8:20 am

Good Morning!

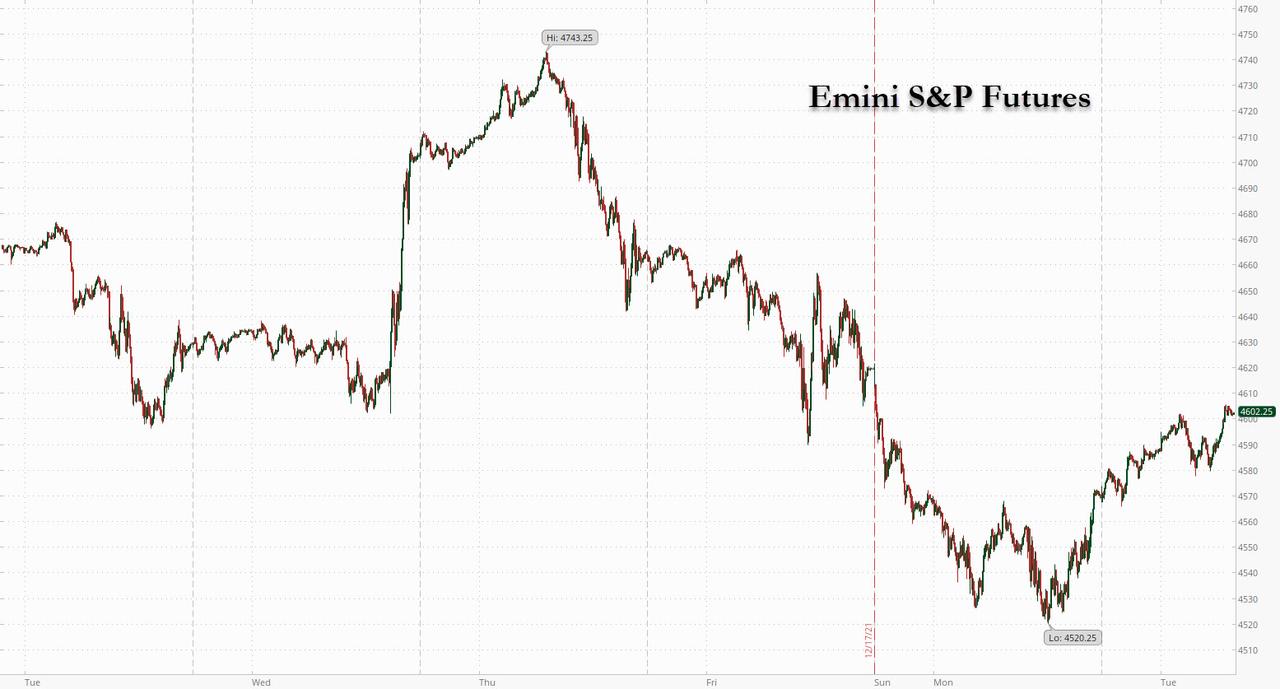

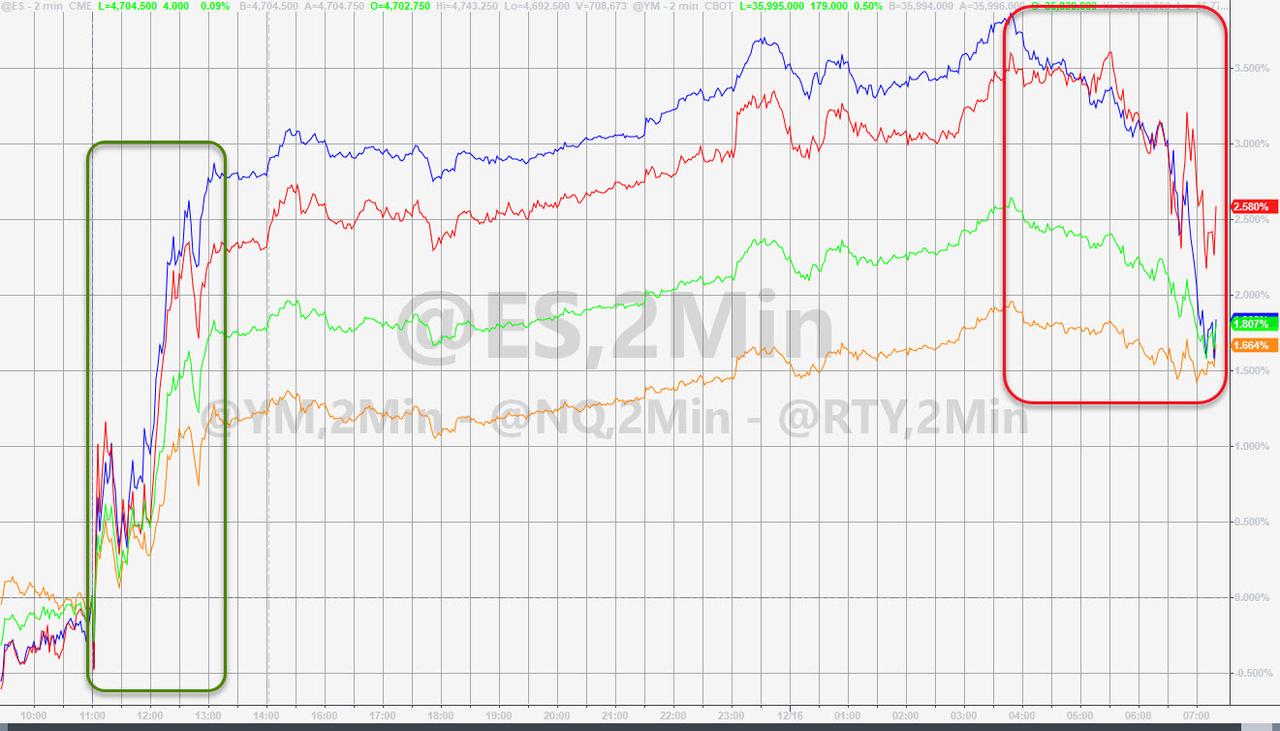

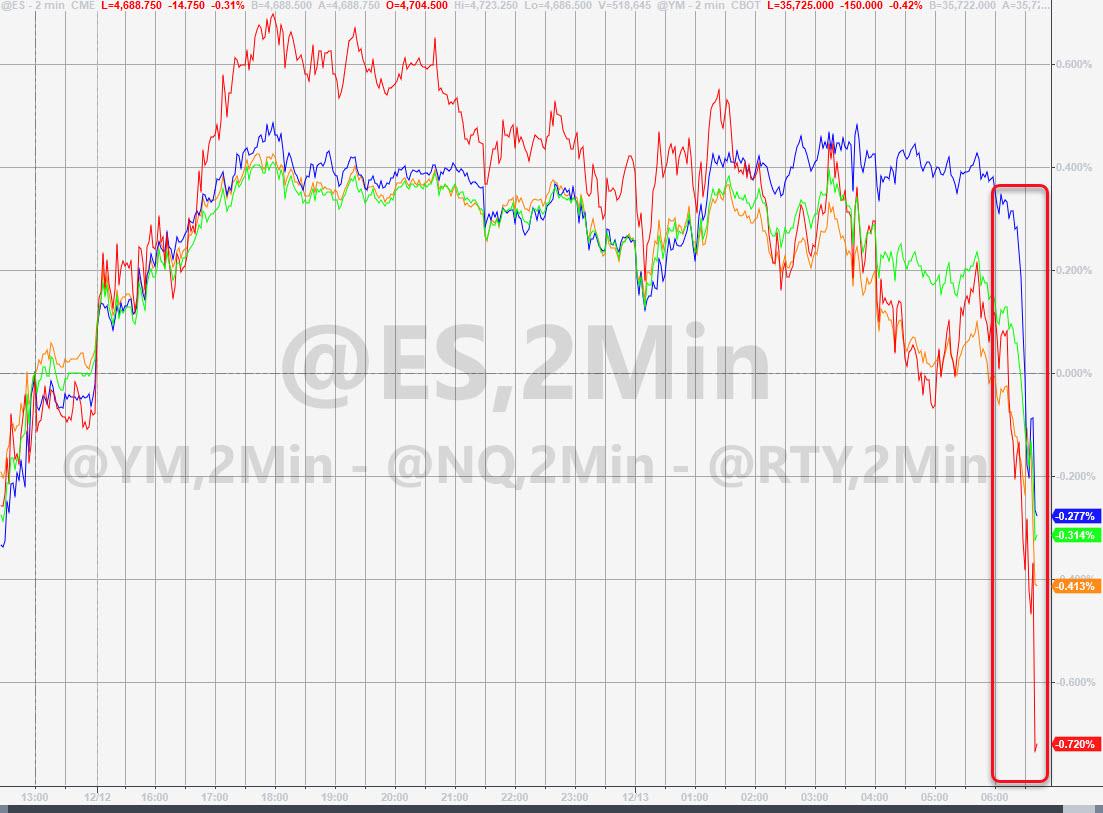

SPX futures may have completed its retracement at the 61.8% level at 4655.00 this morning. It has been moving lower since then. Just a note on Cycles; trending moves are very likely to follow precise Cyclical patterns while counter-trend moves often do not. Yesterday, after 8.6 hours of a counter-trend bounce I was ready to call it “done,” when it was not. However, the bounce had gone far enough to be actionable. While I do not normally measure futures in Cycles, I noticed that the turn came at the next 8.6-hour interval this morning. Back in the cash market, the current hourly Cycle may be complete by or soon after 11;00 am.

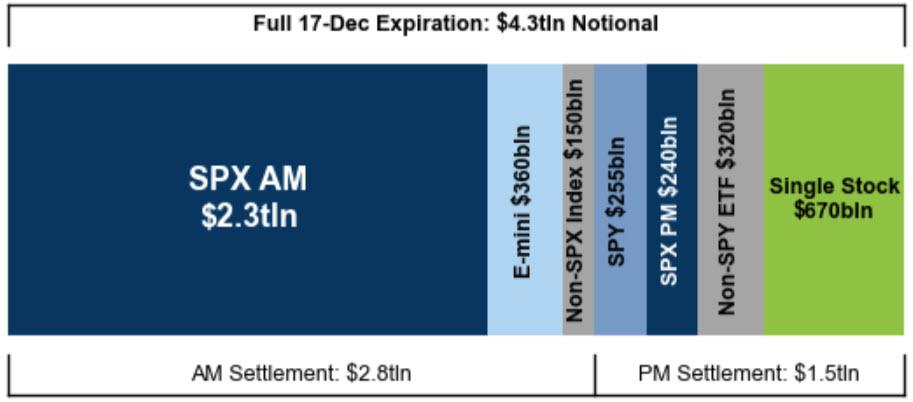

Today’s expiring options show Max Pain at 4600.00, suggesting that SPX options gamma is currently positive. Both 4620.00 and 4630.00 strikes have over 12,000 net open interest call contracts.

ZeroHedge reports, “Tuesday’s rally fizzled on Wednesday, as US emini futures were flat after erasing an earlier dip as attention again turned to news about the omicron variant as cases surged globally. Contracts on the Nasdaq 100 led declines, slipping 0.3% in thin trading ahead of holidays. In Europe, stocks were little changed as more omicron woes weighed on sentiment. Oil steadied as investors assessed mixed demand signals and the dollar fell. Elon Musk sold even more Tesla shares, one step close to his promise to sell 10% of his stake in the electric carmaker.”

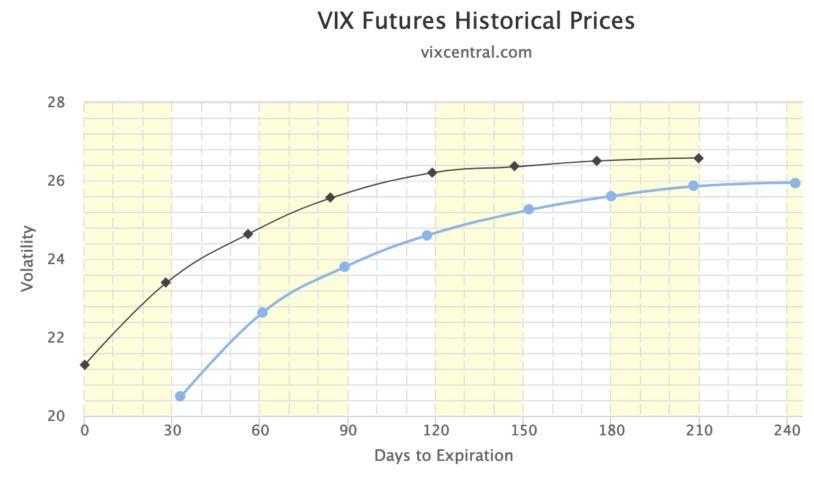

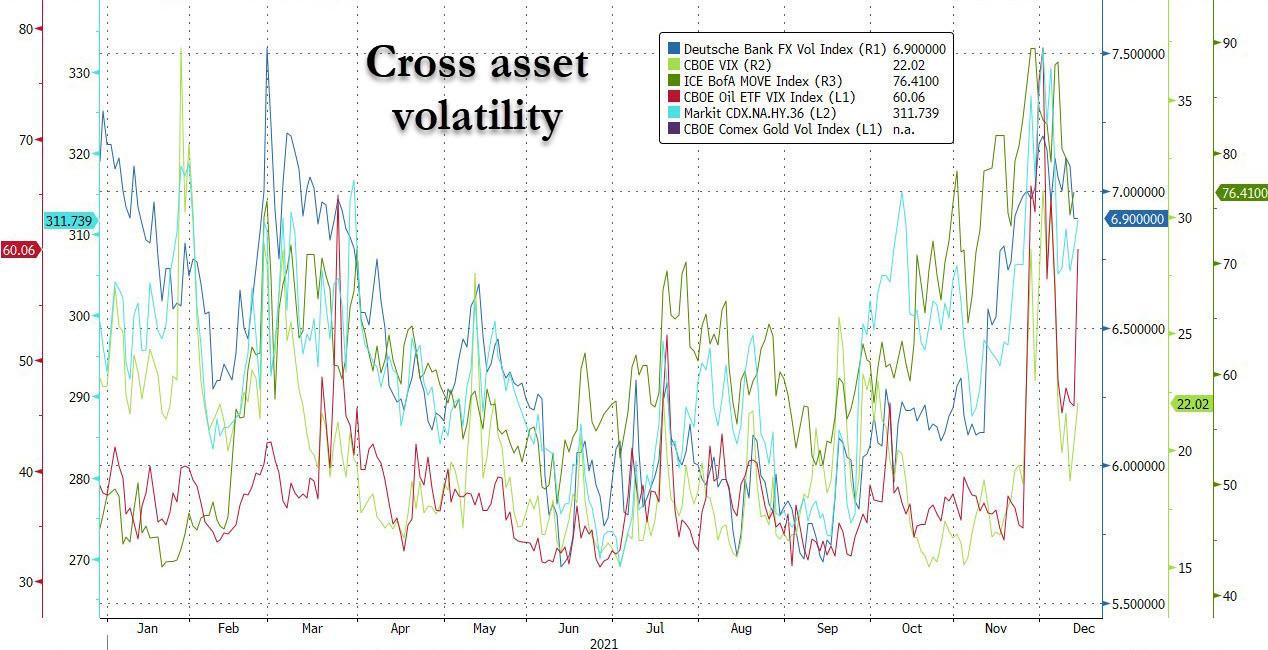

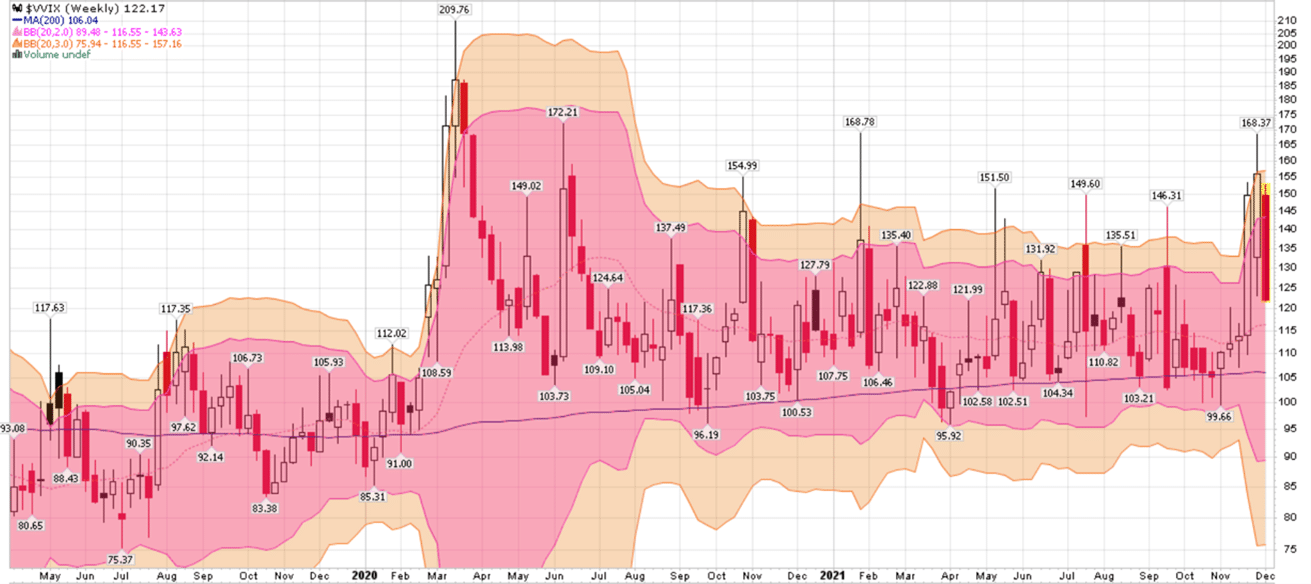

VIX futures began their advance this morning after reaching an overnight low of 20.52, completing its retracement. Yesterday’s move has most analysts convinced that VIX is going lower, issuing in the Santa Rally in stocks.

In today’s market, the Max Pain zone in expiring VIX options is at 24.00, making that price a likely target for the close. However, gamma turns positive immediately at 25.00 and ramps up from there.

ZeroHedge comments, “How was “fear” last Christmas?

We have witnessed some rather big moves lately. Volatility is not cheap if you are trying to finance the theta, but how did the vol indexes trade last year?

V2X traded around these levels, but note VIX was actually averaging higher levels than current “elevated” levels.

Source: Refinitiv

Volatility – they (must) love you

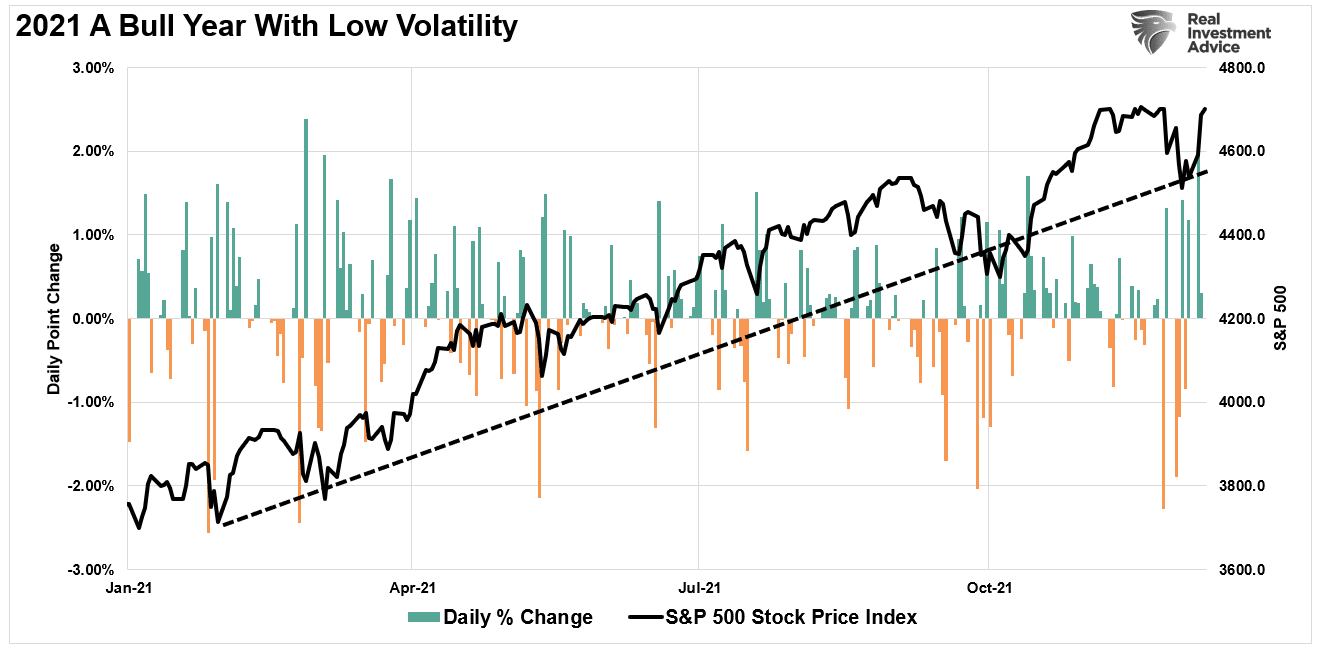

Nobody has missed the latest moves in VIX. An extreme year finishes off in an extreme way, where markets continue to move sharply from realizing low vol to high vol. 2021 full year vol is marginally higher than 2019, but “nervous” investors have pushed vols into a consistently higher vol range than pre Covid 19, writes GS.”

The NYSE Hi-Lo Index closed negative after reaching a neutral 24.00 yesterday, despite the seemingly strong rally in the SPX. Short covering does not drive the Hi-Lo. New money does. This shows the enthusiasm for new money going into stocks is waning.

TNX is pulling back to retest the 100-day Moving Average at 14.47 this morning. This move also suggests new money arriving on the long side in treasuries. The three-month-old sideways consolidation in TNX may be about to change, as the Cycles Model suggests a spurt of strength beginning today, which may allow TNX to emerge above the resistance of the 50-day Moving Average at 15.34.

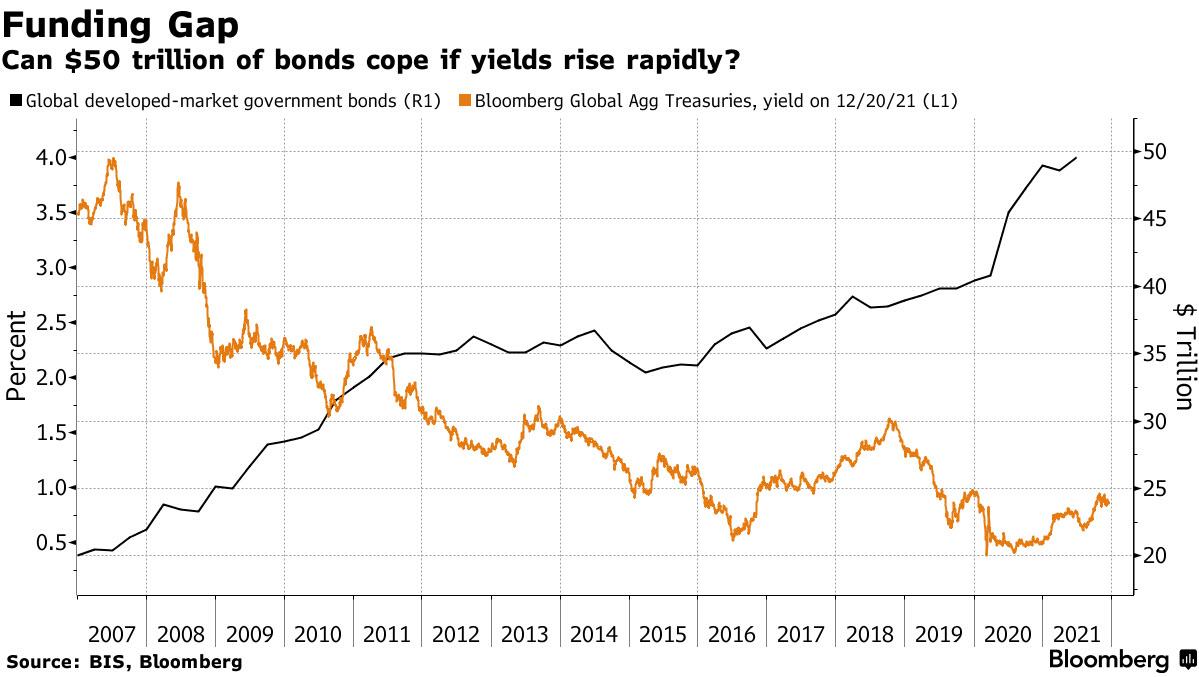

ZeroHedge remarks, “The size of the global government bond market surged by $10 trillion in the space of two years to reach about $50 trillion. Those outstanding borrowings are at least one gorilla in the room as investors gear up for a year in which yields are expected to climb as central banks step back and economies extend their recovery.

The massive bond mountain is not getting much attention, despite the explosive pace at which it grew in size and given the potential it holds to cause extreme havoc. That could be because it is simply too large to seriously contemplate, but the rapid growth in debt is one of the many Covid-era phenomena spicing up the market outlook for the coming year”

The Banking Index gapped above the Lip of the Cup with Handle formation at 128.70 in a 56% retracement of its prior decline. Note that this formation may also be interpreted as a Head & Shoulders formation with a shorter target. However, the extra bounce above the trendline allowed the more bearish formation. Head & Shoulders don’t usually allow the affected index to re-emerge above the trendline, while the Cup with Handle is more permeable.