3:50 pm

NDX has reversed at the 33% retracement level. The decline may resume at this point.

ZeroHedge observes, “A few days ago, with the Nasdaq at all time highs, we showed a striking chart: barely 40% of the Nasdaq’s 3,000+ stocks were trading above their 200 day moving average.

While not nearly as dramatic, a chart comparing the broader S&P and the median stock (via the Value Line Geometric) showed a similar theme: barely a handful of stocks were propelling the entire market higher, and it’s also why two weeks ago we summarized the current state of affairs “They better not start selling the generals”

3:45 pm

SPX retraced to the 38.2% Fib retracement at 4647.41. It has reversed down from there.

2:32 pm

NDX has fallen to its 50-day Moving Average at 15724.62. There has been a bounce, but the impulsive decline may not be complete and may resume shortly. In doing so, it may break through the 50-day and the 2-hour Cycle Bottom at 15632.27, giving NDX additional room to decline.

ZeroHedge observes, “It’s not the economy; it’s the positioning, stupid.

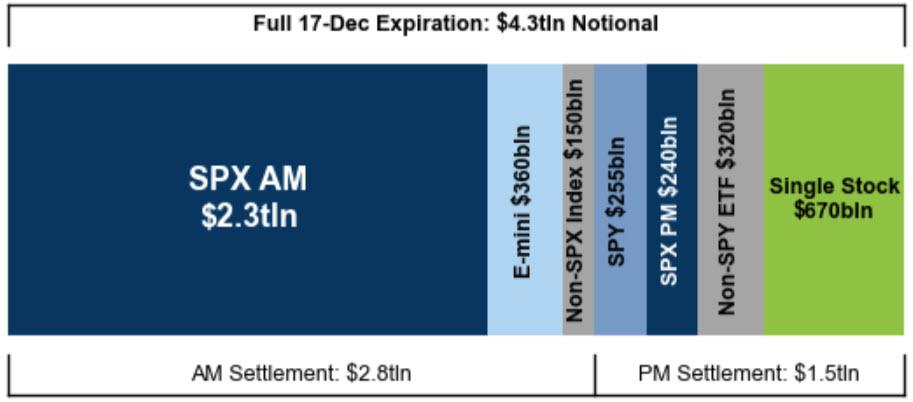

That’s the clear message from Goldman Sachs and SpotGamma as traders ready themselves for a tumultuous week navigating the implicit volatility of tomorrow’s Fed statement, dot-plot, and press conference as turbo-taper-talk is expected, ahead of a very significant options expiration on Friday.

$4.3tln notional of equity options (referencing over 8% of the Russell 3000’s market cap) are expiring (including $2.3tln of SPX quarterly options, $360bln of options on SPX E-mini futures, $255bln of SPY options, and $670bln of single stock options).

This has historically been the most active week of the option trading year.

The Dec-2021 OpEx has less total open interest than last December’s expiration did, but more of its open interest is near the money than last year’s was. While this is the smallest December expiration in at least a decade, but larger than just about all non-December expirations.”

2:10 pm

SPX may have completed an impulsive decline ending at noon. It may now be in a correction with resistance at 4633.00 to 4655.00. The next hourly interval is at 3:00 pm, suggesting that, should the bounce stop at or under the resistance zone, it may resume its decline in the final hour. There is a lot of talk of the Christmas rally beginning. However, the decline is not over yet and the 50-day and trendline await. The NYSE Hi-Lo is at -41.00 and the NDX Hi-Lo is at -260.00. Caution is warranted.

ZeroHedge remarks, “If the infamous tantrum of 2013 was all about the bond markets, this time it may be about stocks. And Monday’s selloff in the S&P 500 and Nasdaq show that traders are getting increasingly nervous about the prospect of the Fed preparing to raise rates, perhaps sooner than earlier thought.

The Nasdaq Composite Index has had an outsized move — a needle that takes it more than 1 standard deviation in either direction based on changes in the past year — on as many as nine occasions in the past month alone. Of course, most of those bigger bands have been shaded in red, perhaps suggesting that traders see the writing on the wall.”

7:50 am

Good Morning!

SPX futures made a low of 4650.40, challenging the mid-Cycle support at 4653.00. Crossing this level confirms the minor trendline break and sell signal. The chart shows a minor bear crossing, where Short-term support/resistance has crossed beneath the mid-Cycle line. The December 15 options expiration shows Max Pain at 4700.00 with bearish gamma beginning at 4680.00. Yesterday’s Key Reversal did not occur on a Master Cycle interval, but is important in establishing the declining trend ahead. Once mid-Cycle support is broken, the next very important support is the 50-day at 4551.98, right alongside the 20-month trendline. Beneath this the decline may be universally recognized.

ZeroHedge reports, “US stock futures fell on Tuesday, reversing an earlier gain, as traders prepared for this year’s barrage of final central bank meetings this week. Treasury yields advanced and the dollar slipped. European stocks were little changed while Asian stocks dropped led by Japan whose Prime Minister Fumio Kishida hinted the government may consider guidelines for share buybacks (a tapering of stock buybacks in the US would lead to an instant market crash). At 745am, S&P futures were down 0.17% or 8 points to 4,651; Nasdaq futures were down 0.5% erasing earlier gains of as much as 0.3% as traders assessed the impact of a less accomodative monetary setting amid coronavirus challenges and high valuations.”

VIX futures made a new overnight high at 21.55 as it begins regaining altitude. The Cycles Model shows the next Master Cycle interval in two weeks. This is likely to be the top of Wave 3, at or above the Head & Shoulders target, discussed yesterday. That interval does not show in the Hi-Lo Index or the SPX Cycles Model, primarily due to the fact that the end of December would only be a Minor Wave 1 in the SPX. The Wave 3 low, which occurs in the 4th week of January does register in the Cycles Model, however.

The NYSE Hi-Lo Index closed at -31.00 after struggling to remain positive during the morning hours. It is on a sell signal and may remain so through the end of January. The NDX Hi-Lo Index closed at -267.00, indicating the decline is gaining intensity.

NDX futures declined with more intensity to 15924.30 this morning, in agreement with the stronger decline in the Hi-Lo. Yesterday’s decline broke the two-week sideways consolidation with the next target the 50-day Moving Average at 15705.18.

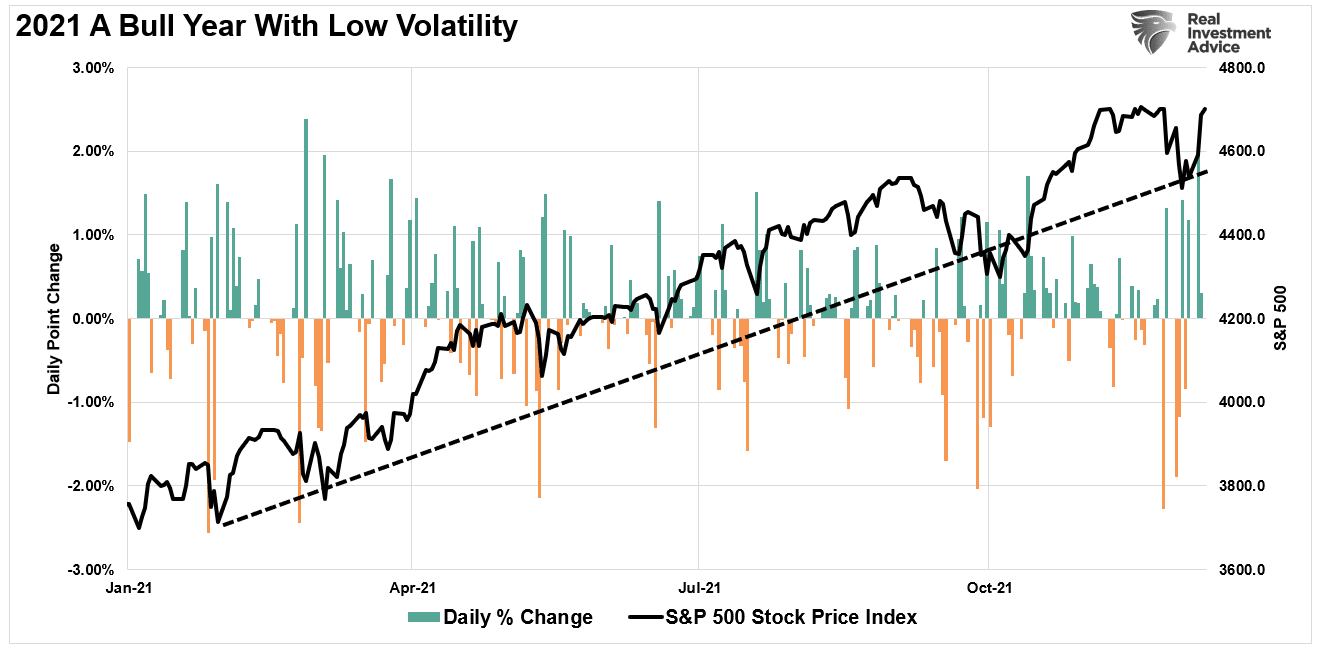

RealInvestmentAdvice declares, “Wipe Out” is an appropriate description of what is happening beneath the calm surface of the bull market.

As we head into the end of the year, many are hoping for “Santa to visit Broad and Wall.” However, those hopes are not just about adding to this year’s already excessive annual gains. Instead, for many, it’s the hope to recover some brutal losses.

If you haven’t been paying much attention, the market is currently sitting near all-time highs. While it has risen nearly 26% this year, there were a couple of very normal 5% corrections along the way.

By looking at the chart, you would assume that performance across the index was pretty equal. However, that would be an erroneous assumption.

As the old saying goes:

“You can’t judge a book by its cover.”

TNX declined beneath its 100-day Moving Average at 14.29 this morning, primarily due to liquidity migrating from equities to Treasuries.

ZeroHedge observes, “After CPI’s rise last week (which was somehow briefly seen as ‘good’ news because it was lower than a wild whisper number), Producer Prices tore up the narrative this morning printing a record breaking 9.6% YoY rise (smashing expectations of +9.2% and well above the +8.6% YoY print for October)….

Source: Bloomberg

Worse still, core PPI surged:

- Ex-food and energy +7.7% YoY vs +7.2% exp and +6.8% prior

- Ex-food, energy, and trade +6.9% YoY vs +6.3% prior

Both Goods and Services prices rose with Energy and Transportation costs the biggest drivers.”

USD futures are challenging the Cycle Top support at 96.20. This corrective action may continue through the end of the week. However, the uptrend may resume next week, with strength.