2:05 pm

SPX may be completing the final Wave of Minute Wave [c] near 3900.00, which is round number resistance. Another resistance nearby is the 100-day Moving Average at 3910.00. The current Cycle has taken 51.6 days from the August 16 high and may have only 8.6 days to the low. Since Wave [3] cannot be the smallest Wave, it would follow that the minimum target may be near 3100.00. The Cup with Handle target is an average. The bottom of Wave [3] may not be achieved until mid-December. The 50-day Moving Average (sell signal) is at 3855.00.

ZeroHedge remarks, “This morning’s melt-up in stocks appears to be more of the same panic-hedge unwind, vol-driven buying-panic as hopes/hints of a “pause” or “pivot” or “step-down” remain the over-arching narrative as rate-trajectory expectations drift dovishly (lower terminal rate and faster subsequent rate-cuts)…”

8:00 am

Good Morning!

NDX futures declined to 11021.70 in the overnight session, crossing beneath the Lip of the Cup with Handle formation near or at 11100.00 before a bounce. The mega-cap technology companies lead the way.

In today’s op-ex, Maximum Pain for options investors is at 11275, while short gamma is at 11250.00, leaving NDX deep in negative territory. Today’s options are light, but may change as hedge funds are buying same-day options. QQQ (close: 272.87) shows Max Pain at 273.00. This is a tightly wound op-ex, since long gamma begins at 274.00 and short gamma begins at 272.00. There are over 150,000 put contracts between 272.00 and 265.00 this morning.

ZeroHedge observes, “As goes mega-cap tech, as goes the US economy

These large mega cap companies aren’t just secular growth stories they are so big that they are the US economy. The US economy is slowing as evidenced by PMIs, regional survey, Conference Board and housing data. And, as evidenced by the chart below, they were probably trading at too big valuation premium going into this. But maybe it does not matter that much from here. Up until this point the dominant factor influencing the price of equities has been rates…rates higher = multiples lower. If we get a reversal in rates (and that’s a big IF of course) that will probably trump even trembles in tech earnings….”

SPX futures made an overnight low of 3767.30 as it declines toward the next support at 3749.48. The Cycles Model suggests a possible event-driven panic starting on Sunday.

Today’s op-ex shows Maximum Pain for options investors at 3805.00. Long gamma begins at 3825.00 wile short gamma intensifies at 3775.00. The shorts are getting back their nerve.

ZeroHedge reports, “With the core of tech earnings season now behind us, FAAMG goes 0 for 5 on earnings as lackluster earnings from the group this week dampened sentiment and underscored the impact of the Fed’s tightening regime. While macro data didn’t help the cause – the GDP report showed the US economy rebounded after two quarterly contractions (all driven by net exports)and briefly assuaged concerns of an imminent recession, consumer spending remains under pressure because of persistent inflation – after the bell, AMZN out with an extremely disappointing miss which sent the stock down as much as 21%, followed by AAPL with a low quality beat driven by As such, Goldman’s Michael Nocerino writes that this morning is going to be harder to compartmentalize these prints (like we have with MSFT, GOOG, META) given AMZN and AAPL make up 10% weighting of the S&P.”

VIX futures made a nominal new low at 26.92 before a bounce began. This has stretched the current Master Cycle to 277 days and may have completed an irregular Wave 2, as well. This irregular formation goes hand-in-hand with the Broadening wedge formation in the SPX and NDX. The probable inference is that some big player has poured liquidity into the market to prevent a melt-down.

RealInvestmentAdvice remarks, “The Fed’s next crisis is already brewing. Unlike 2008, where “subprime mortgages” froze counter-party trading in the credit markets as Lehman Brothers failed, in 2022, it might just be the $27 Trillion Treasury market.

When historians review 2022, many will remember it as a year when nothing worked. Such is far different than what people thought would be the case.

Throughout the year, surging interest rates, the Russian invasion of Ukraine, soaring energy costs, inflation running at the highest levels in 40 years, and the extraction of liquidity from stocks and bonds whipsawed markets violently. Since 1980, bonds have been the defacto hedge against risk. However, in 2022, bonds have suffered the worst drawdown in over 100 years, with a 60/40 stock and bond portfolio returning a horrifying -34.4%”

Crude Oil WTI futures declined to 88.43 this morning, suggesting a Master Cycle high may have been made yesterday, on day 255 of its Master Cycle. A slip beneath the 50-day Moving Average at 86.65 may produce a sell signal, with a potential decline to mid-December.

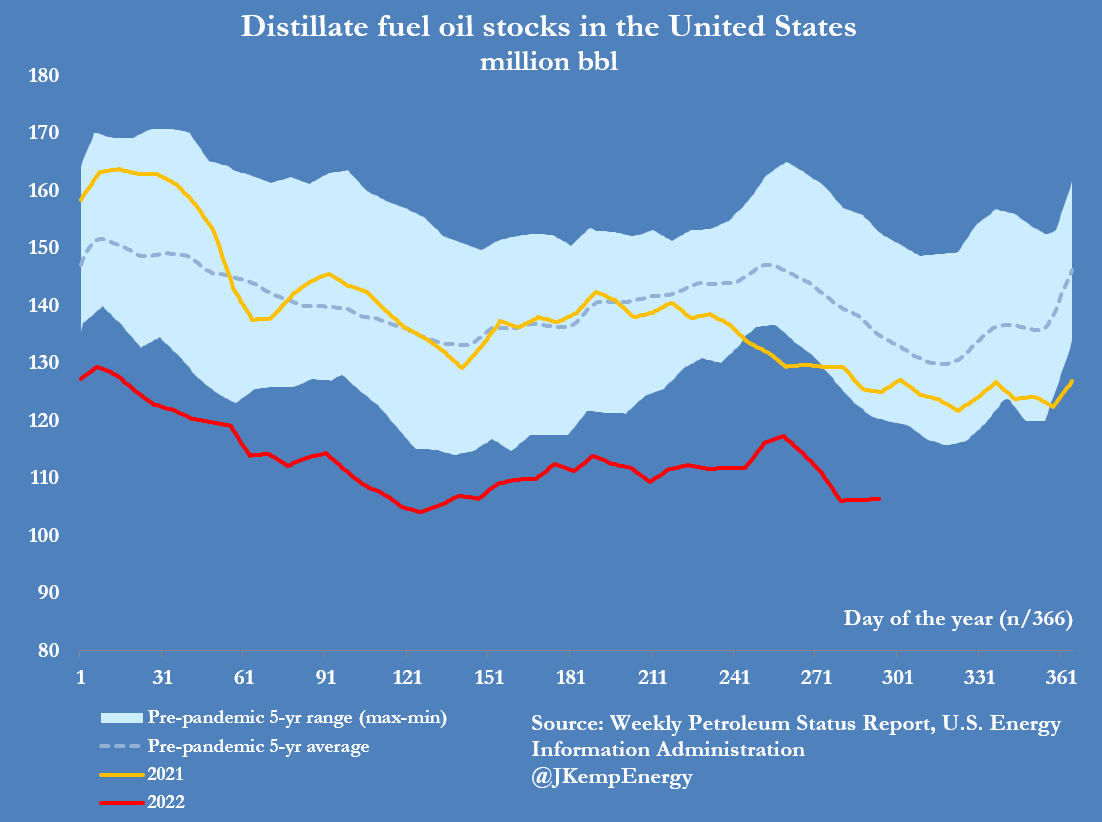

ZeroHedge reports, “U.S. diesel supplies are becoming critically low with shortages and price spikes likely to occur in the next six months unless and until the economy and fuel consumption slow.

Stocks of diesel and other distillate fuel oils were just 106 million barrels on Oct. 21, the lowest for the time of year since the U.S. Energy Information Administration (EIA) started collecting weekly data in 1982.”

ZeroHedge observes, “The worse the tech wreck, the more the fuel – so to speak – for energy gains, and following what has been the worst quarter for megacap tech names, most of which have tumbled double digits following dismal earnings, it is hardly a surprise that the two largest US energy majors just had blowout quarters, with Exxon posting its strongest quarterly result in the company’s 152-year history including its highest ever net income, while #2 Chevron reported its second-largest profit; the two companies amassed more than $30 billion in combined net income as Democrats blast Big Oil for raking in massive profits but since a red avalanche is coming to Congress in less than two weeks, we doubt anyone cares what Democrats think.”