11:23 am

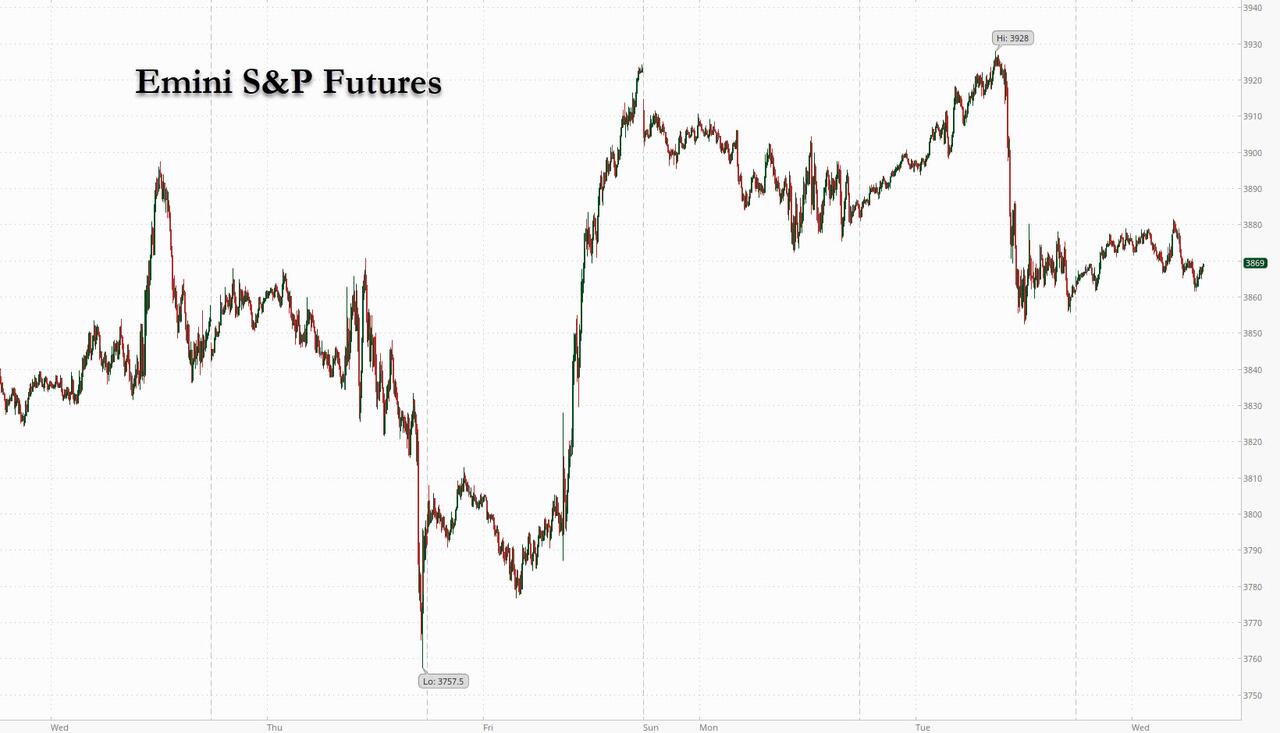

SPX has been challenging the 50-day Moving Average at 3838.27 this morning. Beneath that is a sell signal. However, as long as it straddles the line, there is a chance of a quick move to the 2-hour Cycle Top at 3947.68 at the Fed announcement, a 1.7% move higher. Subsequently, the decline is due to resume with targeting beneath 3000.00, at a minimum. As a reference, the upper Cup with Handle formation came within 10 points of its intended target at 3491.58. The two lower formations are in not-so-surprising agreement. We may see Wave (C) of Wave [3] complete by mid-December. Next week the Cycles Model shows a triple dose of volatility on November 8, 9 and 10.

ZeroHedge remarks, “With a looming sense of deja vu all over again, US equity prices have decoupled ‘hopefully’ from monetary policy expectations in recent weeks as the ‘pause/step-down/pivot’ narrative combined with extreme positioning to prompt yet another squeeze higher…

Source: Bloomberg

This in turn prompted a significant easing in financial conditions (easiest since mid-September), despite terminal rate expectations hitting cycle highs above 5%…

This, as Nomura’s Charlie McElligott details below, is a major problem for The Fed… again.”

9:39 am

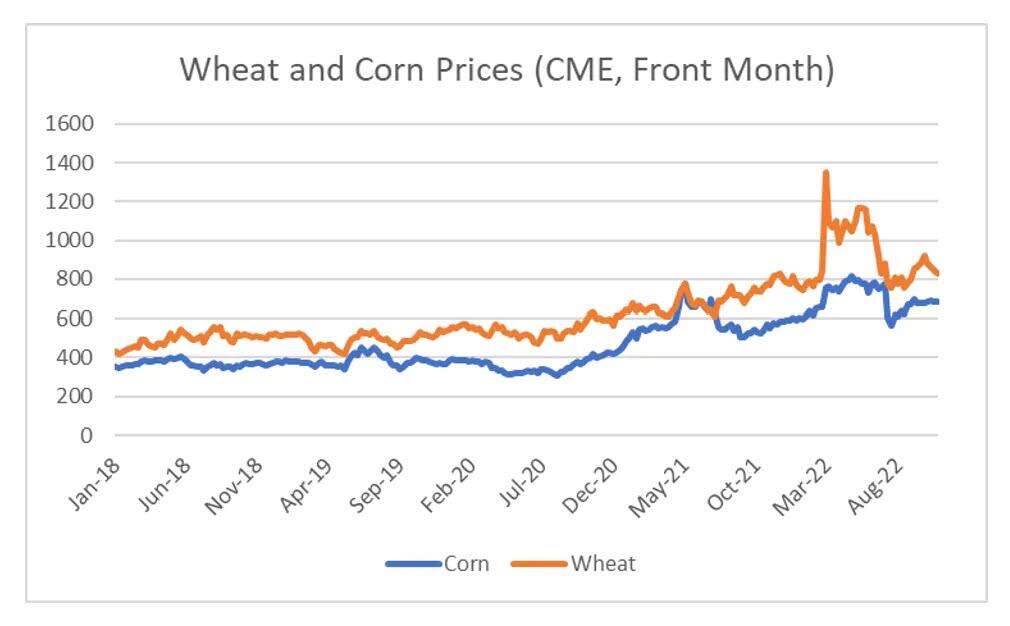

The Agriculture Index has pulled back from the 50-day Moving average at 475.95 after having made a buy signal. Once a signal such as this has been made, buying on the pullback follows. While the new Master Cycle is short (3-4 weeks), the Cycles Model suggests trending strength may prevail, suggesting a breakout is possible. Note that all reporting is done with accurate hindsight.

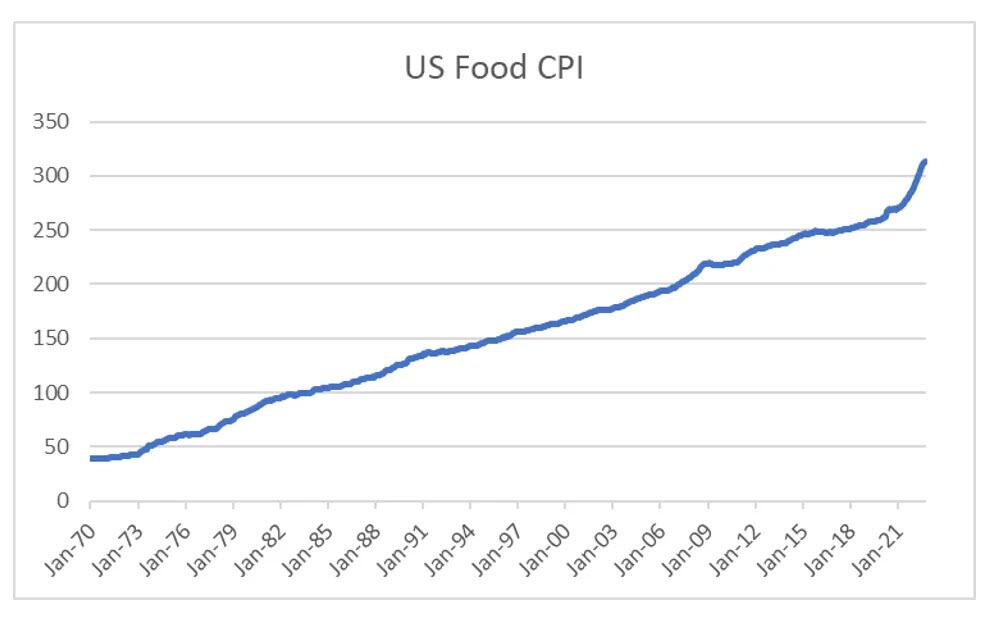

ZeroHedge observes, “Food inflation has continued to surprise to the upside in the US.

That food inflation has not calmed down in recent months is somewhat surprising as we have seen weakness in commodity food prices in recent months.”

However, new information suggests a rough patch ahead. As Russian grain shipments resume, the bird flu strikes Iowa poultry farms with the largest ever bird flu outbreak in the UK.

7:56 am

Good Morning!

SPX futures rose to an overnight high of 3972.20, then has eased down. It is likely to maintain a flat composure until the Fed announcement at 2:00 today. Today is day 251 of the Master Cycle. Should a new high be made today, it qualifies as the end of the current Cycle.

Today’s op-ex shows Maximum Pain at 3855.00. Long gamma begins at 3875, while short gamma may start at 3830.00. Puts are being re-populated after having been thinned out last week.

ZeroHedge reports, “US equity futures were unchanged after two days of declines in underlying gauges as investors brace for today’s 2pm Fed interest-rate decision along with its monetary policy outlook (although a potentially more surprising treasury buyback announcement could come as soon as 830am when the Treasury publishes its quarterly refunding announcement). Contracts on the S&P 500 were little unchanged, while Nasdaq 100 futures advanced 0.2% as of 7:30 a.m. in New York. Stocks have stabilized after a drop in the S&P 500 on Tuesday that was triggered by a surprise surge in job openings. European stocks erased earlier gains while US-listed Chinese stocks rallied in premarket trading and the Hang Seng Index rose in a session cut short by a storm warning as growing speculation over China’s reopening spurred another rally in Asia. The US dollar dropped for the second day as the yen strengthened in a sign traders anticipate a muted impact of Fed tightening on the currency; 10Y yields traded unchanged around 4.04%.”

VIX futures rose to a morning high of 26.27, beneath the mid-Cycle resistance at 26.66. Today is day 282 of a very stretched Master Cycle, should it go lower. However, I am comfortable with calling yesterday’s low “the bottom.” Most analysts do to consider the VIX a “buy,” expecting it to go lower. However, the VIX Cycles Model suggests a double dose of fear may strike the markets over the weekend.

Today’s op-ex shows Max Pain at 27.00, with short gamma at 26.00 and long gamma at 28.00. Heavily populated strikes are at 35.00 and 40.00.

ZeroHedge comments, “Bit of VIXubernce going into Fed

The gap between SPX and VIX (inv) is widening further. VIX has come a long way since the most recent “panic” highs, but as we stated earlier today, it is not cheap enough to buy, nor expensive enough to short.”

TNX is lower this morning, being unable to cross above the Cycle Top resistance at 41.45. The Cycles Model suggests a continued decline over the next two weeks as it completed its correction. It may be due to cross beneath Intermediate-term support at 38.83 and challenge the 50-day Moving Average at 36.53 during that time.

ZeroHedge comments, “Not more than a year ago it was generally thought impossible among mainstream economists and retail investors that the Federal Reserve would commit to raising interest rates and ending stimulus. After 14 years of predictable QE and near zero rates, it’s not surprising that they would refuse to acknowledge the possibility that the Fed would abandon them. Well, as with the seasons, all things must change.

At first they refused to admit that inflation was a problem, now mainstream outlets are openly discussing the idea that the Fed will have to “blow up the economy” in order to stop rising prices, with another 75 bps rate hike expected this week. As CNN noted recently in an article titled The Fed May Have To Blow Up The Economy To Get Inflation under Control:

“It’s unclear what all this tightening will do to the economy. The housing market is already starting to show some signs of strain. Bond yields have spiked due to the Fed. And mortgage rates, which tend to move in tandem with the benchmark 10-year Treasury, have skyrocketed this year as a result.”

In the meantime, the Treasury has deferred its decision about buybacks. Zerohedge remarks, “Yesterday we said that “with all the focus on the Fed tomorrow, it will be delightful(ly ironic) if the Treasury steals the show with a TSY buyback announcement during the 8:30am refunding announcement.”

Of course, as discussed extensively, a Treasury buyback – something that has not been done in earnest since the early 2000s – would be the functional equivalent of a QE/operation twist hybrid, only one conducted not by the Treasury, and thus any affirmative announcement today would have had an even bigger impact on markets than anything Powell would say at 2pm.”

USD futures may be testing the 50-day Moving Average at 110.80 for support before moving higher. The Cycles Model shows the USD strengthening this week in preparation for a possible breakout. The new Master Cycle may last until mid-December.

Crude Oil futures are moving higher and threatening to break through the upper trendline of the Triangle formation. This type of breakout is common and unfortunately sends a false buy signal to the unwary. Today is day 261 of the current Master Cycle, making a reversal imminent. The Cycles Model calls for a decline into the second week of December.

ZeroHedge observes, “Oil prices rallied today for the first time in 3 days after strong JOLTS data and rising geopolitical risks outweighed anxiety overFed-induced demand drags. Additionally renewed Zero-COVID lockdown easing rumors in China helped sentiment.

“Risks to energy supplies remain elevated after reports that Iran was planning an attack on targets that include Saudi Arabia and Northern Iraq,” said Edward Moya, senior market analyst at OANDA.

Meanwhile, “global economic outlook remains very fragile to a swathe of risks, and that should keep crude demand forecasts vulnerable to getting slashed, but for now energy traders remain fixated on how tight the market remains.”

For now, all eyes are on the API for any signs of distillates stocks rebuilding….”

Gold futures are consolidating within yesterday’s trading range. Gold is on a sell signal and may continue its decline through the 4th week of November before a a reprieve in the downtrend.