2:45 pm

SPX may complete the bounce at the 61.8% Fib retracement level at 4672.68. Oddly, the Max Pain zone for today’s options expiration appears to be at 4770.00. We may be spending the final hour of the day near that level. We could see a turn in the final hour or possibly near the open tomorrow. The NYSE Hi-Lo Index is currently at -91.00 and the NDX Hi-Lo is currently at -389.00.

There is another resistance provided at the bottom of yesterday’s gap down at 4660.00, which is also the 50% retracement level. Waves C and 3 often leave unfilled gaps. NDX has also met its gap at 15995.21. In that case, the reversal may come in the final hour of the day.

ZeroHedge reports, ”

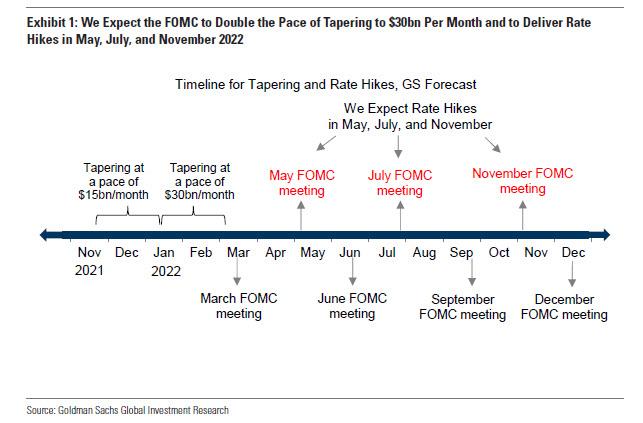

- The Fed statement and economic projections saw the central bank double the pace of its asset purchase tapering to USD 30bln per month (consisting of USD 20bln Treasuries, USD 10bln MBS – this will be doubled again in January, with similar reductions likely be appropriate each month thereafter), which puts it on course to conclude asset purchases by March, from the prior landing zone of around June, although this could be adjusted if warranted.

- Its updated projections now see three rate hikes in 2022, revising up its view from one hike pencilled in at the September FOMC (recall that September, the Committee was essentially split on the potential need for a second 2022 rate hike); longer-term, it has left its terminal rate view unchanged, however.

- Inflation forecasts were revised up to 2.6% for headline PCE by the end of next year (prev. 2.2%), while the core measure is seen at 2.7% by end 2022 (prev. 2.3%).

- On the labour market, the Fed sees the jobless rate return to the 3.5% mark next year (prev. saw 3.8%), where it is likely to stay over its forecast horizon.

The bottom line is that this was largely in line with what the market was expecting (accelerating taper, raising inflation forecasts, seeing continual progress in the labour market), where the Fed sees the economy continuing to grow (its growth view for next year was revised up, although 2023’s pace was revised down a touch).”

8:30 am

Good Morning!

SPX futures were flat this morning, remaining between 4630.00 and 4646.50, as suggested yesterday afternoon. Should SPX go higher, the next hourly turn interval is near 1:00 pm. Go figure.

Today’s expiring options are light, but negative beneath 4670.00. Friday’s options are massive, with the entire span between 4600.00 and 4700.00 loaded nearly equally with both puts and calls. I have never seen anything like this. Sentiment appears to be turning bearish, but the bulls still have not given up. As previously mentioned, sentiment may “flip” as SPX ventures beneath the 50-day Moving Average at 4576.55.

Zerohedge reports, “With the long-awaited Fed day finally here and Powell set to reveal the “turbo-taper” which doubles the pace of QE unwind to $30BN per month starting in January and ending by March, and to publish updated summary of economic projections, so the Fed can hike in April or May as Goldman laid out over the weekend…

… S&P futures were flat, Nasdaq futures dropped as traders braced for another dose of hawkishness on the pace of the withdrawal of stimulus measures and rate increases. Treasury yields and the dollar were little changed. Europe’s Stoxx 600 Index gained after five days of losses, Asian stocks were mixed with Nikkei closing slightly higher, the Hang Seng tumbled by as much as 2.2%, with Semiconductor Manufacturing among the biggest contributors to its decline, as the U.S. is said to be considering tougher sanctions on China’s biggest chipmaker.”

VIX futures are also flat, as it consolidates inside yesterday’s trading range. It’s not clear on the daily chart, but VIX is coiling for its next move higher.

The NYSE Hi-Lo Index fell dramatically yesterday, closing beneath the Cycle Bottom support. While the SPX seems not to be eager for the decline, the internals are falling apart. Do I hear the word “implosion” being used yet?

The NDX Hi-Lo Index closed yesterday at -444.00.

TNX is rising off the 100-day Moving Average this morning as it ventures into a period of strength that suggests a possible breakout by mid week. A Cup with Handle formation may target 23.50, should the prior high be demolished.

USD futures are still consolidating in range. However, today may be the beginning of a period of strength that may ramp higher through the end of the year. The next Master Cycle interval occurs in the second week of January.

The Shanghai Composite Index made its Master Cycle high on Monday, crossed beneath its Cycle Top support on Tuesday and continued making a new low today. It is on a sell signal and sits atop a massive Cup with Handle formation with an average target of 2047.00. Its next Master Cycle interval (low) is due in the last week of January.

ZeroHedge reports, “Chinese stocks were under pressure in the overnight session as the Biden administration proposed stricter sanctions on China’s largest chipmaker, according to Bloomberg.

The Hang Seng Tech index closed down 1% to 23,420 amid worries of further regulatory crackdowns on Chinese tech companies by the US.

The reason for the downdraft in Chinese stocks is the National Security Council will hold a meeting Thursday to tighten the rules on exports to China’s largest chipmaker, Shanghai-based Semiconductor Manufacturing International Corp (SMIC).”

West Texas Intermediate Crude is back on its sell signal, having crossed beneath its mid-Cycle support at 70.73 yesterday. I had previously warned on December 3 that crude oil had hit its Master Cycle low and was due for a bounce of up to two weeks. Tis is it. The Cycles Model suggests an acceleration of the decline starting over the weekend with the next Master Cycle low due at the end of January. There is a possible alternate configuration suggesting a lower target beneath 40.00. Good luck!