3:25 pm

NDX has crossed back beneath the 50-day Moving Average at 11454.58. The final support may be the Lip of the Cup with Handle at 11000.00. There may be free-fall beneath it.

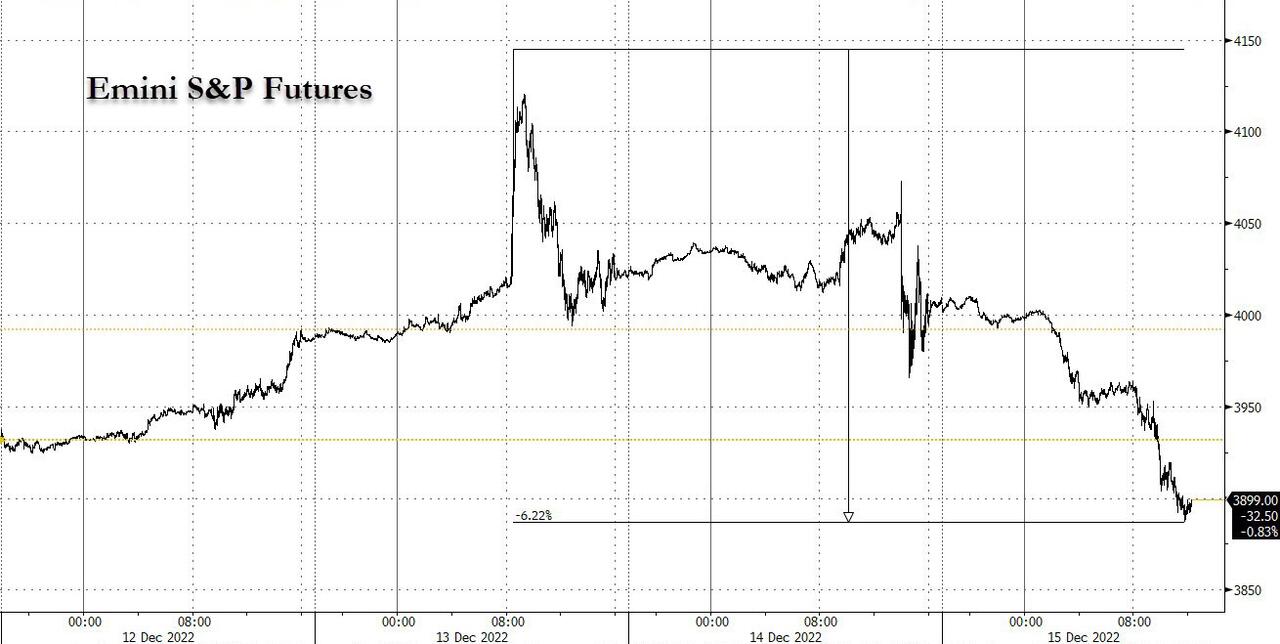

ZeroHedge writes, “Over the weekend, we predicted that with the market stubbornly rangebound, if the S&P was going to move “It will be this week as $3.7 trillion in options expires.” And sure enough, markets moved – a lot – with the S&P first spiking in kneejerk reaction to the weaker than expected CPI to briefly tag 4,145 before sharply sliding more than 6% in the opposite direction after the hawkish Fed and ECB, sent spoos tumbling below 3,900…”

11:28 am

SPX has now crossed beneath the trendline and round number support at 3900.00. It may bounce briefly to retest the trendline at 3910.00, but the trend is solidly down. Note that the month-long trading range has broken down. The next support beneath is the 50-day at 3857.00-3858.00.

9:50 am

SPX has crossed beneath its short-term trendline at 3965.00 , the mid-Cycle support at 3935.00 and the 100-day Moving Average at 3931.00, confirming its sell signal. The next level of support is the trendline at 3910.00. SPX is now declining into short gamma beneath 3950.00. A decline beneath 3900 may accelerate the decline due to additional layers of short gamma being activated.

7:45 am

Good Morning!

NDX futures declined to a morning low of 11556.10, possibly to test Intermediate-term support at 11532.80. Below that is the 50-day Moving Average at 11432.15 which defines the bottom of the trading range in December. A breakdown confirms the sell signal that flashed an aggressive sell beneath the 100-day Moving Average at 11935.25. The Lip of the Cup with Handle formation lies at 11050.00.

Today’s op-ex shows Maximum Pain for options investors at 11680.00. Calls dominate above 11700.00, while puts control the area beneath 11650.00. Gamma level are indeterminate in the NDX. QQQ (closing: 286.51) shows Max Pain at 284.00. Long gamma starts at 289.00, while short gamma may begin at 283.00. Today’s op-ex is sparse.

Friday’s op-ex is heavily populated with Max Pain at 286.00. Long gamma begins at 290.00, while short gamma may begin at 285.00 and accelerates at 280.00. Tomorrow’s op-ex could be a very stormy session.

In the meantime, ZeroHedge takes a nap, “Still looking for the trend

Chart of NASDAQ over the past month. Don’t chase trends that do not exist…

Source: Refinitiv

SPX – king of ranges

SPX remains stuck inside the relatively tight range that has held since that massive November inflation print. Note we are practically on the 200 day moving average. No excitement from us until this breaks out of the range.”

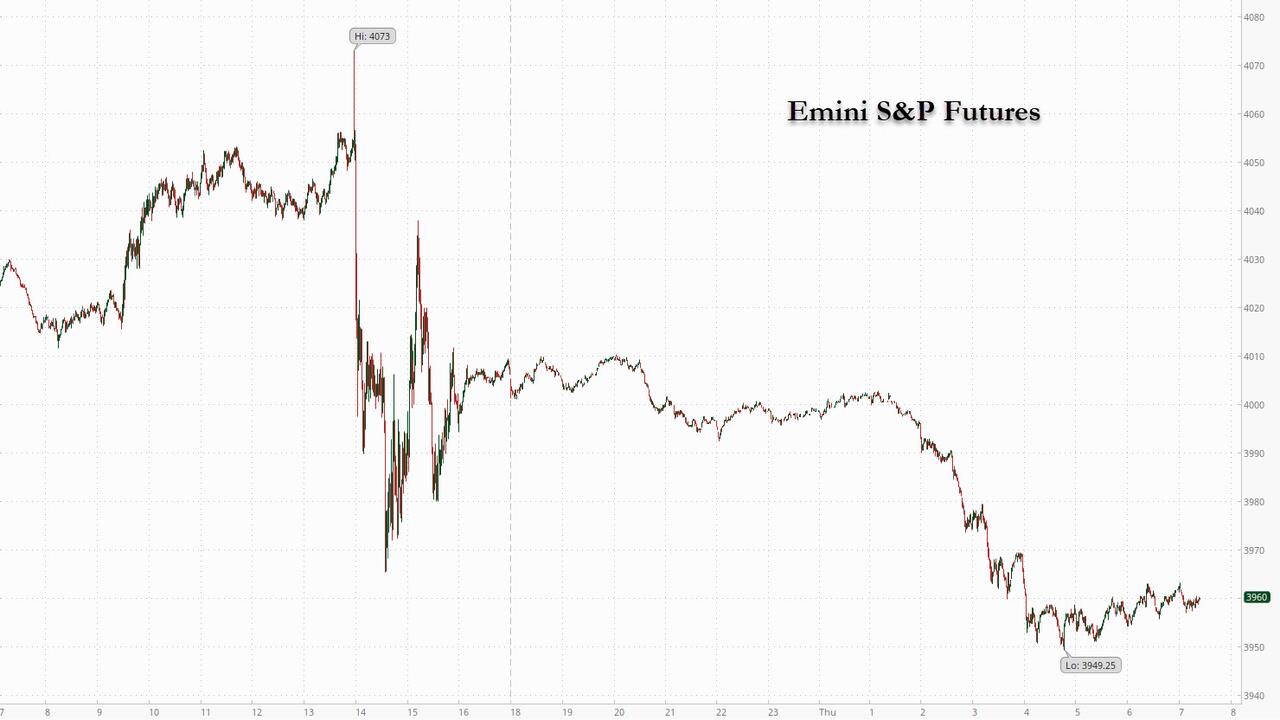

SPX futures declined to 3944.20, just above Intermediate-term support at 3934.51 and the 100-day Moving Average at 3930.00. SPX is on an aggressive sell signal beneath mid-Cycle resistance at 4008.61. Crossing the next supports confirms the sell signal. Should those supports be crossed, SPX begins a 7-week decline to new lows. There is a 2-year Cup with Handle formation that suggests a target of 2250.00, possibly in the next six months. Shorter term, SPX may decline beneath 3000.00. The gentle decline of Wave [1] may turn into a waterfall in Wave [3].

Today’s op-ex shows Max Pain at 3995.00. Long gamma begins at 4000.00, while short gamma starts at 3950.00. Today’s op-ex is lightly populated.

Friday’s op-ex is another story. Max Pain is at 4010.00. The 4000.00 strike being hotly contested with over 150,000 put and call contracts. Each 50-point interval is populated with at least 50,000 contracts down to 3200.00. This train may turn into a runaway with no brakes.

ZeroHedge reports, “S futures extended declines on Thursday following hawkish signs from the Federal Reserve that it would keep rates higher for longer even as it pushed the US economy into a stagflationary recession. Contracts on the technology heavy Nasdaq 100 were down 1.3% by 7:45 a.m. in New York, while S&P 500 futures fell 0.9% after dropping as much as 1.1% earlier. Both underlying indexes dropped yesterday after Fed Chair Jerome Powell delivered a 50-basis-point rate hike, as expected, and said the central bank had more work to do – and will push the terminal rate to 5.1% or higher – in taming inflation despite ebbing price pressures and mounting fears of job losses.”

VIX futures rose to 21.94 this morning, still sleepy from the beat-down it received on FOMC day. VIX monthly op-ex is three days later than the NYSE op-ex. In conjunction with that, the VIX Master Cycle may be due for a peak by that date. The VIX Cycles may be out-of-sync with the SPX Cycles due to the VIX monthly op-ex occurring the week after the NYSE Monthly op-ex.

Next week’s op-ex shows Max Pain at 24.00. Short gamma begins at 22.00 and goes to 17.00. Long gamma begins at 25.00 and rises to 70 with 157,181 contracts at that strike. The numbers smack of institutional involvement and have a high probability of being realized.

TNX is testing the lows again, despite the long-delayed Master Cycle bottom put in on December 7. This has the earmarks of a very large player buying long Treasuries before and since that time. The Cycles Model suggests this could blow up (higher) by mid-week, as trending strength returns. The new Master Cycle should last through the first week of January.

ZeroHedge remarks, “Thousands of tech workers laid off every single week as the Silicon Valley ponzi crumbles under the weight of the Fed’s rate hikes? Not according to the Department of Labor, which moments ago reported that in the latest week, initial claims unexpectedly tumbled by 20K to 211K from 231K, the lowest since September 23 and far below the consensus estimate of an increase to 233K; at the same time unadjusted claims dropped from 288K – the highest since January – to 248.9K.”

USD futures tested the trendline with a low of 103.10 this morning. This may be the low on day 254 of the new MC, only 7 days later. This highly unusual cluster of MC lows may be due to the unusual buying of Treasuries by a large institution. However both Treasury yields and USD are wound up for a very substantial rebound into January. This has the makings of a disastrous year-end for the markets.