3:25 pm

NDX has challenged the 50-day Moving Average at 13146.49. Although it has bounced above it, it may close beneath it, creating a sell signal. Best wishes!

ZeroHedge comments, “With less than 24 hours to go until one of the most closely watch Fed announcements in a long time, the VIX finds itself hanging just below 20, the gamma gravity in the S&P is at 4,000 while dealers remains short Nasdaq/QQQ gamma (which however is shrinking by the day). In short, depending on what Powell says (we previewed how market would respond to a hawkish… and dovish Fed), markets could tumble or surge.

A quick rundown of the key technical factors ahead of tomorrow’s 2pm announcement:

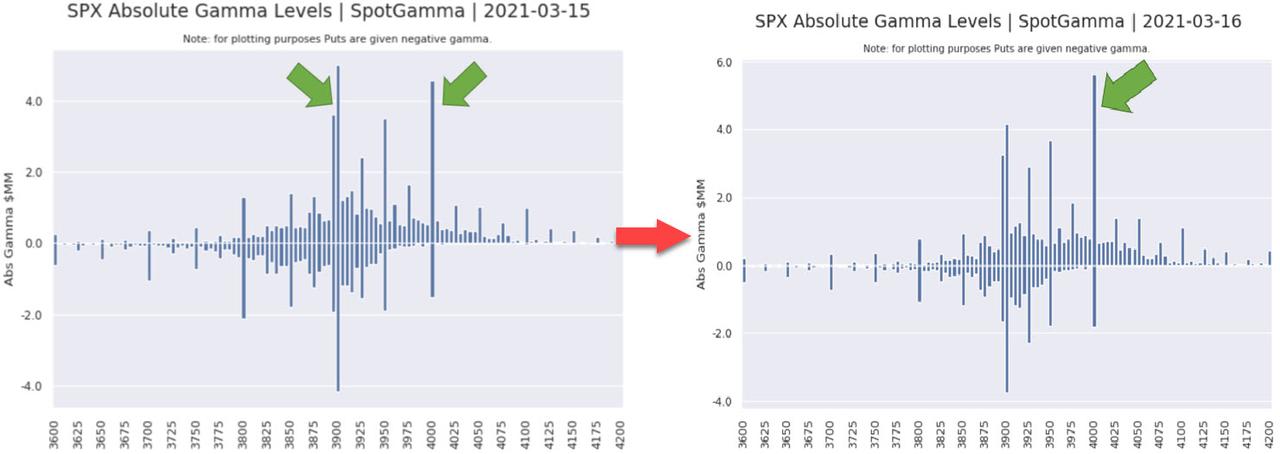

As our friends at SpotGamma note, the 400/4000 Call Wall in SPY/SPX has grown in size to over $5BN from yesterday – 10k 4000 strike calls were added yesterday, along with 100k SPY calls (to 400) – which increases its “pull” and yet total gamma is little changed in the S&P500 (that said, due to the FOMC tomorrow SG does not expect much movement today a forecast which has so far proven accurate).

On the other hand, Nasdaq/QQQ gamma remains negative, but that continues to shrink and SG notes that the upcoming March op-ex should flush out the remainder of that negative gamma position.

7:45 am

Good Morning!

NDX futures challenged the 50-day Moving Average at 13137.42 by rising to an overnight high of 13167.62. While the bearish structure may have weakened, it is not gone. The 61.8% Fibonacci retracement level is at 13241.33. Today is day 260 of the current Master Cycle for the NDX and SPX and day 263 for the DJIA. The reversal is imminent.

ZeroHedge reports, “Exactly one year ago today, the financial world as we know it was on the verge of collapse, with the Dow Jones plunging to 20,000 after the VIX exploded to a record 82.69.

Fast forward to today, when the market is about 66% higher, and on Tuesday morning futures on both the S&P 500 and the Dow Jones edged higher hitting fresh all time highs – the Dow notched its sixth consecutive all-time high on Monday on optimism over a $1.9 trillion fiscal stimulus package – for the second day in a row while contracts on the Nasdaq 100 rose about 0.5% by 730 a.m. ET, pointing to an extension of a rebound in technology stocks that were at the heart of February’s selloff. The Nasdaq 100 is still about 5% below its Feb. 12 record closing high. Traders were looking ahead to today’s industrial production and retail sales data (which as a reminder, will be a huge miss), while the Federal Reserve was set to kick off its two-day policy meeting.”

SPX futures made a new all-time high at 3964.38. Futures are currently 12 points beneath the cash market. It is possible that it may continue to rise to the Cycle Top at 3985.40. Another possibility may be the daily Cycle Top at 4037.69.

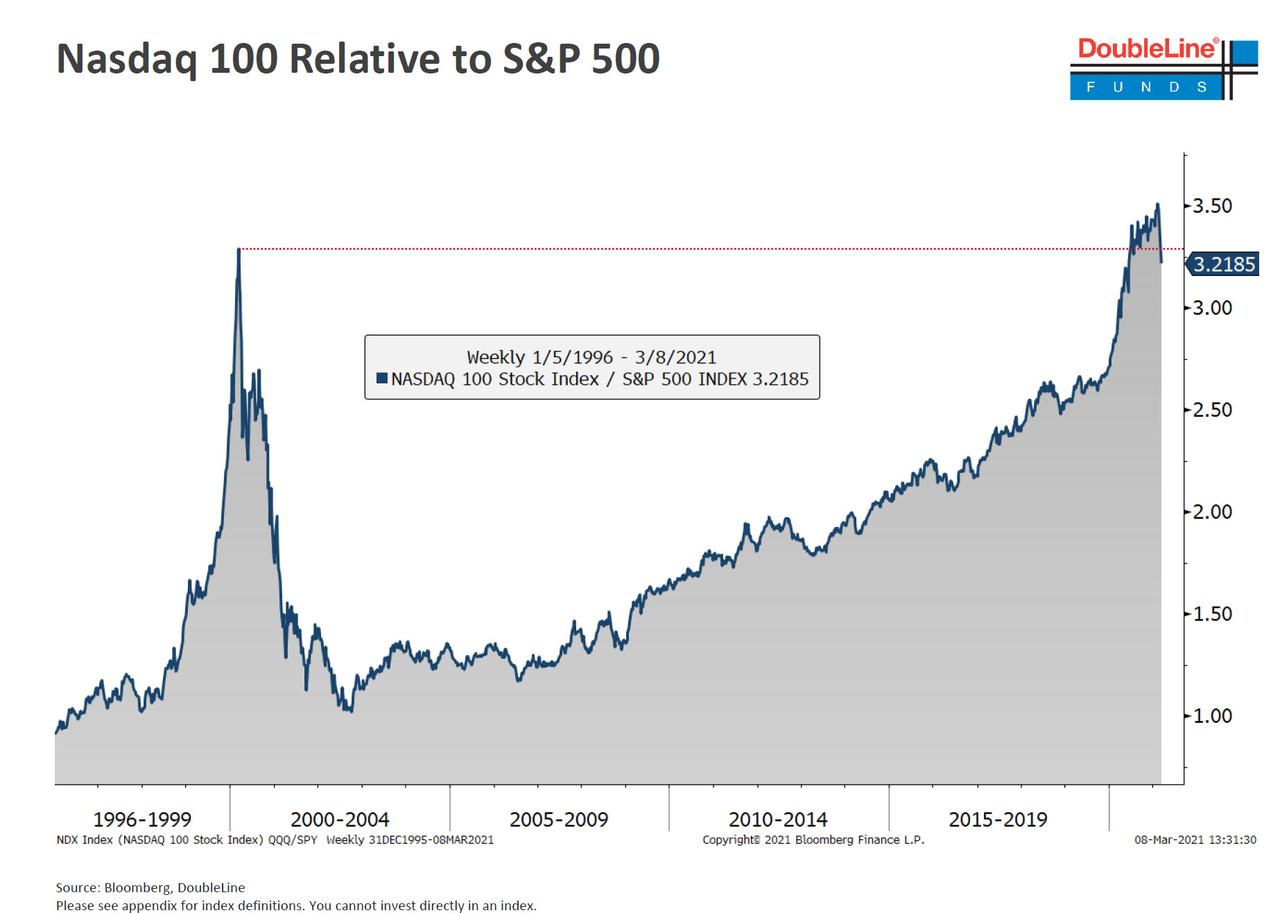

ZeroHedge remarks, “Last week in his latest Doubleline webcast, Jeff Gundlach presented a remarkable chart, one showing that the ratio of the Nasdaq to the S&P 500 has been pulled lower (due to Nasdaq underperformance coupled with strength in value stocks) and is now right on its dot com bubble peak levels.

Picking up on this chart, over the weekend in his latest Bear Traps Report, Larry McDonald wrote that “we are sitting on an incredibly important turning point” adding that “the world’s first and second most liquid and arguably most important stock indices are sending important rotation signals. In our view, both tech and growth equities outperformance run is over and the rotation to value and commodity exposed equities has begun.”

VIX futures made a new low at 19.81 this morning. It is possible that the VIX may decline lower than the February low, which may advance the Wave [B] structure. It would make sense that the Master Cycle would terminate at a lower low (beneath 19.69). A rally out of that low may be explosive.

TNX eased down to 15.88, then bounced back above 16.00. The Cycles may allow a retracement to the support levels between 12.38 and 14.22. From there, TNX may resume its advance through late April.

ZeroHedge observes, “Being dovish is harder than it looks for the FOMC. We expect two hikes in the 2023 dots. The consensus probably is close to expecting a single hike. If we are right, the initial response would probably be to add another half hike to the three already priced in by end-2023, taking the USD higher. But we think the Fed can present its dots as good news — a maximum employment soft landing is approaching quicker than expected. However, continuing the attitude of laissez-faire for long bond pricing would invite investors to take yields higher as economic data improved, even if the FOMC stuck with zero hikes in the dots.

How quick come the reasons for approving what we like

We think the FOMC will have a hard time expressing concern about asset markets with the S&P at an all-time high on 12 March, despite 10Y UST yields at post-February 2020 highs (Figure 1). Focus has been on the FOMC ‘dot plot’ in recent days, but if the FOMC and Fed Chair Powell do not push back against current yield levels, investors are likely to take yields higher as better data arrives.”