAAMG stocks all slumped while Fuel-cell firm Plug Power Inc. plunged more than 20% in pre-market trading after it disclosed accounting errors.

The 10-year TSY yield ticked up to a new 13-month high of 1.6656% ahead of the policy decision, with market-implied inflation expectations are at 12-year highs even after yesterday’s 20-year bond auction drew stellar demand…

…. hammering demand for high-growth technology stocks, and sending Nasdaq 100 futs tumbling.”

VIX futures have risen steadily in the overnight session to 20.55. Today is options and futures expiration for the VIX. The Cycles Model suggests that yesterday may have been the Master Cycle low on day 274, a stretched Cycle. However, FOMC days have been known to evoke wide swings in volatility in either direction. We may see a momentary dip (at the FOMC announcement) to fill the open gap at 17.54 – 18.21, should the SPX rise over 4000.00.

USD futures are higher this morning. The Cycles Model shows trending strength this week and possibly continuing into early April. The strength of the USD may be dependent on rising yields in the 10-year Treasury note.

TNX is surging higher this morning. 10-year futures made a new high not seen since January 2020. Should Powell attempt to allow inflation to ” moderately overshoot,” we may see interest rates continue to rise through late April. Given that probability, I am not sure of the Elliott Wave structure. I had mentioned earlier that TNX could go as high as 17.00. That now seems to be a good probability. Should the rally continue through April, 20.00 may be a realistic target.

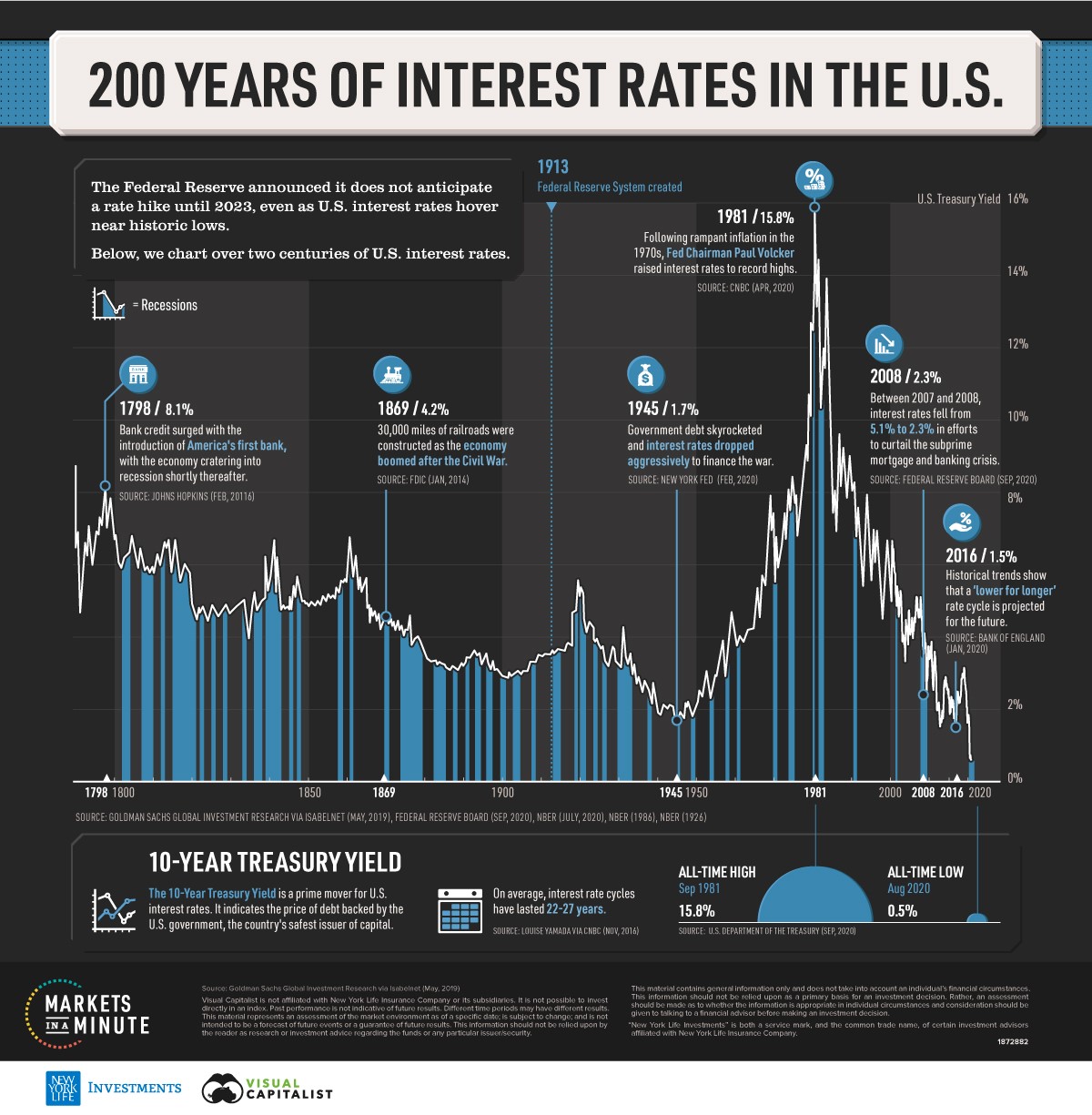

RealInvestmentAdvice gives some guidance, “What Interest Rate Triggers The Next Crisis?

- The Ten-year U.S. Treasury note yields 1.61%.

- 10-year high-quality corporate bonds yield 2.09%.

- The rate on a 30-year mortgage is 3.05%.

Despite recent increases, interest rates are hovering near historic lows. We do not use the word “historic” lightly. By “historic,” we refer to the lowest levels since the nation’s birth in 1776.

The graph below, courtesy of the Visual Capitalist, highlights our point.

Despite 300-year lows in interest rates, investors are becoming anxious because they are rising. Recent history shows they should worry. A review of the past 40 years reveals sudden spikes in interest rates and financial problems go hand in hand.

The question for all investors is how big a spike before the proverbial hits the fan again?