3:10 pm

TNX has settled down to its session low after the Treasury auction this afternoon. It may retest its Intermediate-term support at 15.67 before resuming its rally.

ZeroHedge observes, “After last week’s catastrophic 30Y auction, traders were keeping a close eye on today’s sale of $23BN in 20Y bonds to see if it too would suffer from lack of demand following last week’s historic CPI print.

As Bloomberg’s Alyce Anders wrote ahead of the auction, the Fed and the Treasury “have done everything they can to support the doggy 20-year sector. The lack of a concession today and a well advertised relative value set up might mean the $23 billion offering should go fine even if it tails. That’s because the government cut its issuance size and the Fed left its new purchase schedule for 10-year to 22.5-year Treasuries untouched despite tapering Treasury buybacks by $10 billion per month.”

3:03 pm

If this Wave count is correct, we should see some downside in the final hour. An aggressive sell signal lies beneath Short-term support at 4669.79.

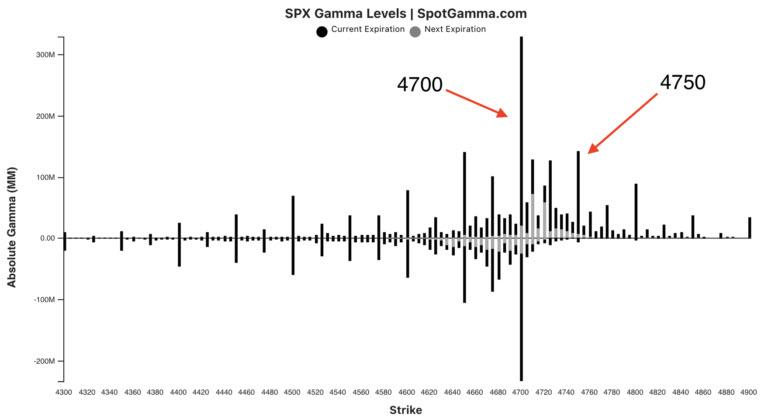

ZeroHedge observes, “Goldman’s quadrupling down on its year-end meltup call has been spot on so far, and the S&P overnight gravitated back up to the 4700 strike which continues to house the most $Gamma on the board at $8.8B, followed by the 4750 strike with $6.7BN.

And, as Nomura’s Charlie McElligott reminds us, heading into Friday’s op-ex, SPX/SPY Net Delta is 99.9%ile (since ’13)…”

8:00 am

Good Morning!

SPX futures made an overnight high of 4704.90 as it “stays in place” on day 258 of the Master Cycle. Thus far, yesterday’s high at 6714.95 may be the best candidate for the Master Cycle high. Today 4700.00 appears to be the Max Pain zone with calls dominating at 4710.00 and above and puts dominating at 4680 and below for options at the close of the day.

Friday, on the other hand, is a different problem. Calls dominate the options expiry all the way down to 4600.00. Max Pain is a 4595.00. That would damage the technical landscape, since the Ending Diagonal trendline is at 4675.00 and Short-term support (aggressive sell signal) is at 4662.32. The way I see it, a Friday close at 4700.00 would cause a lot of dealer pain, while a close beneath 4600.00 would give them an enormous profit.

While SPX is very close to making a new high, NDX and the DJIA are not, unless the enormous “pull” of the calls causes a melt-up to bring all the indices in line. In March 2000, the SPX and NDX made new all-time highs while the DJIA limped along to a secondary high. Today’s scenario could be compared to such a case.

ZeroHedge reports, “Price action has been generally uninspiring, with US index futures and European stocks flat after UK inflation climbed faster than expected to the highest in a decade, heaping pressure on the Bank of England to raise interest rates, while Asian markets fell as investors fretted over early rate hikes by the Federal Reserve after strong retail earnings dented the stagflation narrative. Ten-year Treasury yields held around 1.63% and the dollar was steady. Cryptocurrencies suffered a broad selloff, while oil extended losses amid talk of a coordinated U.S.-China release of reserves to tame prices. Gold rose. At 7:30 a.m. ET, Dow e-minis were down 14 points, or 0.04%. S&P 500 e-minis were up 1.25 points, or 0.0.3% and Nasdaq 100 e-minis were up 24.75 points, or 0.15%, boosted by gains in Tesla and other electric car-makers amid growing demand for EV makers.

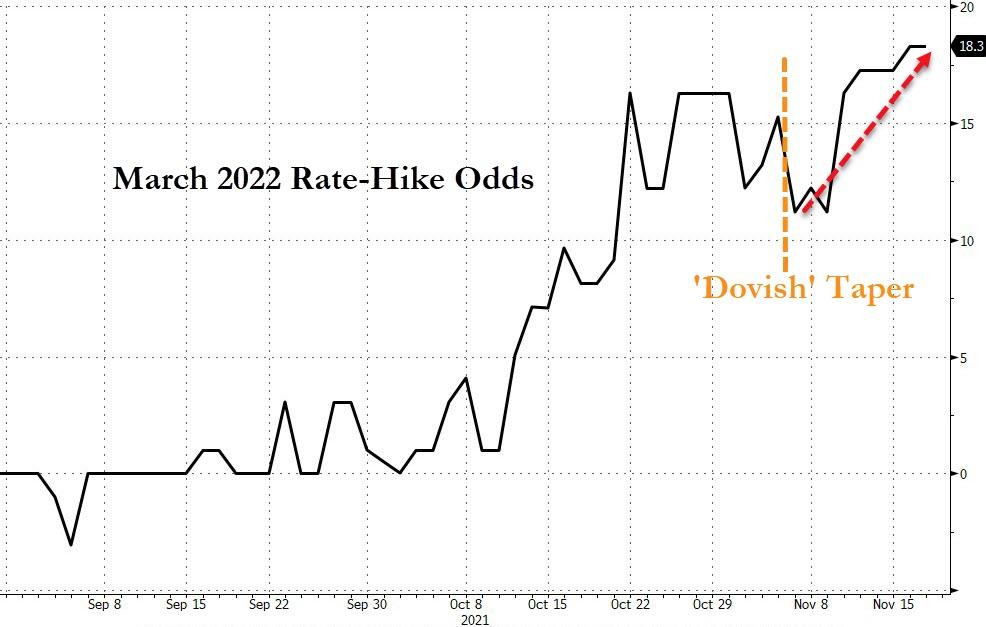

At 8:21 am ZeroHedge reports, “Too much of a good thing…

STIRs are continuing their hawkish trend, with the market now pricing a 19% chance of a rate-hike as soon as March 2022…

US Treasury yields are on the rise again this morning, with 30Y yields breaking out to one-month highs…”

VIX futures moves higher, but still within yesterday’s trading range. Today is day 258 of the VIX Master Cycle and possibly the last day for a new low, due to monthly options expiration for the VIX. MAX Pain in the VIX options is at 22.00 with puts dominating beneath that level. This could be a very interesting day.

TNX moved higher this morning, setting off jitters in the equities market. The Cycles Model suggests rising rates through Janusry options expiration.

Yesterday, ZeroHedge pointed out, “30Y Yields are back above 2.00% this morning, with rates having jumped notably in the last few days…

Nomura’s Charlie McElligott notes that, after the three week rolling squeeze in bearish fixed-income / underweight duration trades (helped by the epic global CB “rug pull” on prior hawkish rhetoric) has now allowed for resetting of shorts as the buy impulse fades…particularly from Systematic Trend.”

USD continued its melt-up to 96.27 this morning. The Cycles Model suggests a continued rise in the USD through mid-January.

Gold futures made a partial retracement of yesterday’s decline on day 254 of the Master Ccyle. This may set the stage for a definite change in trend after a complex sideways consolidation over the past year. The Cycles Model suggests a decline through the first week of January. The Triangle formation forecasts the final move before a reversal. This may be the reversal, not a breakout.

ZeroHedge comments, “Gold’s huge break out

Gold broke out of the huge triangle like formation that has been in the making for a long time. Time for a technical thread. The first obvious observation is that the shiny metal is well above the negative trend line and that the 200 day moving average is not sloping downwards anymore. The short term move has of course been powerful and gold is now somewhat overbought, but the price action in the recent squeeze is nevertheless interesting. First support we have down at the 1830 level.”