3:39 pm

BKX probed to its corrective high this morning before reversing back down on day 257 of its Master Cycle. I had originally considered Thursday’s low as a possible Master Cycle ending, but today’s rally makes more sense. The question this morning was, how to explain the jump in stocks after Goldman reported a 47% decline in profits?

The Cycles Model suggests a long decline through the end of September.

ZeroHedge reports, “Concluding the big banks’ Q2 reports, which had been at best mediocre with more banks missing than beating estimates, on Monday morning Goldman Sachs reported a 47% drop in second-quarter profits, as the Wall Street giant suffered from a slowdown in investment banking fees and plummeting revenues in asset management, offset by a jump in trading.”

2:58 pm

The days of short-squeezes are over. SPX has reversed out of the call-dominated zone above 3850.00 and is about to enter the short zone at 3840.00. It is back on a sell signal beneath the mid-Cycle support/resistance at 3882.00 and is challenging short-term support at 3841.08. In other words, short the bounce.

ZeroHedge lays it on the line, “There is a growing chorus of “hike fast and get it over with” coming from the market with an expectation that getting back to neutral fast will spark a recessionary environment that will prompt a pivot from The Fed back to easing rates and unleashing a fresh round of QE.

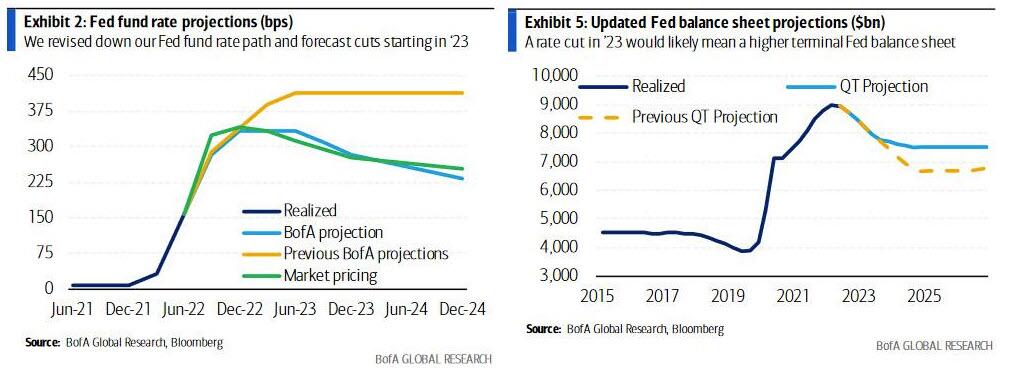

As we have recently detailed, BofA’s top Rates strategist, and former NY Fed analyst, Marc Cabana expects Powell to be forced to end QT much sooner than expected

We expect the Fed will stop QT with rate cuts due to the contradictory signal it sends on monetary policy and to simplify policy communications; the Fed will likely not want to be easing with rate cuts but tightening with QT.

Cabana reminds us that the Fed has established a playbook for such an action in 2019 when the Fed cut started cutting rates in July ’19 and simultaneously announced a cessation of QT. “

ZeroHedge further states, “While most analysts and traders were digging through Goldman’s stronger than expected Q2 earnings report which beat on revenue despite a nearly 50% plunge in profits and another quarter of dismal investment banking, but redeemed itself with stellar FICC numbers…

… which sent Goldman stock higher, for the fourth quarter in a row there was troubling disclosure in the bank’s Asset Management division (which overlaps with the verbotten Goldman Prop, which does but doesn’t really exist since banks still aren’t technically allowed to have prop trading post Volcker). Here, after a very disappointing Q3 2021, which saw a $820 million loss from the trade of public equities…”

7:30 am

Good Morning!

NDX futures rose above the 50-day Moving Average at 12090.43 over the weekend session and has since pulled back, still above the 50-day. A new peak at the open may move Wave 2 over, but the Cycles Model suggests this may be the final probe. NDX has spent 12.9 market days from the peak at 12175.95 and 43 market days from the peak at 12987.63 as of this morning’s open. The Model tells us that there may be another 17.2 days of decline to the upcoming Master Cycle Bottom, due the second week of August.

Today’s options expiration shows calls outnumber puts above 11800.00 and potential long gamma above 11900.00. Institutions are starting to buy calls again. QQQs (291.87) show calls dominate above 285.00 with potential long gamma at 290.00.

ZeroHedge observes, “On the one hand, what was the most bullish case for markets starting this month fizzled with a bang, when after a solid start to July and the best start to Q3 since 1980, stocks resumed their bear market slide, only to recover some losses toward the end of the week. In any case, the barely 1% rise in the first half of July was at best meh considering the lofty expectations for what has traditionally been the best two-week period of the year…

… for markets.

So as attention turns from what was a big dud of a strong calendar period, to what is already shaping up as a disappointing Q2 earnings season (with virtually all banks missing expectations across the board), the bulls are once again in retreat, and nowhere is this more obvious than in hedge fund positioning which according to Goldman’s Scott Rubner, “is so low, it has officially fallen off my chart.” Rubner then invites readers to take a look at some of this stuff, and points to Goldman’s Prime Broker hedge fund exposure, Futures Positioning, CTA, Risk Parity, noting that “I don’t think there is more marginal position left to sell, given large hedges vs. fundamental positions already in play.”

SPX futures rose to Intermediate-term resistance at 3901.72 and has stalled, possibly ending the Triangle formation that is Wave B. Should Wave C reach equality with Wave A, SPX would be targeting 3360.00, fulfilling the Head & Shoulders formation. There is a probability that the anticipated Wave (3) of [3] may go much deeper by the second week of August, when the next Master Cycle low is due.

Today’s expiring options show calls dominate above 3850 and puts crowd out calls at 3840.00 in a thinly populated op-ex. Gamma levels are not discernible at this time.

ZeroHedge reports, “US equity futures and global markets stormed higher, as the dollar extended its slide from a record high as investors scaled back bets on how aggressively the Federal Reserve will tighten policy in response to growing recession fears which Bloomberg paradoxocially interpreted as “easing recession fears.” In other words, rising risk of a recession lowers the risk of a Fed-induced recession. Lovely.

In any case, Nasdaq 100 futures rose 1.2% and contracts on the S&P 500 added 1%, with spoos trading back over 3,900 and more than 5% above June’s closing low following Friday’s strong rally on renewed hopes that the Fed will end its rate hikes and soon start cutting rates as well as end QT. West Texas Intermediate crude oil also stormed higher, undoing all recent losses and traded near $100 a barrel while the Bloomberg Dollar Spot Index slipped 0.5%, extending a retreat from a record high. The benchmark Treasury yield rose back toward 3%.”

VIX futures are rising in the face of higher stock prices this morning after a probable Master Cycle low on Friday, day 254. VIX tends to lead the markets and tis may be a sign of an imminent reversal in the SPX. The final plunge in the VIX on Friday may have been meant to boost stocks in the face of monthly op-ex.

In Wednesday’s upcoming op-ex, Max Pain is at 29.00. Long gamma comes to life at 30.00 while short gamma dominates below 26.00.

SeekingAlpha observes, “Summary

- Last week could have been a disaster for the equity market if not for options expiration.

- The macro backdrop is deteriorating quickly, and that is likely to weigh on stocks heading into next week’s FOMC meeting.

- Can the market continue to rally, sure? But there continue to be many more reasons for it not to rally.

- Looking for a helping hand in the market? Members of Reading The Markets get exclusive ideas and guidance to navigate any climate. Learn More »

Stocks had a solid finish to the week, thanks to options expiration. But if it had not been for the monthly options expiration, last week would have been a disaster. The S&P 500 (SP500) was down more than 4% at its lows on Thursday morning but finished the week lower by around 1%. The end-of-week comeback was aided by the slow melt of the VIX index (VIX).”

TNX is rising again, but still beneath the 50-day Moving Average at 30.06. The Cycles Model suggests another week of rally, possibly to the Cycle Top at 34.74, before a substantial decline. The Model often calls for a return to the mid-Cycle support for the decline, but all indications are that it may be much deeper. The Weekly mid-Cycle support is at 15.30.

ZeroHedge admits, “The debate about recession risk is pointless. We are already in a recession. Real GDP (gross domestic product) in the United States declined at an annual rate of 1.6% in the first quarter.

The Atlanta Fed Nowcast shows a 1.5% contraction in the second quarter. But the underlying figures are scarier. According to the Atlanta Fed, “the GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022 is -1.5% on July 15, down from -1.2% on July 8”. That is an enormous negative change, -0.3% of GDP, in one week.

They go on to say that “the nowcast of second quarter real personal consumption expenditures growth and real gross private domestic investment growth decreased from 1.9% and -13.7%, respectively, to 1.5% and -13.8%, respectively”.

Investment is collapsing, consumption is barely kept alive and if we look at other components, imports are soaring while exports rise less than expected.”

USD futures pulled back to 107.05, testing the upper trendline of the year-long trading channel. The rally may resume with strength later this week as it has another three weeks of rally to the Master Cycle Top.