2:36 pm

SPX has broken down beneath short-term support at 3995.59 and has bounced at the uptrend line at 3965.00. It is on a sell signal with additional confirmation beneath the trendline and the mid-Cycle support at 3929.63. Expect volatility to rise.

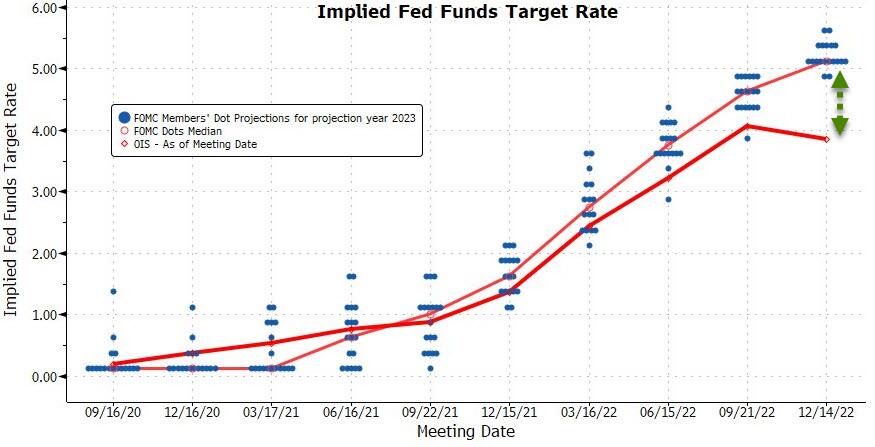

ZeroHedge remarks, “Tl;dr: Fed hiked rates by 50bps as expected but signaled, through its projections, that it will hike rates higher than the market expects and hold those rates higher for longer. Furthermore, the projections for economic growth, employment, and inflation all suggest The Fed expects a recession.

Fed rate expectations are notably more hawkish than the market’s…

With the market expecting rates to be lower than current levels by January 2024…

8:10 am

Good Morning!

SPX futures eased lower to 4010.90, near the mid-Cycle support at 4011.40, but beneath the 200-day Moving Average at 4033.69. Today is FOMC day and, given past practices, we may see a nominal new high this afternoon after the announcement and press conference. Today is day 260 of the Master Cycle, so a further probe higher may be acceptable. It may also set the stage for a reversal to new lows.

Today’s op-ex shows Maximum Pain for options investors at 4005.00. Long gamma begins at 4050.00, while short gamma starts at 3950.00. This week’s op-ex is sparsely populated, which may lend itself to wider swings. Friday’s op-ex, however, is loaded for bear beneath 4000.00 with 50,000 incremental contracts every 50 points down to 3400.00 and possibly lower.

ZeroHedge reports, “US equity futures were little changed ahead of the final Federal Reserve policy decision of 2022 as traders fretted whether cooler-than-expected inflation will justify smaller rate hikes. Contracts on the S&P 500 and Nasdaq 100 traded on either side of the unchanged line by 730am ET. The underlying benchmarks surged in early trading on Tuesday after the latest CPI data showed a US inflation posted the smallest monthly advance in more than a year, indicating the worst of inflation has likely passed; all gains were subsequently pared however with the S&P closing little changed (See “What Was Behind Today’s Drift Lower In Stocks“). Treasuries and bitcoin rallied, while the dollar slipped.”

VIX futures are clustered near yesterday’s close. They are poised for a new move higher, which may take VIX to the Head & Shoulders neckline. It appears to be common practice to goose the SPX and suppress the VIX immediately upon making the FOMC announcement. A revisit to the bottom trendline of the Triangle formation may be anticipated. Upward momentum (trending strength) may build through Monday.

Today’s op-ex is lightly populated with calls favored at 23.00 and higher. There are no discernible long or short gamma levels for today’s expiration. Next week’s op-ex shows Max Pain at 25.00 with short gamma at 22.00 and long gamma at 26.00.

Bloomberg points out, “While the S&P 500 was en route to a 1.4% gain Monday, the Cboe Volatility index — a gauge of cost on options tied to the stock benchmark also known as VIX — jumped more than 2 points to surpass 25. Not only do same-direction moves buck the historical pattern where the two normally move in opposite directions, their outsize jumps today mark the first time since 1997 when both climbed in sync as much as they did.”

TNX rose above its trendline at 35.00 this morning, signaling a potential positive trend may have emerged. Of course, this hinges on the outcome of the FOMC report. The Cycles Model implies a continued rally in rates through the end of the year.

ZeroHedge observes, “The Federal Reserve’s revised dot plot that will be unveiled Wednesday will acknowledge the need for policymakers to raise rates higher than previously anticipated in order to put the inflation genie back into the bottle.

The dot for next year is likely to show the median at 4.875% compared with the 4.625% estimated in September. A number even higher than that would spur an immediate selloff in Treasuries — especially at the front end — though slower-than-forecast inflation for November may stay the Fed’s hand from doing so.”

USD futures declined to a new low at 103.25 on day 259 of the Master Cycle. This may be the low, or nearly so, as both time and target may be met today. Should the reversal be made today, the Cycles Model projects the ris in the USD to mid-January. The prediction of the demise of the USD is early and overdone.

BKX, our liquidity proxy, is due for a day of strength, which goes along with the “goose” of the SPX upon the FOMC announcement. However, the balance of the month may be in decline as BKX makes the final crossing of the neckline of the Head & Shoulders formation.

RealInvestmentAdvice declares, “Often, boaters take the warning blow of a foghorn for granted and disregard it. However, all skippers seem to pay attention when they hear the scraping of their hull against a reef.

The yield curve is a financial foghorn of sorts. Currently, it is bellowing that something is drastically wrong. As evidenced by earnings growth estimates for 2023, financial skippers are going about their business as if a recession is unlikely.

Yield curve foghorns are often unheeded by investors as they blow well before danger is apparent. As such many investors are unprepared when problems arise.”