1:10 pm

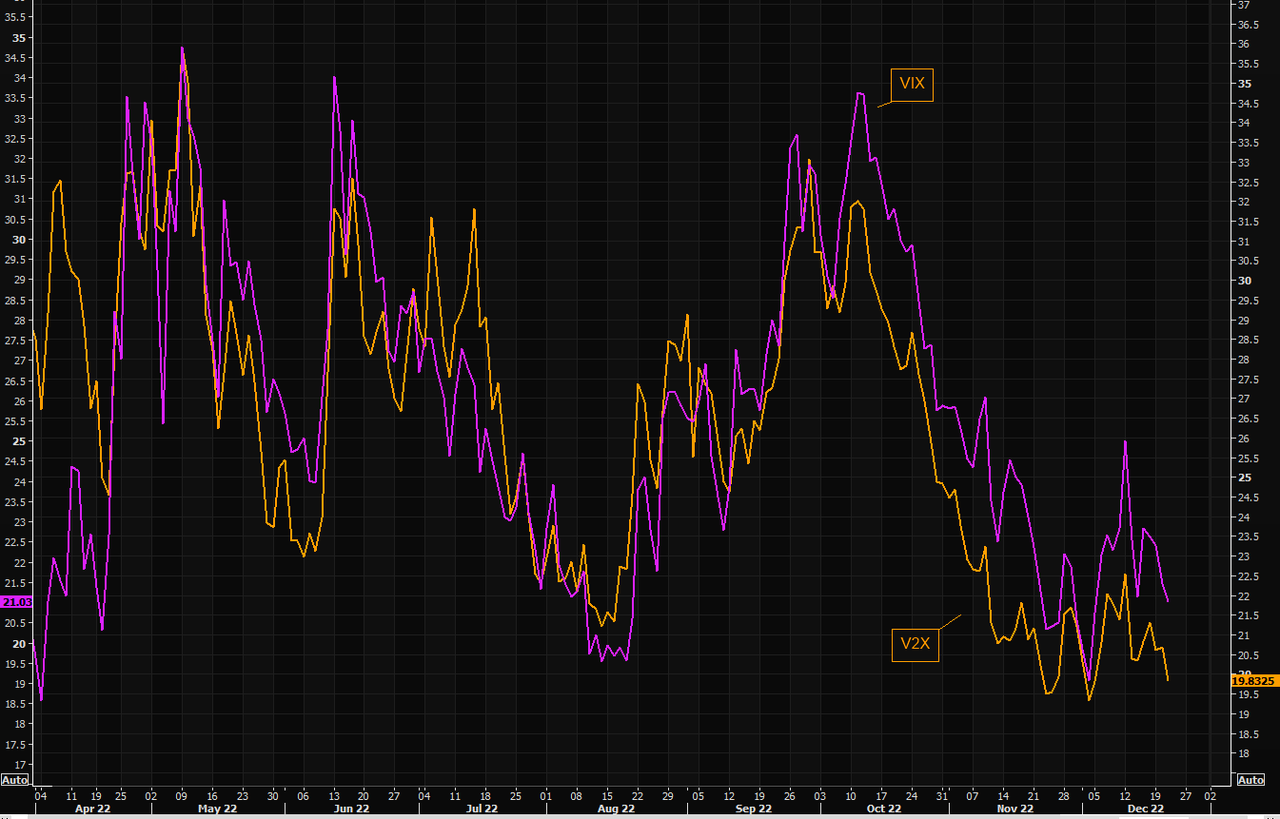

VIX has responded by rising toward the 50-day Moving Average at 24.50. The rise above the trendline launched an aggressive buy signal. The 50-day confirms it.

12:58 pm

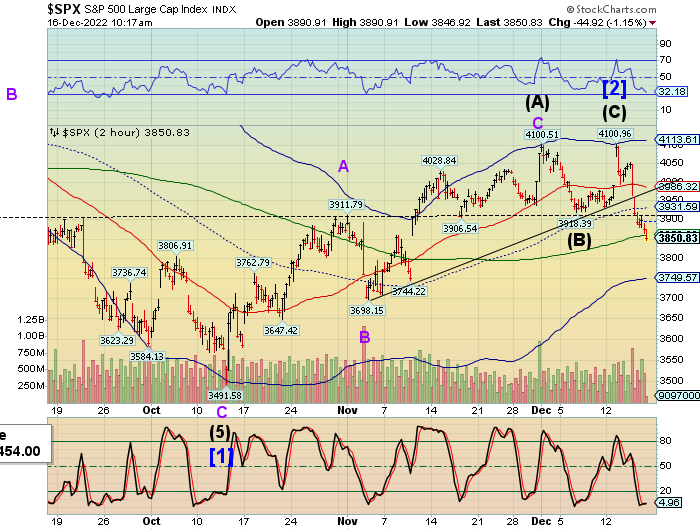

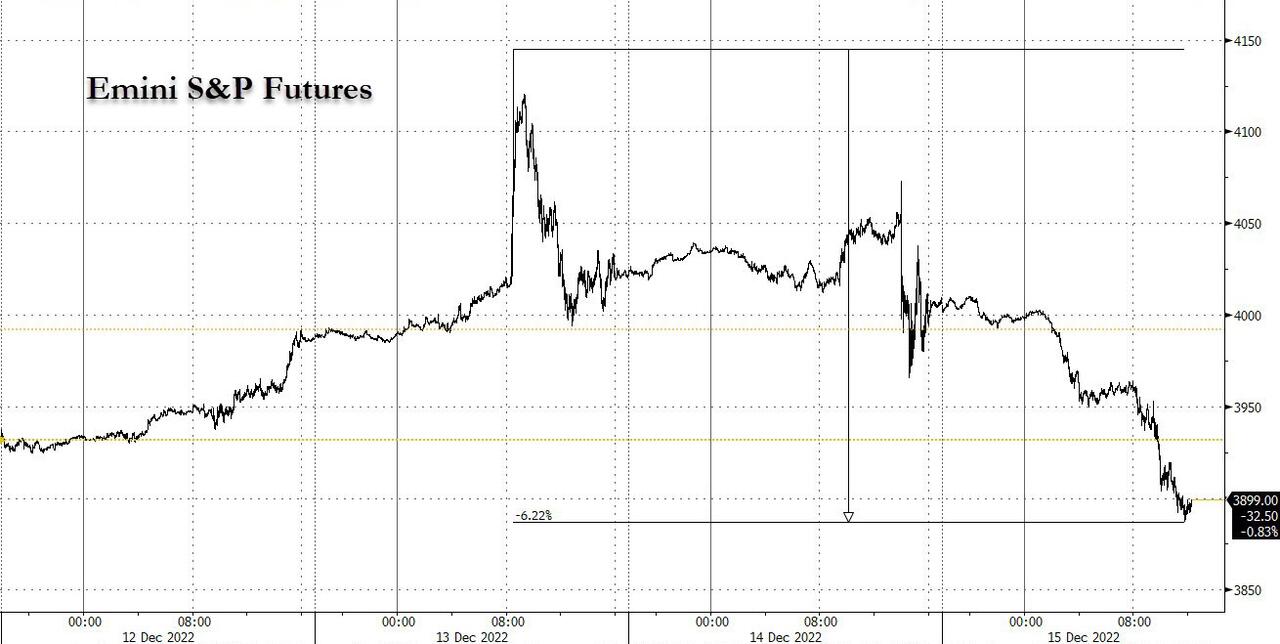

SPX has dropped well beneath its previous low at 3795.00, confirming the bearish trend. The next possible support is at 3740.97 where a bounce may occur. There is still the possibility of a bounce, but SPX is deep in short gamma beneath 3800.00. Sadly, the runaway train may come at Christmas.

ZeroHedge observes, “Update (1245ET): Shit’s getting real in equity-land as this morning’s selling pressure has turned into a blood-soaked sea of red with TSLA leading the plunge, down 11%…

The S&P has erased all of the week’s gains…”

9:49 am

The Ag Index is challenging the 50-day Moving Average at 463.60 today. This may confirm a buy signal that may extend to the end of the year. The target may be mid-Cycle resistance at 495.09 or the Lip of the Cup with Handle at 500.00. The Ag Index may become very active next year as it emerges out of its six-month trading range.

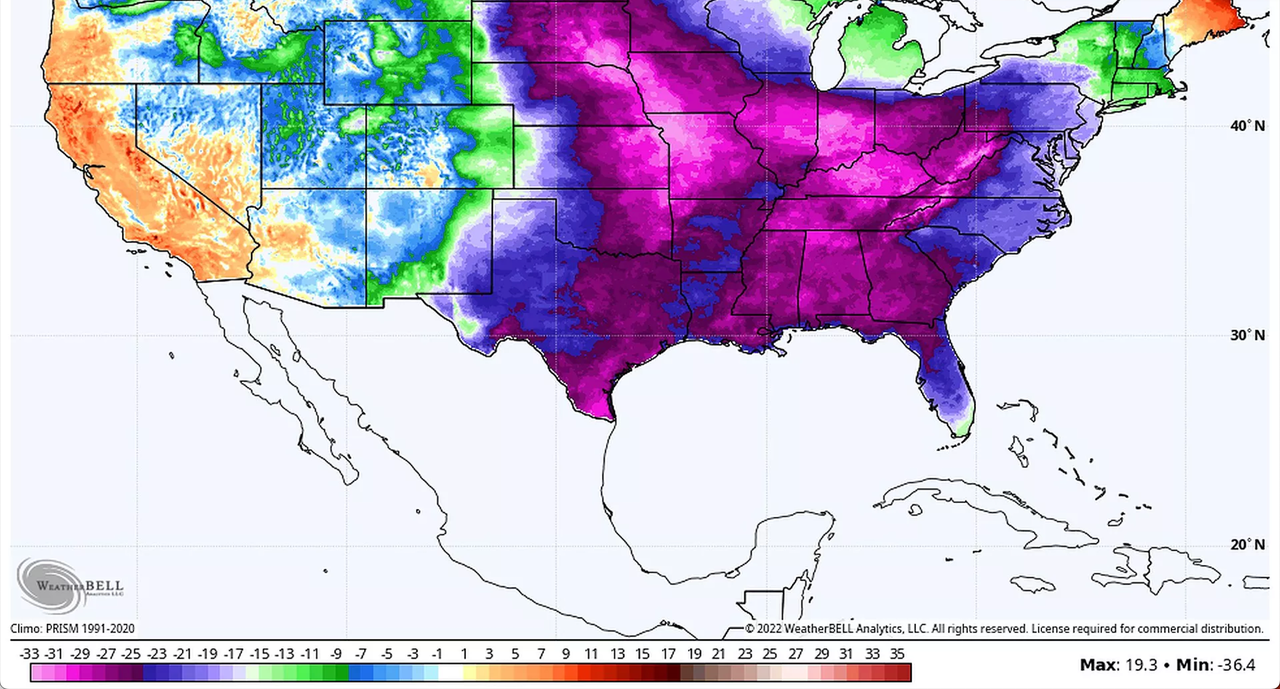

ZeroHedge warns OJ lovers, “Widespread cold air is already pouring into the Plains and Deep South. This cold will last through Christmas weekend into early next week and could threaten citrus groves across Florida.

America’s top orange juice maker is already battling a record decline in crop this season because of citrus greening, a devastating crop disease, and damage sustained by Hurricane Ian and Tropical Storm Nicole earlier this year. Now a cold blast could damage crops even more. ”

ZeroHedge observes, “Demand for US cropland remains robust despite skyrocketing borrowing costs and mounting macroeconomic headwinds. Private sales of cropland across the Midwest, the nation’s breadbasket, have jumped among the ultra-wealthy.

When it comes to investment choices, billionaires and centimillionaires make smart decisions (well, at least some) to preserve wealth. One of the best ways to do so is own tangible assets: land.

Investment in cropland has become popular among financial elites. The list of billionaires, including Bill Gates, Jeff Bezos, and Warren Buffet, has been growing amid a commodity boom across the US farm belt: ”

8:20 am

Good Morning!

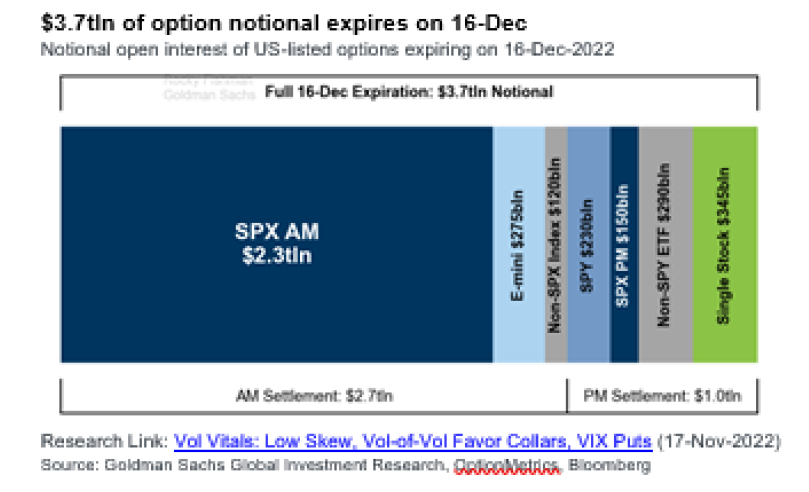

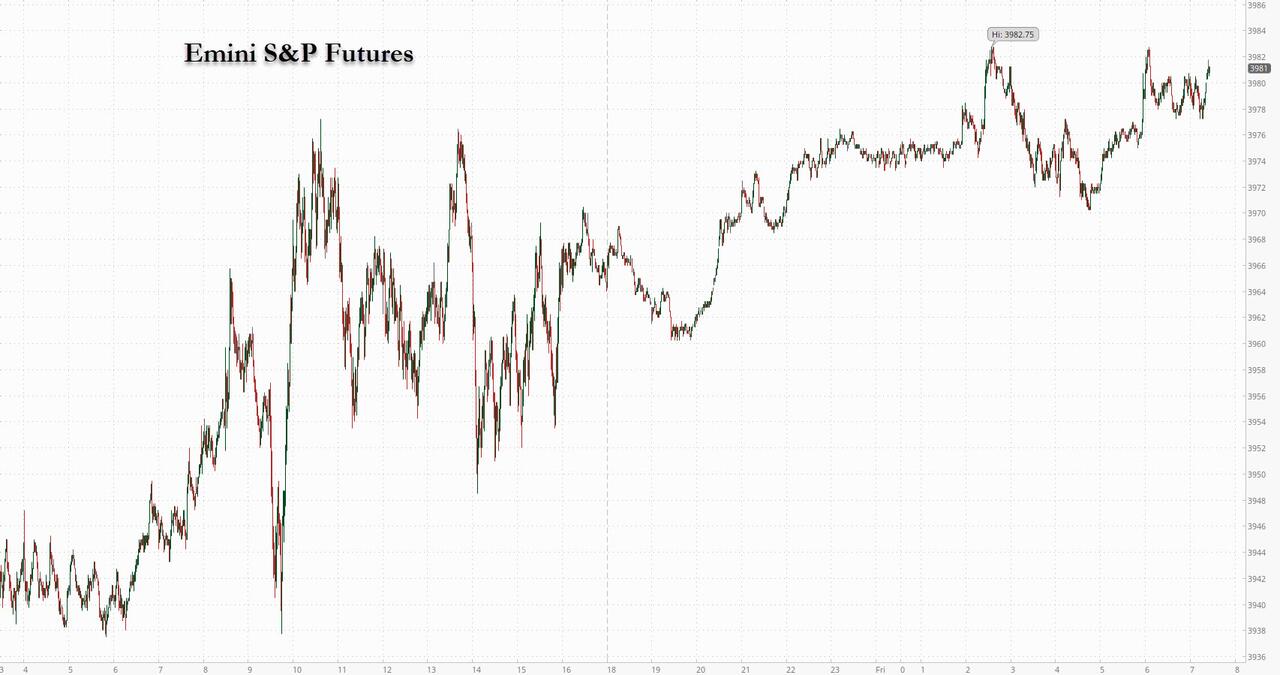

SPX futures are challenging the 50-day Moving Average at 3866.70. The Cycles Model suggests today may be a consolidation day. Trending strength may return on Friday. Next week appears to be relatively peaceful, barring any potential earth-shattering news.

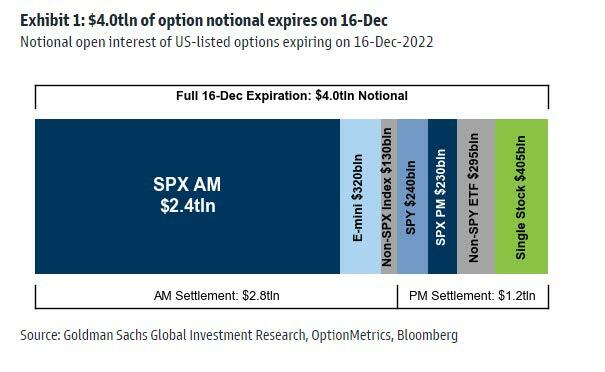

This Morning’s op-ex shows Maximum pain for options investors at 3890.00. Long gamma starts at 3900.00, while sort gamma begins at 3875.00. SPX may stay trapped in the neutral zone for the day. Tomorrow’s op-ex shows Max Pain at 3955.00 with long and short gamma at lower levels as well.

ZeroHedge reports, “US stock futures reversed gains from earlier in the session and struggled to hold the momentum that propelled the S&P 500 to its best daily gain in three weeks, as investors assessed whether the world’s biggest economy can skirt worst-case recession scenarios. Contracts on the Nasdaq 100 and the S&P 500 were both 0.3% lower at 7:30 am ET, erasing earlier gains of 0.3%. Both indexes had bounced on Wednesday following better-than-expected earnings from FedEx and Nike as well as a pickup in consumer confidence, but the mood was dampened by memory chipmaker Micron, whose gloomy outlook knocked its shares in US premarket trading and weighed on other chip firms. European semiconductor shares also fell, erasing earlier gains on the Stoxx 600 gauge, though it remains set to break a two-week losing spell. The dollar index was flat while the US 10-year yield dropped to about 3.64%.”

VIX futures consolidated in the lower part of yesterday’s trading range with a high of 20.40. The threat of a new low lingers until the end of the week. Today is day 262, nearly three weeks from the low on the chart. Trending strength is due to re-appear at the new year.

As we move into next week’s op-ex, Max Pain is at 22.00. Short gamma is at 18.00, while long gamma begins at 25.00. This week’s downward pressure on the VIX has expired.

TNX appears to be consolidating just beneath Intermediate-term resistance at 37.11. Above that is the 50-day Moving Average at 38.30 and a confirmed buy signal. Today shows trending strength re-appearing and gaining strength over the next two weeks. This may be a surprise to investors after three months of steady-to-declining rates.

ZeroHedge reports, “After several disappointing coupon auctions to start the month of December many of which tailed and pushed yields wider, moments ago the Treasury placed the final 20Y auction for 2022 when it sold $12 billion in 19-year 11-month (Cusip TM0) reopening. The auction was a blowout: the high yield of 3.935% was the first auction to price below 4.00% since September, it was well below November’s 4.101% and and also stopped through the 3.948% When Issued by 1.3bps, which while less than half of last month’s 2.9bps stop through was still the 10th stop through in the past 13 auctions.”

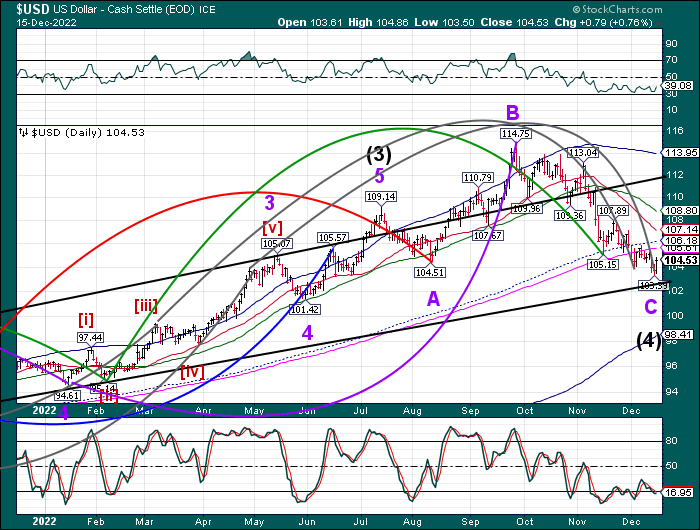

USD futures rose to 104.06, not -quite-a-breakout, and remained in the upper part of yesterday’s trading range. Trending strength is due to re-appear as it returns to its uptrend through the second week of January. The double bounce off the trendline offers an aggressive buy signal to be confirmed once it rises above the resistance levels.

Gold futures linger near their high with a chance of making a nominal new high in the next week. Be aware of a potential reversal after the new year with a possible new low at the end of January.

Crude oil futures are higher, possibly aimed at the 50-day Moving Average at 82.50 in the next few days. The Cycles Model warns of a potential reversal next week.