1:52 pm

BKX gave up all of its CPI spike gain and is back beneath the 50-day Moving Average at 102.74. It remains on a sell signal, although an antacid may have helped the jumpy stomach this morning. It’s downward course may be set through the year end. We may see an “everything down” market for a while as liquidity is drained from the market.

1:47 pm

The CPI spike also brought TNX below the trendline for a brief test. However, it stopped before making a new low and is back above the trendline. The Cycles Model suggests a rally may resume until the first week of January.

ZeroHedge reports, “One day after the ugliest 10Y auction since 2016 (which however saw a blowout in yields ahead of the 1pm deadline) moments ago the Treasury sold the last coupon bond of the week ahead of tomorrow’s FOMC meeting when it found buyers for $18BN in 30Y paper (technically 29-Year 11-month reopening of Cusip TL2). In a nutshell, the auction was almost as ugly as the 10Y even though yields tumbled this morning after the far weaker than expected CPI print.

Pricing at a high yield of 3.513%, the auction tailed the 3.482% When Issued by 3.1bps, the biggest tail since December 2021.”

1:40 pm

VIX reversed its gains at the CPI spike, declining to the Triangle trendline at 21.45. It has since recovered and may be ready for further gains. Wednesday may show the breakout above the double resistance.

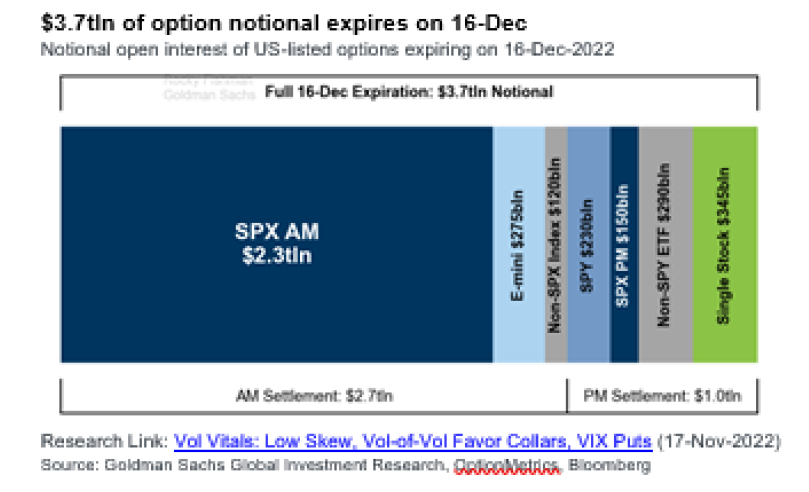

ZeroHedge remarks, “As we detailed over the weekend, this week’s options expiration is a doozy with a massive $3.7tln of option notional expires on 16-Dec…

12:45 pm

SPX made a surprise bulls-eye on day 259 of the Master Cycle with a (very) marginal new high, then giving up all of the CPI spike gains. Needless to say, I had been expecting a different outcome. Welcome to my world! Now let’s discuss what’s next. The Cycles Model calls for a very strong pivot in the first week of February. That also happens to be 12.9 months from the top on January 4. Thus, I was leaning toward a top at that point. Leading up to that point would have necessitated a low in December followed by a sideways-to-higher rise through January.

Today’s new high on the MC Pivot day suggests otherwise. Should SPX cross beneath the combined 100-day (3930.00) and Intermediate-term support at 3929.18, we may see a 7-week decline to the next MC pivot in Wave (1) of [3]. For now, we wait for the FOMC announcement tomorrow.

8:10 am

Good Morning!

SPX futures have tested the mid-Cycle resistance at 4013.79 and pulled back, waiting for the CPI report at 8:30 am. The 50% retracement value is 4009.45. As of yesterday’s close, the SPX barely exceeded the 38.2% retracement level at 3987.96.

8:30 am

SPX futures leaped to a new high prior to the CPI report, probing to 4133.80 before settling down beneath the prior cash high. A reminder that today is day 259 of the Master Cycle. More observations after the open.

ZeroHedge reports, “After a dismal start to December, US futures extended their gains to a second day ahead of today’s critical economic data: the final consumer prices print due of 2022 which in turn precedes tomorrow’s final for 2022 FOMC meeting where Powell is expected to slow the pace of hiking to 50bps. Contracts on the S&P 500 rose 0.6% higher by 7:45 a.m. ET while Nasdaq 100 futures gained 0.7%. The underlying benchmarks advanced on Monday in anticipation Tuesday’s inflation data and Wednesday’s Federal Reserve decision will establish a slower pace of interest-rate increases. The greenback halted a two-day rally, while Treasuries gained. Oil futures extended gains by another 0.5% after almost sliding below $70 on Monday on signs of further easing in China’s Covid rules. Oil traded higher by 0.5% on signs of further easing in China’s Covid rules.

Today’s op-ex show Max Pain at 3980.00. Long gamma starts at 3990.00-4000.00. Short gamma may begin at 3950.00, a hotly contested level.

ZeroHedge observes, “Nomura’s Charlie McElligott’s note this morning begins with a warning of sorts:

Fear of the dovish “right-tail” response to CPI is back… Bigly!

Expectations into today’s CPI print for a continuation of the “past peak inflation = past peak tightening = FCI EASING” theme are building, which is contributing now to this ongoing “bullish” tilt towards Upside optionality in US Treasuries / STIRS and Equities.”

VIX futures have risen to a morning high of 25.84, which may trigger a further buying response from the knowledgeable. The mid-Cycle and 50-day Moving Average are both at 25.94. A rally above that area may spark an abrupt change in outlook for the market.

NDX futures ramped up to 12191.80 as CPI came in under the consensus. It now appears that the current Master Cycle (day 259) may end at a new retracement high. The potential target may be the mid-Cycle resistance at 12351.33.

ZeroHedge observes, “The first of this week’s big event risks has arrived and while the world and his pet rabbit is focused on the number’s potential for ‘dovishness’, bear in mind that expectations are for a 0.3% MoM rise and 7.3% YoY rise (which while ‘slowing’ remains extremely high by any standards).

The banks’s CPI forecasts were all in sync:

- 7.2% – Barclays

- 7.2% – Credit Suisse

- 7.2% – Goldman Sachs

- 7.2% – Bloomberg Econ

- 7.2% – Citigroup

- 7.2% – Morgan Stanley

- 7.2% – Wells Fargo

- 7.3% – HSBC

- 7.3% – JP Morgan Chase

- 7.3% – UBS

- 7.3% – Bank of America

- 7.4% – SocGen

The headline CPI printed cooler than expected, rising just 0.1% MoM, with the YoY rise falling to +7.1% (below all the big banks’ expectations) – lowest since Dec 2021.”