9:40 am

On of the biggest beneficiaries of the Fed largesse is the banking sector. At the end of October BKX was threatening to break through the neckline of a 4-year wide Head & Shoulders formation near 71.00. Banks are scrambling by laying off employees and cleaning up their portfolios while conditions are eased. Interest rates are due to start rising again after the first of the year, which may reveal how poorly prepared the banks may be.

ZeroHedge remarks, “The collapse of three US regional banks – First Republic Bank, Silicon Valley Bank, and Signature Bank – marked some of the largest failures in the banking system since 2008. Central banks contained the “mini-crisis” earlier this year with forced interventions and the mega-merger of Credit Suisse and UBS. Despite the interventions, global banks still axed the most jobs since the global financial crisis.

A new report from the Financial Times shows twenty of the world’s largest banks slashed 61,905 jobs in 2023, a move to protect profit margins in a period of high interest rates amid a slump in dealmaking and equity and debt sales. This compared with the 140,000 lost during the GFC of 2007-08.”

8:15 am

Good Morning!

NDX futures consolidated under the all-time high this morning. Usually a key reversal such as the one we witnessed last week would have been the end of the line for the rally. However, it did not break the uptrend, allowing the NDX to go even higher. The trendline is near 16800.00 which, if broken, may begin the decline. Recent information shows that the 0DTE investors having a hand in this rally is an urban myth. Retail investors have been absent from this rally thus far.

Today’s options chain shows Max Pain at 16920.00. Long gamma may begin at 16930.00 while short gamma begins at 16910.00. Large investors are taking positions against the rally. It may be to “protect” their profits but may be a spark for a reversal.

ZeroHedge remarks, “That perfect storm

A tsunami of capital has been competing for stocks in December. Buybacks, equity inflows, CTAs and hedgies. SPY has drawn around $40 billion in inflows in December, on track for the biggest monthly haul since it began trading in 1993.

Source: FactSet

Elevated positioning

ETF flows, vol target, CTA and CFTC components are all at elevated levels.”

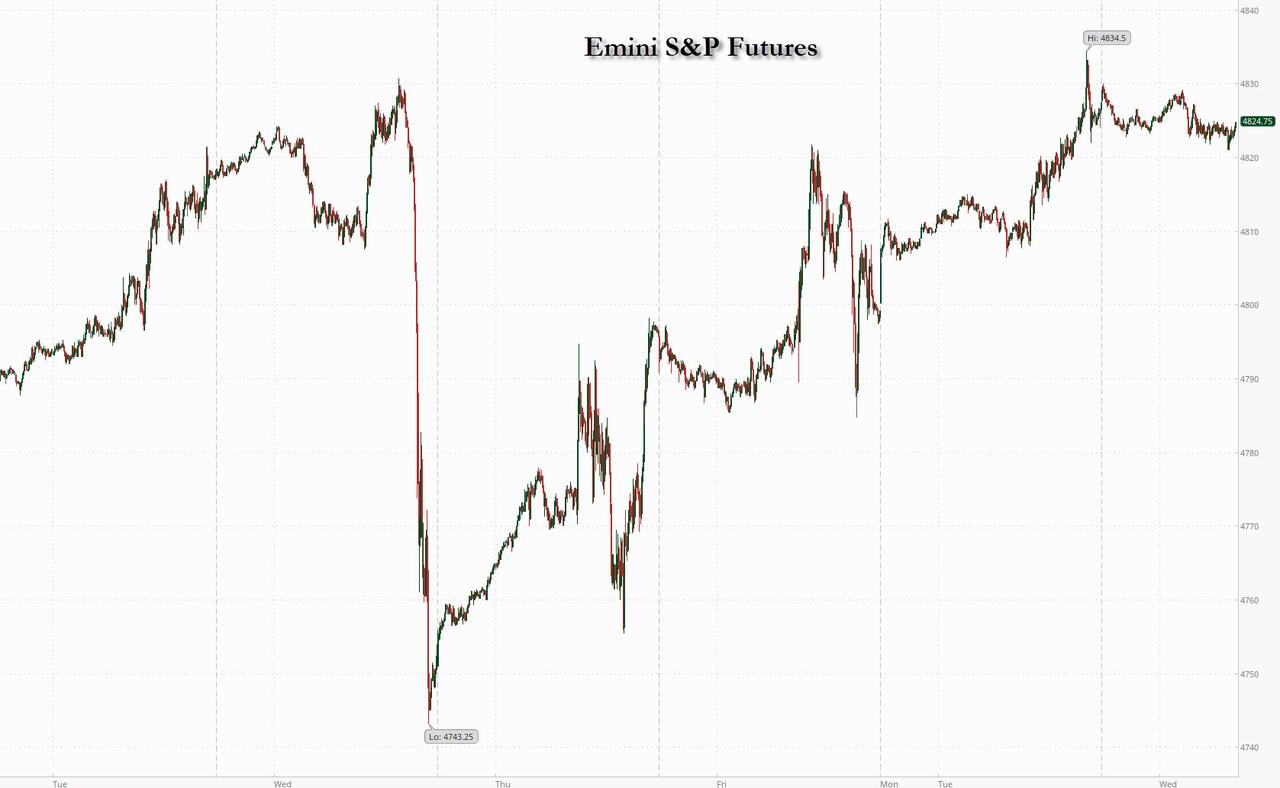

SPX futures are also consolidating near the highs. SPX is in a throw-over formation, usually associated with a final push in an uptrend. As mentioned earlier, large, liquid institutions are dominating the rally to date. They are also building their hedges, waiting for retail investors on which to offload their books. The next target is the January 2022 high that may be taken with lots of fanfare to incentivize the retail investors to join the party. There remains an overhead resistance at 4795.00 that may have the potential of stopping the rally. Keep an eye on that level.

Today’s op-ex shows max Pain at 4755.00 to 4765.00. Long gamma may begin at 4780.00 to 4800.00 while short gamma may start at 4740.00.

ZeroHedge reports, “US futures were flat in muted trading following yesterday’s gain which pushed the S&P to within fractions of an all-time high amid trader hopes that the Federal Reserve is getting close to cutting interest rates, even if it means sparking another violent bout of inflation. As of 8:15 am, futures on the S&P 500 and the Nasdaq 100 indexes flirted between small gains and losses; after rising 0.4% on Tuesday, the S&P is heading for a seven-week winning streak and resides within 0.5% of the record high reached early last year. 10Y yields slumped to session lows around 3.842%, down 5 bps from Tuesday’s close, while Brent also dipped about $1, sliding below $80.”

VIX futures are testing yesterday’s low. It may hold, even though bottom support is at 12.76. VIX may be due for a burst of trending strength today as shown in the Cycles Model. VIX is on an aggressive buy signal. Aggressive signals come early in a trend and are subject to blow-back. If held with patience these signals may produce the best results.

Today’s options chain shows virtually no short gamma. Long gamma starts at 13.00 and extends to 24.00.

TNX futures have declined to 38.37 thus far. There appears to be a concerted effort to re-liquify the markets by keeping rates low. Today is day 252 of the Master Cycle leaving about a week in which yields may fall. The reason may be that the Treasury auction schedule shows no bond being sold for the balance of 2023. The five year and seven year notes are on the block in the next two days. This may artificially increase demand for the 10-year notes and 20-year bonds.

ZeroHedge observes, “Despite resilience in US data, 30Y Yields have plunged back below the 4.00% Maginot Line this morning…

Source: Bloomberg

The last few weeks have seen US macro data reverse its recent trend of disappointment…”