11:00 am

The Banking Index, proxy for market liquidity, has finally declined beneath Intermediate-term support at 138.44. BKX declined beneath its Cycle Top support on November 3, but stayed glued to it for almost two weeks. Today its departure signals a confirmed sell signal, suggesting liquidity may be draining out of the market.

ZeroHedge suggests that market observers are still caught in a “straight line” thinking process, “Being ‘rationally irrational’ one more time

It’s no longer a secret that markets are irrational due to central bank action, and where we see suggestions of less action, they are increasingly volatile. This is taken as a bad thing because we prefer markets under conservatorship, like poor old Britney Spears was until recently. (“Get out there and perform, stocks/yields!”) The establishment loves hearing “Oops, I did it again” and/or “Hit Me Baby One More Time,” and it is rationally irrational to do so given the money keeps flowing to them. Other headlines today also show the same rationally irrational thinking.”

10:55 am

SPX hsd broken away from the trendline, giving us an aggressive sell signal. confirmation comes at the crossing of Sort-term support at 4672.93.

ZeroHedge observes, “As we contemplate next week’s ‘quiet’ Thanksgiving week, ahead of tomorrow’s options expiration, traders are bracing for the now ubiquitous volatility storm that occurs on the 3rd Friday of the month… and this one will be a doozy!

Bloomberg notes, the total number of outstanding contracts on equity, index and ETF options expiring stands at 95.5 million, a hair away from 95.6 million in July, data compiled by Susquehanna International Group’s Souhow Yao show. That was the most for any month ever, when excluding the expiration of quarterly options or the so-called long-dated options, or LEAPS, that have been listed for longer and accrued a higher open interest.”

7:50 am

Good Morning!

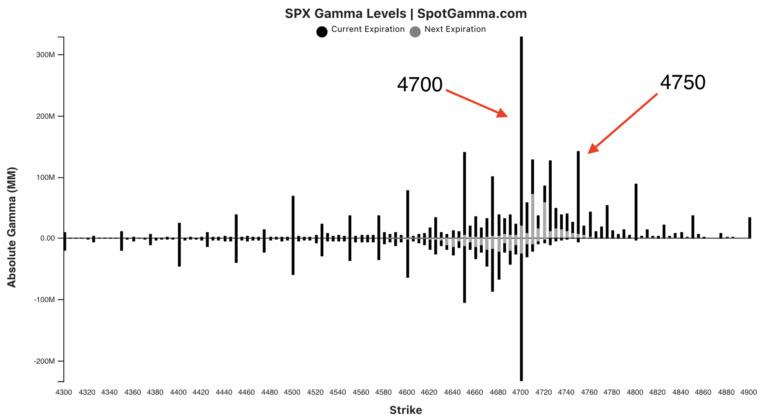

SPX futures rose to 4707.40 this morning without making a new high, but keeping the call options fully funded at maximum gamma. Today is day 259 of the Master Cycle, the second highest “hit” after day 258 for the Master Cycle.

Tomorrow’s options expiration show the Max Pain zone in the SPX at 4650.00. However, the index options implying institutional involvement are light, indicating a waning interest. However, the (retail) SPY options show an open interest in 282,000 call contracts vs 99,000 put contracts above 467.50, its Max Pain level. By the way, the number of (SPY) put contracts are rising, with less than 70,000 put contracts above 467.50 earlier this week.

ZeroHedge reports, “U.S. index futures rose again, trading on top of the massive 4700 “max gamma” level despite downbeat data out of Chinese tech names, as investors awaited the latest batch of unemployment data and taking comfort from signals that central banks will stay far behind the curve and keep pledges to overlook faster inflation rather than rush into rate hikes.”

The NYSE Hi-Lo Index closed below 30.00 for the first time since October 12 as institutional investors quietly leave the market. While we await a reading below 0.00 to have a sell signal, this number raises the cautionary flag on market participation.

VIX futures eased down to 16.654 this morning as it consolidates (coils) beneath overhead resistance at 18.53. Some traders will accumulate shares after the first breakout above resistance, as the probability of going higher is elevated. Others wait for the “sure thing,” the second breakout above the resistance level. The “failed” Master Cycle low on November 17 indicates the opportunity for accumulating shares at a lower level.

TNX (futures) made a low at 15.74, near Inttermediate-term support at 15.71 this morning. It is possible that a Trading (short-term) Cycle may have been made, allowing TNX to continue its rally. If so, TNX may have made a “running correction, where the bottom of Wave (c) is higher than the top of Wave (a). The Cycles Model suggest a continued rally to January options expiration.

ZeroHedge comments, “In the usual post-FOMC meeting jawboning circus, today we had not one but two Fed officials discussing not the topic du jour – Fed policy errors and soaring inflation – but something far more ominous: the broken Treasury market. Just days after a catastrophic 30Y Treasury auction which may well be the harbinger of what’s to come as the market realizes that i) tapering is tightening and that without the buyer of first resort we will finally get some price discovery and ii) inflation, contrary to the latest Fund Manager Survey, is not transitory, both Cleveland Fed president Loretta Mester and NY Fed president John Williams warned markets that the Treasury market is “not as resilient” as it should be, and that even modest stress could break it. Unfortunately neither of them admitted that it’s entirely the Fed’s fault that what was once the world’s most liquid market has become a political tool to be abused by central planners and power hungry politicians.”

USD futures pulled back to 95.65 in a short-term consolidation. The USD may continue to rise with treasury rates through the end of the year, per the Cycles Model.

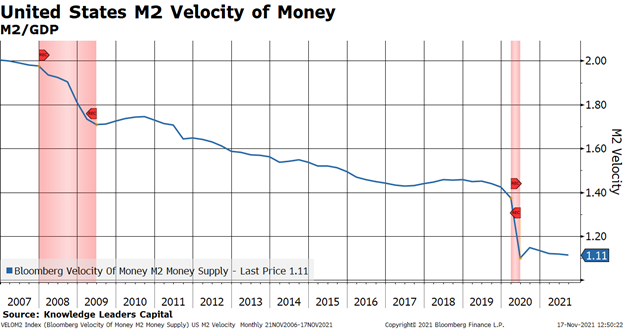

ZeroHedge observes, “A basic tautology that economists consider when thinking about monetary policy is the velocity of money. MV=PQ translates into Money*Velocity=Price*Quantity. Of course, price*quantity is nominal GDP while “M” is the money supply (for example, M2) while “V” is velocity, or the number of times the money supply turns over. A prominent feature of the post-Great Financial Crisis period has been the persistent decline in velocity, which is why the Fed has had to pump so much money into the system for so long. Absent an increase in the money supply, the drop in the velocity, all else equal, would have likely been the backdrop for a long recession.

But, it appears that the decade of falling velocity may have ended. Bank loans have made a strong turn upward since June.”

The GSCI Ag Index continues its rally to a potential breakout above its May high to new highs not seen in over 8 years. A potential overhead resistance level occures at 570.50, its March 2011 high. It is possible that it may reach that level by mid-December, its next Master Cycle interval.

ZeroHedge reports, “Cargill CEO David MacLennan has changed his mind about “transitory” inflation and now believes it will be more persistent with higher food prices in 2022. He blamed elevated food prices on snarled supply chains, labor shortages, and adverse weather conditions, among other things.

MacLennan highlighted that labor shortages are a significant challenge for the food industry. He said food processing plants across the country operate at less than full capacity, which drives down food output and prices higher as demand remains robust.

“I thought inflation in ags and food was transitory. I feel less so now because of continued shortages in labor markets,” MacLennan said during an interview at the Bloomberg New Economy Forum in Singapore. “That’s one of the inputs to the supply chain that we’re watching most carefully.”

ZeroHedge also comments, “The era of cheap meat is over. For those that are carnivores, that is really bad news. For decades, Americans have been able to count on the fact that there would always be mountains of very inexpensive meat at the local grocery store, but now those days are gone and they aren’t coming back. As I was writing this introductory paragraph, it struck me that what is happening to meat prices actually parallels what I wrote about yesterday. Just as the left doesn’t want us to use traditional forms of energy because they believe that doing so is “bad” for the climate, so they also detest that a lot of us like to eat a lot of meat because the production of meat causes levels of certain greenhouse gases to rise. ”

Gold futures continue to consolidate after making its Master Cycle high on Tuesday, day 253. There’s nothing like a a pullback after a “breakout” to get the bullish juices roaring. Unfortunately, as the USD rises into the new year, gold may be on the decline. Sorry, Jim!

ZeroHedge comments, “This is getting ridiculous. And that’s a good thing.

By “this,” I mean the price of gold, and by “ridiculous,” I mean repetitive to the point of absurdity. That’s OK. The prospects for gold from here are highly positive.

By now, readers are tired of my description of gold trading as range-bound between $1,700 per ounce on the low side and $1,900 per ounce on the high side, with $1,800 per ounce as the central tendency. That’s completely accurate but also highly repetitive, since it has held true with only brief and minor exceptions for the past year.”