2:36 pm

The NYSE Hi-Lo is now on a confirmed sell. This is the final piece of the puzzle saying, “go short, young man!”

1:05 pm

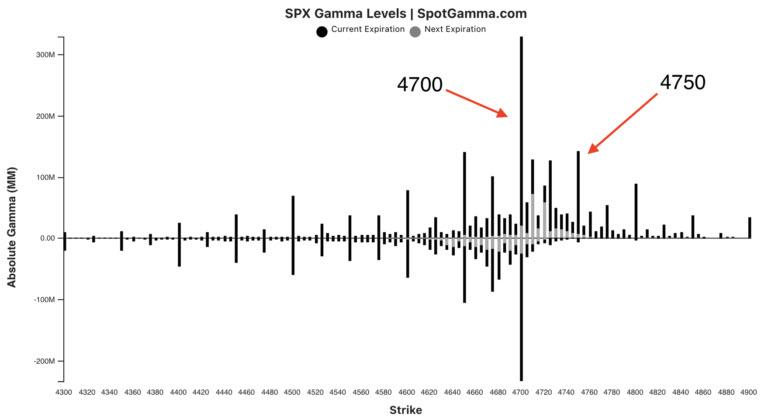

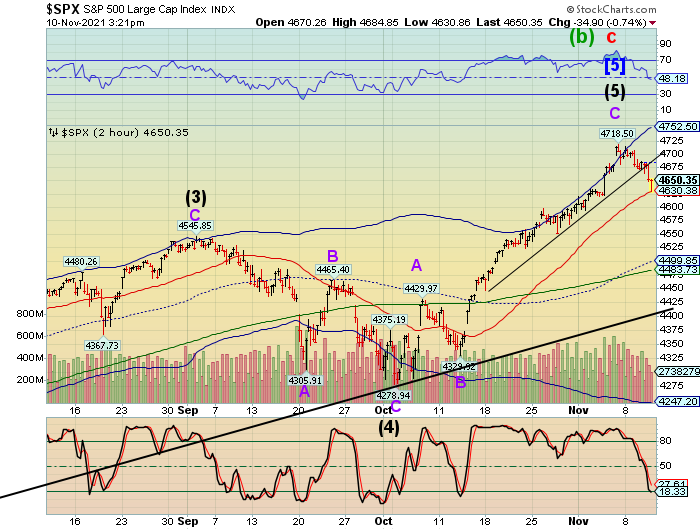

SPX is looking weak after it has completed an impulsive decline. Normally we may see a bounce back to Short-term resistance at 4688.70 by the weekend. This poses a dilemma for those not having made their move, especially over the holiday-shortened week. For those who have sold long and gone short, it is time to be patient. Others, who are waiting for the “right moment” may get whipsawed. For myself, having made my move, I intend to relax and enjoy Thanksgiving with my family. I may make a shortened commentary tomorrow, but Friday will be very busy from the word “go.”

ZeroHedge explains, “Something odd happened today. Treasury 10- and 30-year TIPS fell to session lows after the Fed postponed Tuesday’s scheduled purchase operation targeting the 7.5- to 30-year sector until Wednesday.

“Due to technical difficulties, today’s Treasury outright purchase operation – scheduled for 10:10 AM in the TIPS 7.5 to 30 year sector for up to $1.075 billion – is being rescheduled,” Federal Reserve Bank of New York says.

“It is now scheduled to take place Wednesday, November 24, 2021 at 11:00 AM,” New York Fed says Tuesday on its website

TIPS prices fell quickly on the news…”

12:30 pm

Yesterday morning I reminded that gold was on a sell signal. Well. here it is. Today gold declined further to 1781.85, beneath the 50-day Moving Average at 1790.83. The sell signal may continue through early January with a likely test of the Head & Shoulders neckline at 1675.00. Pundits aren’t happy.

ZeroHedge notes, “Good Morning. Monday morning saw a massive sell order hit the Gold futures market with almost reckless abandon. While no-one who is speaking knows why the market acted this way, we do know that it was one of three type players. It always is.

Someone Sold $2.2 Billion of Gold in 2 minutes Monday…”

7:45 am

Good Morning!

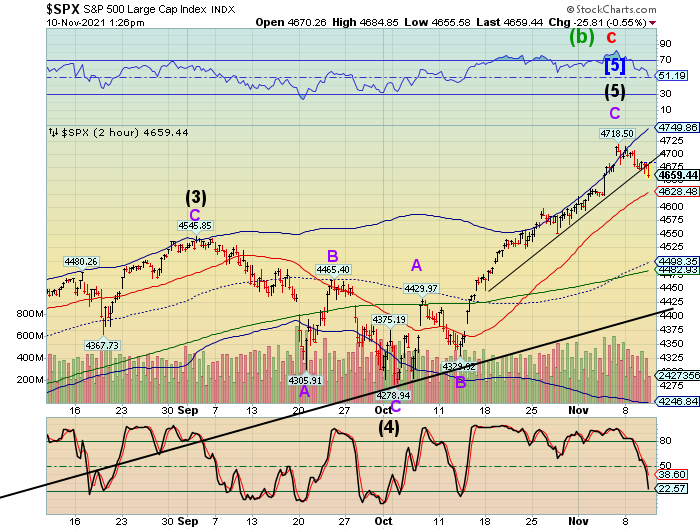

SPX futures are wobbling around the close after declining to an overnight low of 4658.10. It has made a “Key Reversal” by making a new all-time high, then closing beneath Short-term support at 4688.68 and the Wave (5) trendline at 4725.00 for an aggressive sell signal.

My original thought was that the SPX might flash crash after the November 8 high, then make a comeback to new all-time highs through January. It appears that this assessment was premature. The uptrend from March 23, 2202 now appears complete. The Cycles Model now posits that a 2-month decline awaits the SPX ending in the last week of January. Should that be the case, it is possible that the SPX may decline to “Point 6” of the Orthodox Broadening Top near 2100.00. In order to do that, SPX must decline beneath the bold trendline near 4400.00 in the next few weeks. Fasten your seatbelts.

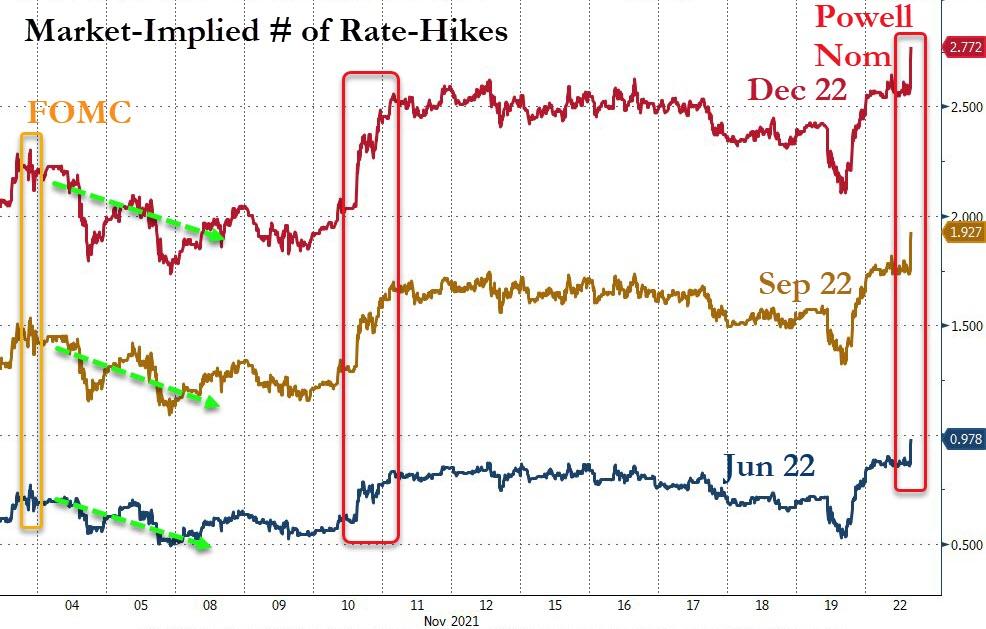

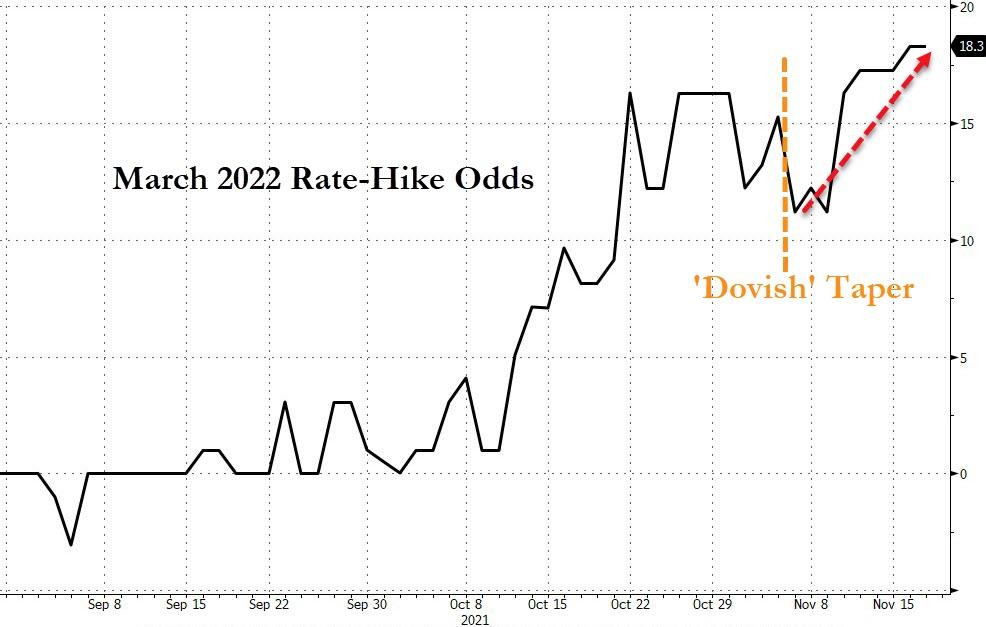

ZeroHedge reports, “US equity futures continued their selloff for the second day as Treasury yields spiked to 1.66%, up almost 4bps on the day, and as the selloff in tech shares spread as traders trimmed bets for a dovish-for-longer Federal Reserve after the renomination of Jerome Powell as its chair. At 8:00am ET, S&P futures were down 2.75 points or -0.05%, with Dow futures flat and Nasdaq futures extended their selloff but were off worst levels, down 41.25 points or 0.25%, after Monday’s last-hour furious rout in technology stocks.

VIX futures broke out above its November 10 high, rising to 20.83. It is officially on a buy (SPX sell) signal. The next resistance appears to be the Cycle Top at 23.40. VIX has two upcoming Master Cycles, the first in the last week of December and the second at the end of January, while SPX only has the second. Tis may make for some interesting volatility patterns through the year end.

The NYSE Hi-Lo Index closed at 6.00 after rising to 93 at mid-day. The item that apparently throws off the Hi-Lo count intra-day is that ETFs may be included, double and triple counting the new 52-week highs and lows. They are taken off the count after the close, so intra-day measures may be misleading.

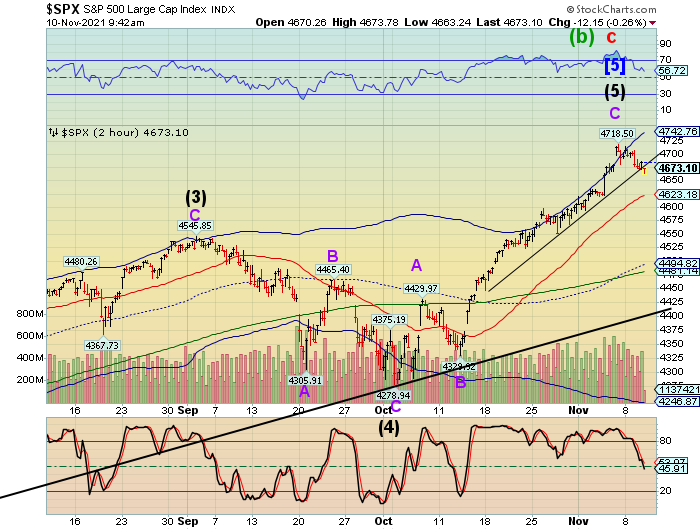

Yesterday’s close was low enough to count as a sell signal, pending today’s open.

NDX futures declined to 16276.60 this morning, crossing beneath the trendline at 16350.00 and giving a potential sell signal. It also made a huge Key Reversal, indicative of a potential change in trend.

The NDX Hi-Lo Index plunged to new lows not seen since March of 2020, confirming a sell signal. The Hi-Lo Index was negative since last week, despite making new all-time highs. Tis indicates a lack of confidence in all but the mega-caps.

TNX has broken out above the previous November high and may be overtaking the October high, as well. The Cycles Model suggests a continued rise in rates through January options expiration.

ZeroHedge observes, “Investors are fretting over the prospect of a “Fed Taper,” but history shows such will likely be good news for the bond market. Currently, it doesn’t seem that way, with rates rising post-announcement. As noted by CNBC:

“While the Fed has gone into policy retreat before, it has never pulled back from such a dramatically accommodative position. For the past eighteen months, it bought at least $120 billion of bonds each month, Such provided unprecedented support to financial markets that it now will walk back.

The bond purchases have added more than $4 trillion to the Fed’s balance sheet which now stands at $8.5 trillion. Roughly, $7 trillion of which is the assets bought up through the Fed’s quantitative easing programs. The purchases helped keep interest rates low. Such provided support to markets that malfunctioned badly during the pandemic, and fueled a powerful run for the stock market.”

Previously, when the Fed began to taper their bond-buying programs, the market buckled as the “risk-on” trade reversed.”

USD futures rose to 9662 in the overnight market before a brief pullback that may last to the end of the week. Thereafter, a surge of strength is indicated through the month of December.