12:46 pm

SPX has declined to the convergence of the short-term trendline and the 1987 trendline. A break beneath the double trendline offers an aggressive sell signal. One should not own stocks beneath that point. The first confirmation is at the short-term line at 4698.96 (4700.00), another aggressive confirmation. Take advantage of these supports to unencumber yourself of any longs. Shorts may be taken at those points, as well. When the liquidity spigot closes, we may see a “no bid” event.

ZeroHedge remarks, “Over a month ago (and well before the Fed’s “shocking” dovish pivot) as the Fed’s Overnight Reverse Repo tumbled below $900 billion for the first time since June 2021 amid a growing debate of where and when the Fed’s reserve scarcity constraint will be hit, we warned that liquidity is rapidly approaching the reverse repo constraint level which could emerge as soon as the RRP facility dropped to $700 billion, at which point the market’s all-important credit plumbing will start to crack”

ZeroHedge further observes, “Earlier today, when discussing the sudden spike in the SOFR rate to an all time high 5.40% and which dragged the SOFR-Fed Funds spread to the highest since the March 2020 repo crisis…

… we said that “two factors are the likely culprits: the year-end liquidity crunch, and the recent sharp increase in the Fed’s reverse repo facility, which has increased from a multi-year low of $683 billion on Dec 15 to yesterday’s $830 billion, and which STIR strategists expect will shoot up above $1 trillion in today’s final for 2023 reverse repo operation as a whopping $300+ billion in short-term liquidity in pulled from markets in just days.”

9:30 am (short session)

SPX futures attempted a new high by briefly reaching 4795.30, but fell back to a flat position. The cash market high has been 4793.30 thus far. The rally formation is complete, or nearly so. Today may remain flat on weak volume as the book for 2023 is closed for many. The rising trendline and the 1987 trendline bot reside at 4750.00. An aggressive sell signal lies beneath them. The Cycle Top resides at 4732.30 which may confirm the sell signal.

Today’s options chain shows 4780.00 is hotly contested and offers the Max Pain. Long gamma starts at 4800.00 while short gamma may begin at 4775.00.

ZeroHedge reports, “US futures once again flirted between gains and losses on the last trading day of the year, but with the all time high in the S&P just 0.3% away, it is virtually guaranteed that the script calls for a new record to close out 2023 because that’s how centrally-planned markets work. And who knows, maybe this time BIden’s approval rating will actually increase; after all that’s what all of this is about.”

VIX futures consolidated inside yesterday’s trading range, without the energy to break up or down. However, it has completed its first positive hourly Cycle since the Master low on December 13. The new Master Cycle may extend to mid-January with an upward bias.

Wednesday’s options chain shows Max Pain at 13.50. An 11,000 call contract at 11.00 negates the potential short gamma. Long gamma otherwise begins at 16.00 and extends to 30.00.

TNX opened higher this morning, putting more distance from its probable Master Cycle low on December 27th. There are multiple indications that yields have stopped going lower.

ZeroHedge remarks, “It’s only appropriate that a year which saw 10Y rates soar above 5%, the most in 16 years, before sliding on fears of an imminent recession and/or Fed easing cycle, that the final coupon auction of the year was a dog with a capital D.

Yesterday’s far stronger than expected 5Y auction surprised many: not only was there no concession with yields tumbling all day, but there was no tangible reason for the burst in demand that lead to one of the strongest stop-throughs on record, besides perhaps a big squeeze overhang as shorts sought to cover in the year’s last trading hours. Well, moments ago we did get confirmation that yesterday’s strength was indeed technically-driven because the $40BN in 7Y paper that was just sold by the Treasury could be described by just one word: ugly.”

BKX continues to hover near its retracement high. As noted, TNX is beginning to rise, indicating that liquidity may be drying up. Should that be the case, a decline beneath the Head & Shoulders neckline may be imminent.

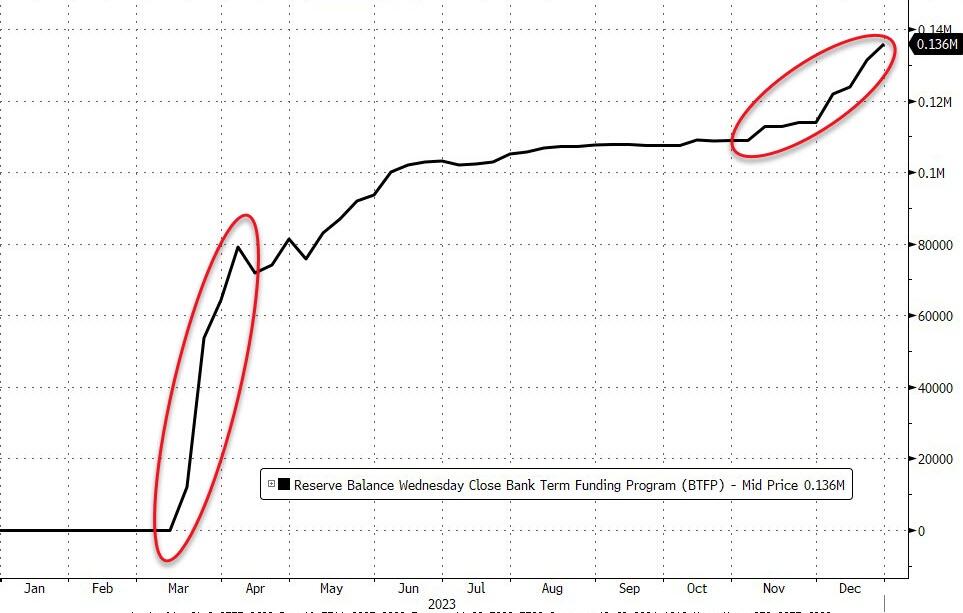

ZeroHedge notes, “Usage of The Fed’s bank bailout facility rose by another $4.5BN last week to a new record high of $136BN…

Source: Bloomberg

But Regional bank shares don’t care…”

The Ag Index made its Master Cycle low on December 21. There is no visible buy signal except the Cycle low. Overhead resistance is at 395.98, beyond which lies a confirmed buy signal.

ZeroHedge observes, “The war in Ukraine has transformed parts of the Black Sea into a conflict area. Commercial vessels transporting agricultural goods from the ‘breadbasket of Europe’ have been caught in the crossfire.

The latest maritime incident occurred on Wednesday when a Panama-flagged bulk carrier struck a mine in the Black Sea while sailing to a port on the Danube River to load grain, according to Reuters.

“A Panama-flagged civilian vessel was blown up on an enemy sea mine in the Black Sea … The vessel lost its course and control, and a fire broke out on the upper deck,” Ukraine’s southern military command said on Telegram.”

For those with a sweet tooth, ZeroHedge remarks, “Cocoa prices Wednesday hit $4,285 per ton in New York, the highest level since 1978, as the outlook of poor crop harvests across West Africa has been a major bullish factor pushing prices higher this year. There is also an increasing risk that El Nino-induced weather disturbances could cause the global cocoa market to sink into a deficit for the third year.”

On the other side of the world, shortages lurk. ZeroHedge reports, “On Wednesday, the Thai Rice Exporters Association revealed that the price of Thai white rice 5% broken, a key Asian benchmark, reached a new 15-year high. This surge is mainly attributed to increasing fears of a global shortage due to the damaging effects of the El Nino weather phenomenon on Asian farmlands and India’s recent decision to restrict certain rice exports.

Thai white rice 5% broken hit $659 a ton, the highest level since October 2008. Prices of the staple food that feeds billions of people worldwide are up over 50% since the start of 2022. ”