12:02 pm

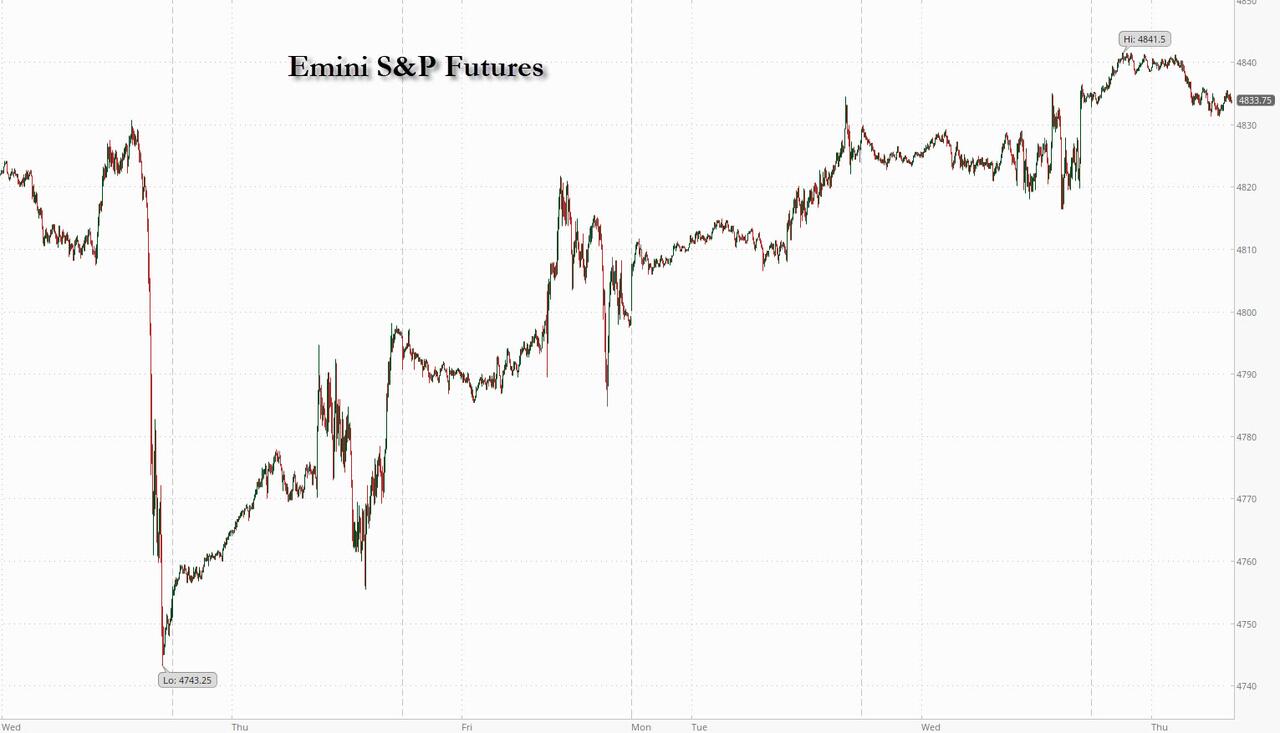

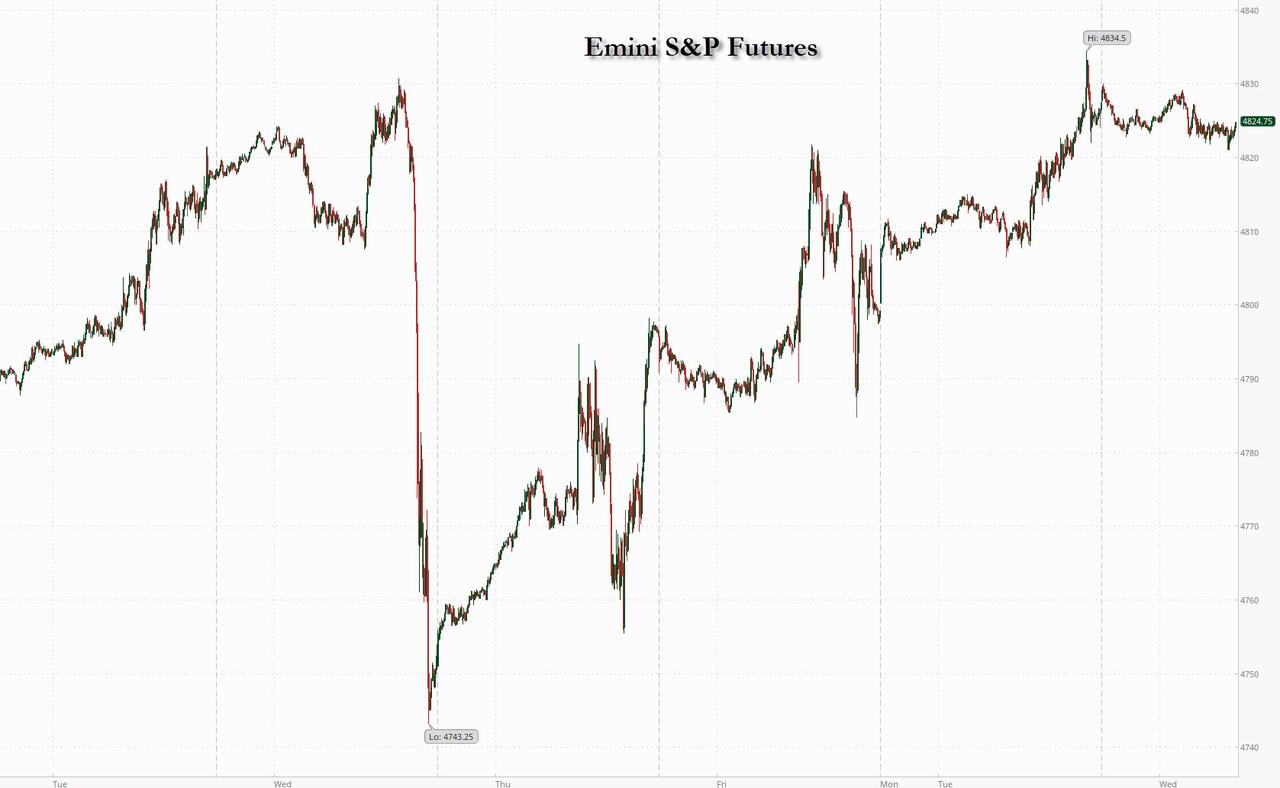

SPX has a potential of one more probe higher, but has possible structural limitations at 4781.00. Currently the 1987 trendline is near 4763.00-4765.00. The daily Cycle Top resistance is at 4769.67, imposing its own limitations on the rally. SPX may have the ability to send one more probe higher today, completing the retracement.

Note: The 10-year Treasury Note Auction is being held today and the 30-year bond auction will be offered tomorrow.

ZeroHedge observes, “One day after a stellar 3Y auction launched the coupon Treasury issuance for 2024, moments ago we got the sale of the first benchmark piece of paper for the new year, when some $37BN in a 9-Year 10-Month reopening were sold to the public in a generally strong auction.

The auction priced at a high yield of 4.024%, which was a sharp drop from December’s 4.2960 and was the lowest yield since the 3.999% August auction. More notably, the high yield tailed the When Issued 4.019 by 0.5bps. This was the 4th consecutive tailing 10Y auction, and the 11th non-stop through auction in a row (September was on the screws). More remarkably, there have been only 3 stop-through 10Y auction in the past 27 months!”

10:00 am

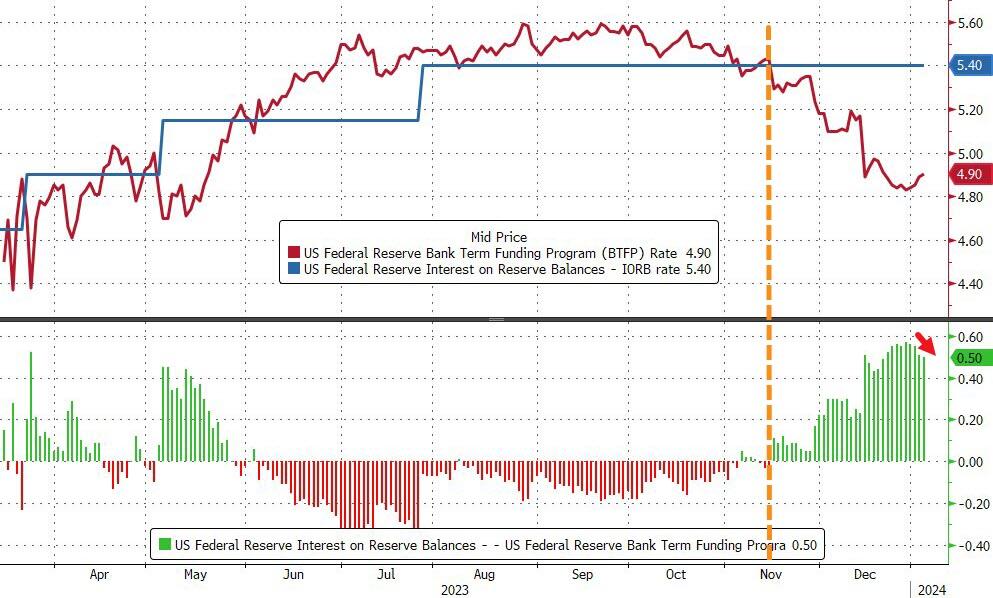

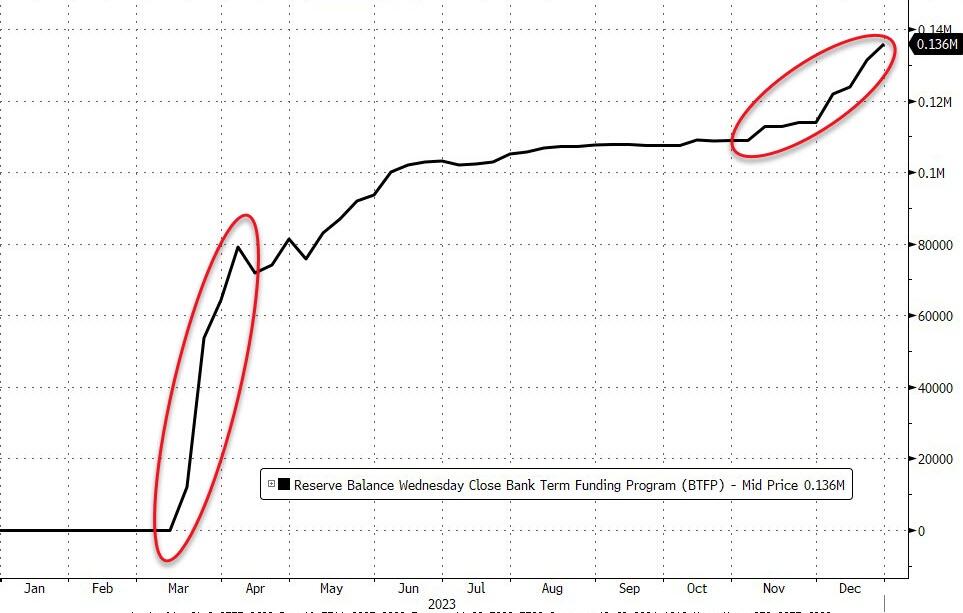

BKX has dropped to the lower end of its one-month trading range. Should it decline further, a bearish cross beneath its Cycle Top support at 94.57 may produce a sell signal. Today is day 251 of its current Master Cycle, a week early. However, should the decline take place, it may confirm the top is already in. Should the BTFP expire, the Federal tit is removed and banks may have to fend for themselves. Should rates also rise, the outcome may not be pretty.

ZeroHedge remarks, “The Federal Reserve is likely to retire the Bank Term Funding Program in March. This would entail an additional ongoing headwind for reserves, and thus liquidity, through 2024. At the margin, this adds weight to the case for the Fed cutting interest rates sooner in the year.

The BTFP was created in the wake of the SVB crisis to help struggling banks get access to liquidity when bond prices were dropping. However, its use in recent months has jumped to over $140 billion. That is not, however, a sign of banking stress.

The chart below shows the usage of the BTFP along with the rate paid at the 99th percentile in the fed funds market relative to the upper bound of the range for fed funds.

As can be seen, this is under zero, i.e. banks are not having to pay up to get liquidity.”

8:50 am

Good Morning!

NDX futures remain stalled at the short-term resistance at 16662.27 and a 64% retracement of the first week decline. Today is day 259 of the (old) Master Cycle, leaving NDX with diminishing capabilities of a new all-time high. Should the decline resume, it may do so with an increased intensity as momentum factors are increasing.

Today’s options chain shows Max Investor Pain at 16725.00. Long gamma may begin at 16750.00 and short gamma starts strong at 16720.00. Dealers may be fighting a negative tape today.

ZeroHedge remarks, “Market narratives have been around for ages. However, the internet and, more recently, social media allow narratives to spread much quicker. Accordingly, they have become more frequent and potent market forces. Following economic data, corporate earnings, politics, global affairs, and many other factors are still crucial for investors. But equally important, especially over short periods, is identifying which narrative(s) most heavily impact markets. Today’s popular narrative is a growing consensus for the Fed to engineer a soft landing and a Goldilocks economy. It’s worth appreciating the Fed and Jerome Powell, purposely or not, started the narrative.

As the fiscal stimulus that drove above-average economic growth in the post-pandemic era exits the system and monetary policy remains very tight, economists and investors wonder what comes next. The scenario rapidly gaining in popularity is the Goldilocks narrative.”

SPX futures remain flat beneath the 1987 trendline at 4765.00. There was a slight gain yesterday to the 67% retracement value, also at 4765.00. We canot rule out the potential for another probe higher, but the old Cycle is winding down with less and less capability to forge higher. On the other hand, should a reversal take place today, the Cycles Model suggests a potential for a panic decline over the next week.

Today’s options chain shows Max Pain from 4745.00 to 4755.00. Long gamma starts with a 7,520 contract call wall at 4760.00. Short gamma begins at 4740.00. Speculation is overwhelmingly bullish.

ZeroHedge reports, “US stock futures were unchanged, trading in a narrow range and shifting between modest gains and losses, as investors clung to the sidelines ahead of a key US inflation report. As of 7:50am, Nasdaq 100 futures gained 0.1% while S&P 500 index futures were little changed. The Treasury 10-year yield crept back under 4%, before recovering much of the move. The Dollar was also unchanged while the yen tumbled after the latest Japanese wage data confirmed there will be no rate hikes soon, if not ever. Brent crude rose 0.5% and was trading just below $78 a barrel in a choppy session following more attacks on vessels in the Red Sea that could upset both oil supplies and trade flows. Bitcoin dropped to trade around $45K after a hacked post on the SEC’s X/twitter account prompted large price swings on Tuesday. Today’s calendar is sparse: just wholesale inventories and trade on deck.”

VIX futures are consolidating near yesterday’s low. Today is day 254 in the Master Cycle and we are looking for a bottom before the week is over.

Today’s options expiration shows Max Pain at 13.00. There is a small contingent of short gamma at 12.00. Long gamma starts at 15.00 and runs to 37.00.

TNX is marching the flat line at 40.00 this morning. Should it succeed in going higher, the neckline at 41.00 may be in its sight. The 10-year and 30-year auctions will be interesting to watch. The Cycles Model indicates trending strength to start rising.

ZeroHedge observes, “While not nearly as interesting as the upcoming long-duration 10Y and 30Y auction later this week, all eyes were on today’s sale of 3Y paper as it was the first coupon auction of the year. And despite some erroneous previews at competing publications, the auction was nothing short of stellar.

Pricing at a high yield of 4.105%, down 38.5bps from the December yield of 4.490%, and the lowest 3Y high yield stop since May 2023, today’s auction stopped through the When Issued 4.116% by 1.1bps, the biggest stop through since Aug 2023.

The bid to cover was 2.672, a solid jump from the 2.416 in December, and the highest since September.”