2:25 pm

SPY stalled at 384.00 and SPX at 3859.90, a 70% retracement. The complex pattern is emerging from this mess. The Wave formation shown above may be correct, should SPX not rally further. A decline beneath short-term support at 3835.00 may be construed as a sell signal. Institutional investors usually come back into the market before 3:00 pm. Their sentiment may become obvious.

10:49 am

This morning I mentioned that SPY options Max Pain was at 382.00. SPY was rallied up to 384.33 enabling the dealers and hedge funds offering today’s options to go short. This morning I mentioned that short gamma began at 376.00, near the Cycle Bottom at 374.07. Since then, short gamma has moved up to 380.00, with 89,175 put contracts in place! The Alternative is to simply go long and avoid short gamma altogether. Calls are favored above 388.00 and long gamma begins at 390.00, right in line with the 50-day Moving Average at 388.51 and Intermediate-term resistance at 391.76.

9:45 am

Today may be a whipsaw day, as SPX rose to the 61.8% Fib retracement level at 3843.20, then reversed. The market may have rewarded the institutional investors who are still long at op-ex, but now has to deal with retail, who are net short.

ZeroHedge observes, “Despite ISM surveys tanking, analysts expected US Industrial Production to eke out a 0.1% gain in June but they were wrong as output slumped 0.2% MoM (and May was revised lower also). There hasn’t been a weaker month since September 2021…

Source: Bloomberg

Only mining (+1.7% in June after rising 1.2% in May) kept the headline industrial production print positive.

Utilities fell 1.4% in June after rising 1.9% in May.”

7:40 am

Good Morning!

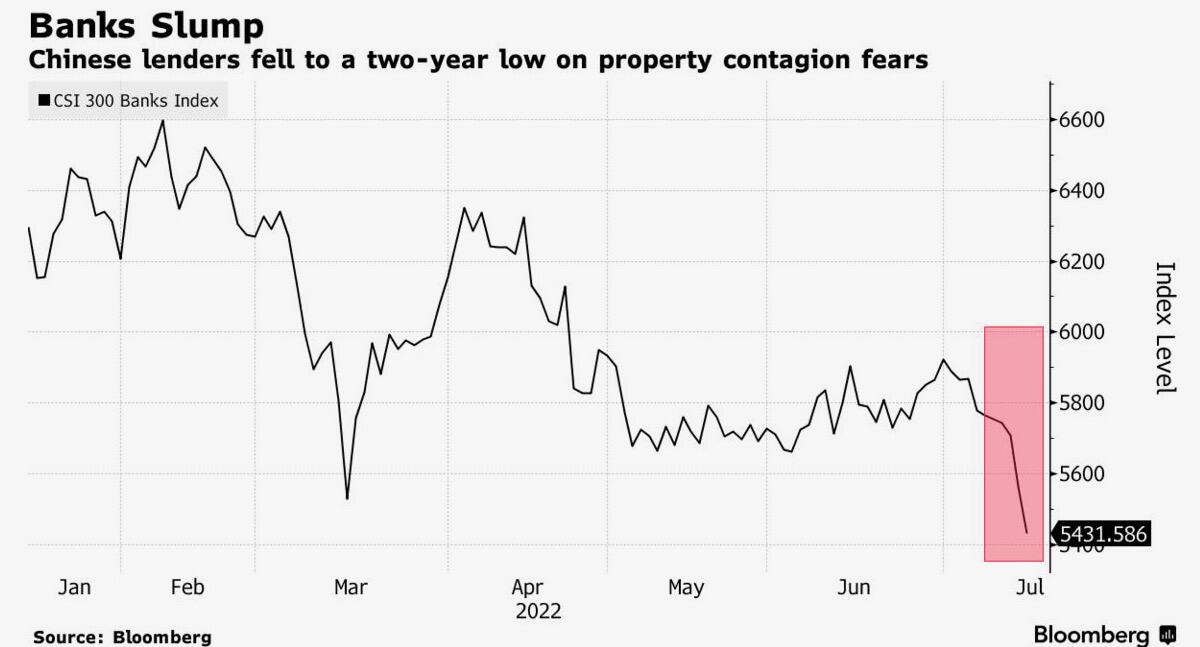

While op-ex is an important consideration today, we should not ignore other considerations across the globe. After Challenging the Lip of the Cup with Handle formation at 3315.00 in June, it has reversed back through it and today is threatening the 50-day Moving Average at 3227.13. The Cup with Handle formation proposes a potential 40% decline from the June peak to the possible August trough. Economic conditions in China now suggest this is possible. Even likely, as liquidity is under attack.

ZeroHedge reports, “On Friday, shares of China’s banks extended their slide to a two-year low amid fears widespread mortgage non-payments would spark contagion within the banking sector (see “China On Verge Of Violent Debt Jubilee As “Disgruntled” Homebuyers Refuse To Pay Their Mortgages“) even after the local banking and insurance regulator said it will maintain continuity and stability of financing policies for the real estate sector.”

NDX futures rose to 11837.70 in the overnight market, a 50% retracement, before easing lower. The Cycles Model suggests potential weakness in equities today. The next Cyclical support is near 11000.00.

In today’s morning op-ex it is easy to see why the overnight rally to 11800.00, since a large cluster of expiring puts lies there. Options are sparse, but predominately short. QQQ (close 286.67) afternoon op-ex shows Max Pain at 288.00. Long gamma begins at 295.00, while short gamma starts at 280.00.

ZeroHedge observes, “Retail – which until now was a steadfast buyer of most dips (if with less and less vigor) – is starting to sell its equity holdings according to Bloomberg data, while speculators in futures markets are very short, in a potentially contrarian setup for the market, writes BBG’s Simon White.

While US equity sentiment based on retail investors has been bombed out all year at levels usually associated with market bottoms, the market has continued to remain weak and volatile. However, as White notes, the poor sentiment of retail investors masked what they were actually doing, as their equity allocations continued to remain high.

This is now changing, with average equity allocations finally gathering pace to the downside.”

SPX futures rallied weakly in the overnight session to 3808.50, but have eased beneath 3800.00. SPX closed above Cycle Bottom support at 3759.52 and must decline beneath it to lose all nearby technical supports. The weekly Cycle bottom support is at 3058.70. The Cycles Model suggests a possible bottom during the week of August 8, making a 30-day decline. However, other indicators suggest an extension of this decline to the week of August 15, for a 37-day decline.

This morning’s monthly op-ex shows Max Pain at 3795.00. But they don’t go positive until 3875.00. Puts dominate beneath 3750.00. SPY closing options (377.91) show Max Pain at 382.00, as retail investors become more bearish. Short gamma begins at 376.00 and intensifies at 375.00.

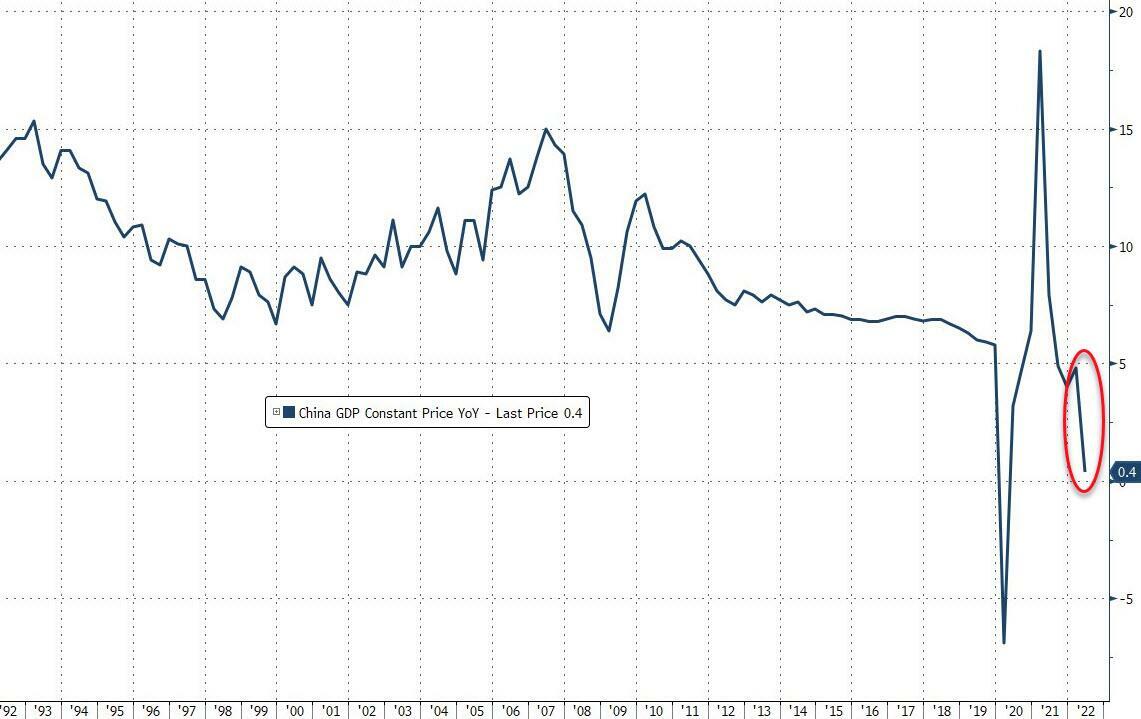

ZeroHedge reports, “US futures and European stocks advanced, shaking off data that showed China’s economy expanded slowest pace since the initial 2020 Wuhan outbreak amid pervasive lockdowns…

… while the dollar’s record surge stalled at the end of a week in which markets have been whipsawed by shifting expectations for monetary tightening by the Federal Reserve and worries over global economic growth.”

TNX remains beneath the 50-day Moving Average at 30.06 as it seeks direction on its next move. The Cycles Model suggests a further bounce approaching the Cycle Top at 34.65 in the next week or so. The scare of a 100-point bump by the FOMC is still being considered. However, the Cycle Model calls for a dramatic decline to the mid-Cycle support at 22.16 as a possible next move.

ZeroHedge considers, “When BofA’s top Rates strategist, and former NY Fed analyst, Marc Cabana speaks, investors, the Fed – and even his former Fed co-worker and repo guru, Zoltan Pozsar – listen. And what Cabana has to say now is extremely important.

On Thursday morning, roughly around the time BofA’s chief equity strategist Ssavita Subramanian slashed her S&P year-end price target by a whopping 25% from 4,500 to 3,600, Cabana’s rates team published a must read note (which is also available to pro subs in the usual place), in which he wrote that the bank’s rates team “is making substantial downward revisions to our rate forecasts following our US economics team’s new call for a mild 2022 recession and lower Fed funds rate path.”

What revisions?

Well, as of today, in addition to sharply lowering its stock targets, BofA is also slashing its 10y Treasury end ’22 forecast from 3.50% to 2.75% and end ’23 forecast from 3.25% to 2.50%. The cuts come as BofA’s economics team yesterday also slashed its forecast to reflect a US recession in 2022 and materially lowered the Fed funds rate path with the terminal Fed funds rate lowered from 4.00-4.25% to 3.25-3.50%, as the BofA economics team now expects 100bp of Fed rate cuts between Sep ’23 and Jun ’24.”

USD futures are lower this morning, signalling short-term weakness. The Cycles Model suggests a pullback to the trendline at 107.00 before a final probe to the top of this Cycle, due during the week of August 8. The “standard” target for the final probe may be 111.00, but it may extend higher.