8:00 am

Good Morning!

NDX futures rose to 12329.00 this morning before reversing back beneath the upper Rising Wedge trendline at 12250.00. Yesterday’s action is viewed as a “breakout” by many, when in fact it is a throw-over leading to a reversal. What is interesting is that yesterday was the end of a Trading (60-calendar day) Cycle beginning May 20 and a 30-market day Cycle from the June 2 high. Order out of chaos.

In today’s op-ex, Max Pain is at 12090.00,, leaving room for a large decline. Calls are favored at 12100.00, but not heavily populated. QQQ ( close: 298.30) op-ex favors calls above 295.00 with long gamma starting at 300.00. Short gamma starts at 285.00.

ZeroHedge comments, “The Fed is hiking blindly into an economic downturn, putting pressure on risk assets unnecessarily.

The good news, with cash levels at the highest since 9/11 and equity allocation the lowest since the Lehman collapse, if the Fed stops sooner than many think, the second half of 2022 risk rally will be enormous (ZH: and they will: according to Michael Hartnett, the Fed will pivot in November, while Marc Cabana says QT will end well ahead of schedule).”

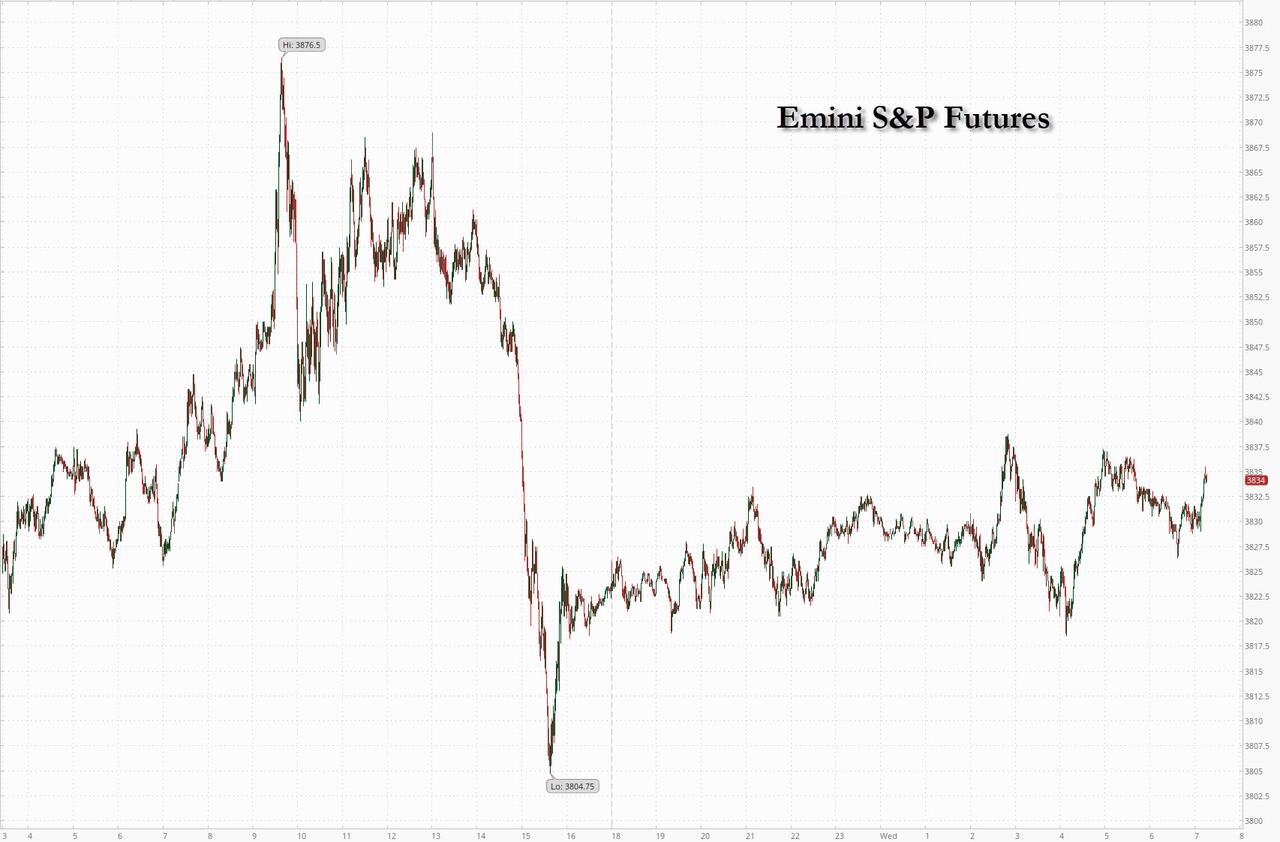

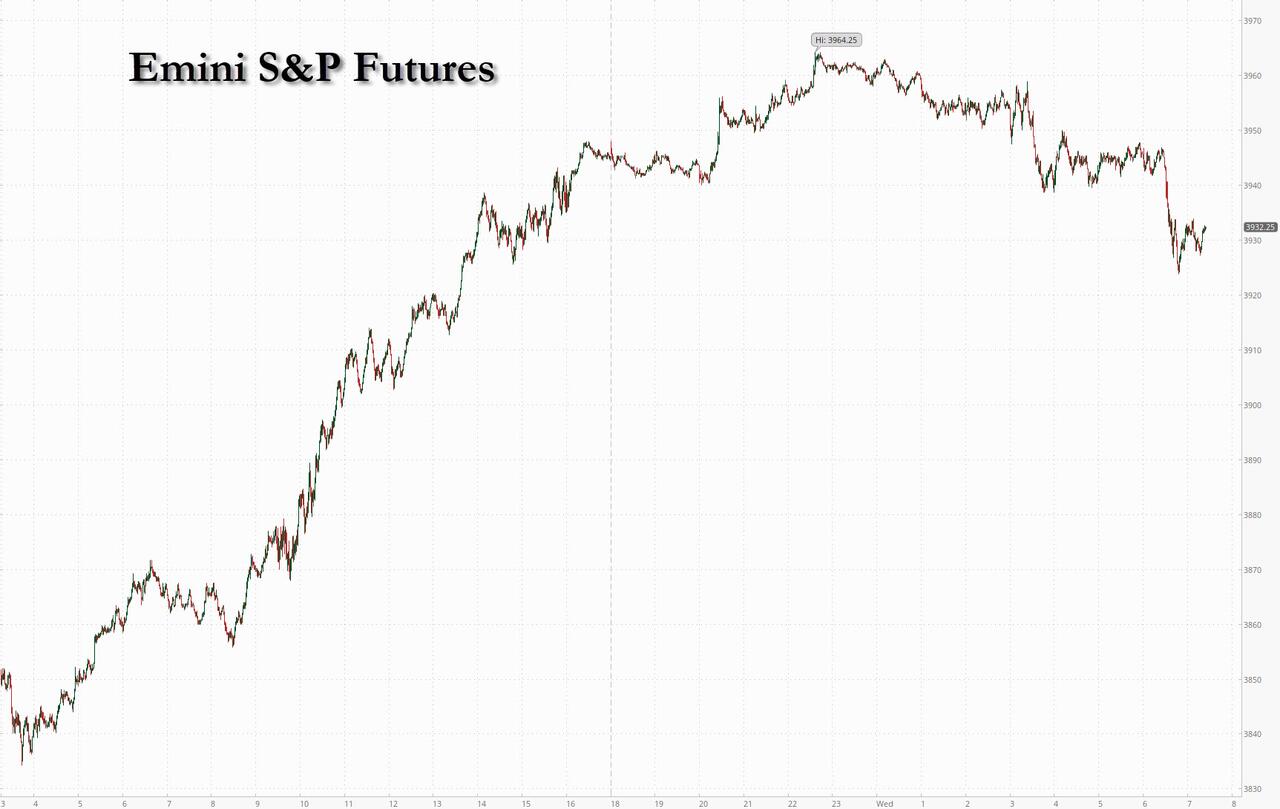

SPX futures rose to 3961.10 in the overnight session, but has since reversed back beneath the 50-day Moving Average at 3935.00. The Triangle is complete and the new decline is in play. There is some tension between a 12.9-day or a 17.2-day decline straight ahead. Since Wave A was 16 days in length, the latter length is favored.

In today’s op-ex Max Pain is at 3895.00. Long gamma begins at 3950.00, gaining intensity above 4000.00. There is no short gamma level that is discernible. An interesting time for a decline.

ZeroHedge reports, “What was a solid overnight rally which pushed global markets higher and US index futures as high as 3,964 after a beat in Netflix subs helped further ease market jitters, fizzled and then reversed around 6:30am ET, when the European Union officially proposed that the bloc cut its natural gas consumption by 15% over the next eight months to ensure that any full Russian cutoff of natural gas supplies won’t disrupt industries over the winter, with Commission president Ursula von der Leyen going so far as suggesting the EU would be able to enforce a slowdown in gas consumption.

The move which saw spoos slide more than 20 points from 3,947 to below 3,925 before rebounding, and sparked a reversal in haven assets, as Treasuries rose with 10Y yields dropping back under 3.0%, and the dollar index stabilizing after three days of declines…

VIX futures dropped to 24.15 before bouncing back into the green on day 259 of the old Master Cycle. The threat of a marginal new low is diminishing, although VIX may be sold here to reinvigorate the SPX rally. Today’s op-ex in VIX may be active. Max Pain is 28.00. Puts dominate beneath 26.00 with short gamma at 25.00 Long gamma begins at 30.00.

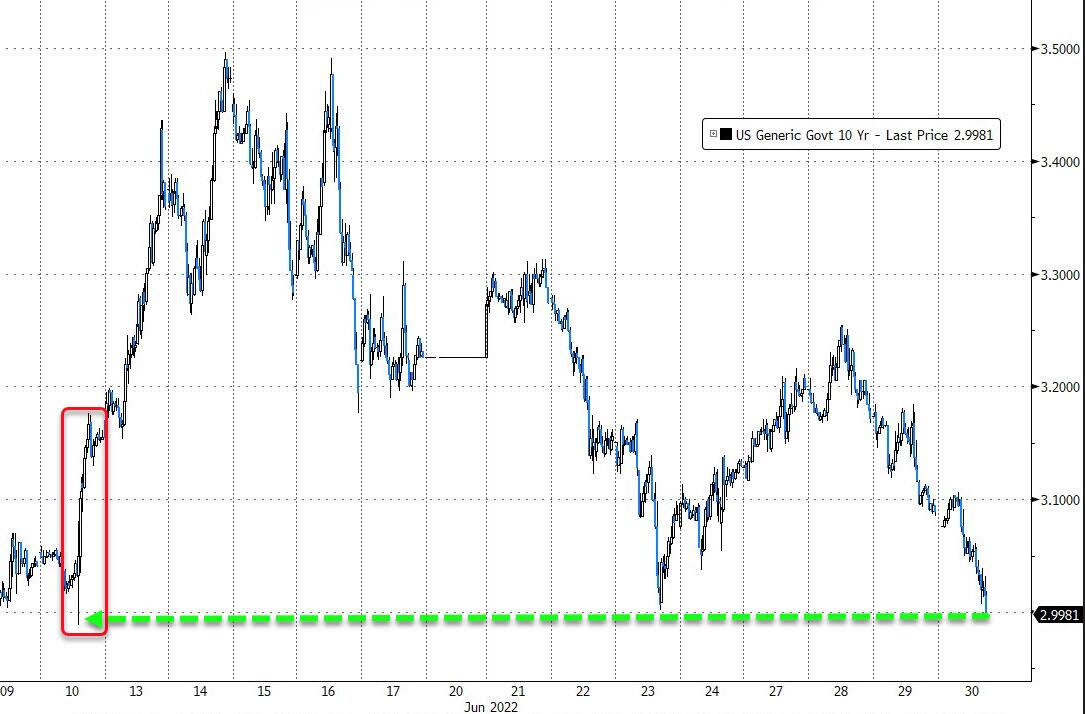

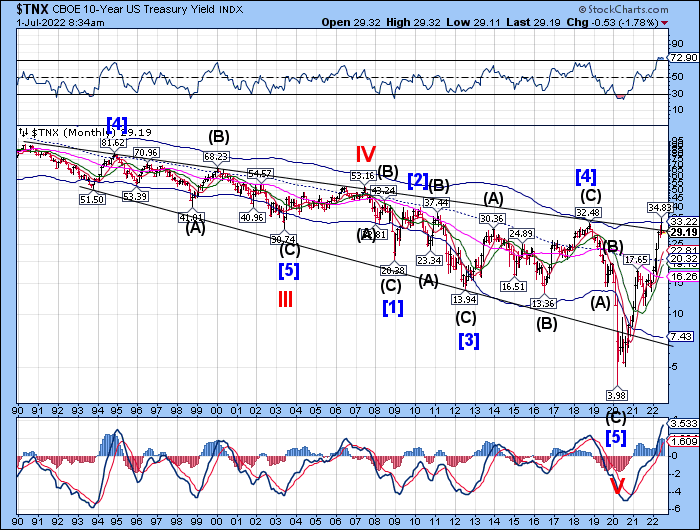

TNX slipped back beneath the 50-day Moving Average at30.06 this morning. Less than a week remains to complete the rally to the Cycle Top at 34.93. A rally of that magnitude in such a short period of time may be a real shock to the equities markets.

ZeroHedge comments, “Appearances can be deceptive. Especially those that seem self-evident at first sight.

On the face of it, it would seem that Treasuries around current levels offer investors a good deal. After all, for the better part of the past decade, such seemingly high yields have been elusive. However, at current levels, long-dated maturities show circumspection, but also reflect optimism about the Fed at the same time.

Obviously the current nominal yield of around 3% on 10-year Treasuries would only make sense if an investor believed that — if they held the bond until it becomes due — they would come out ahead if, on average, inflation is well less than the yield to maturity. What becomes of an investor who is buying 10-year Treasuries now?”

USD futures dipped a tick lower to 106.24 this morning before a bounce brought it back. Odds are igh that a rally may emerge to bring USD back above the Cycle Top and upper trendline, both near 106.99. The uptrend may resume beginning this weekend and lasting through the second week of August. Note that a spike in the 10-year Treasury yield may bring this about.

Crude oil futures have pulled back to 98.50 this morning, possibly on their way to mid-Cycle support at 94.72 before a rally to the 50-day Moving Average at 109.21 by mid-August.

ZeroHedge notes, “Solid risk-on moves in stocks, a weaker dollar, and a disruption along the Keystone pipeline were enough – in thin liquidity – to send oil prices notably higher (WTI back above $100).

“Right now liquidity is thin, people are away on holiday, there’s more machines than humans,” Amrita Sen, co-founder of consultant Energy Aspects Ltd., said in a Bloomberg Television interview.

“We can continue to trade in this very technical band. But structurally this is a market defined by underinvestment.”

Oil markets have been volatile in recent weeks as traders navigated concerns that a looming recession would hurt demand and the fallout from a stronger dollar against the signs of tight physical supplies.”