2:15 pm

SPX made two 8.6-hour declines from the high at 4731.99. Today it has complete an 8.6-hour rally from the low. It may now be ready for another 17.2-hour decline from here, closing out the day before Christmas Eve at a new low. Coal in the stocking, anyone?

VIX made a low f 20.90 this afternoon and is on the same (inverted) Cycle as the SPX.

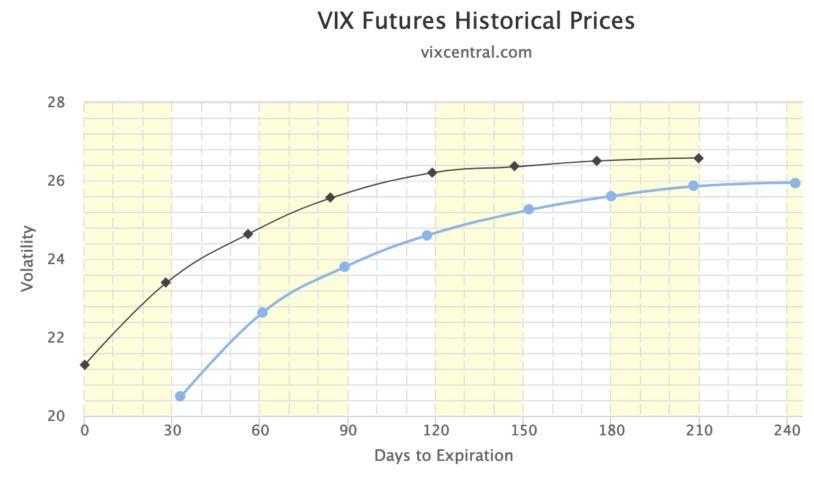

ZeroHedge comments, “Tomorrow is VIX expiration, and, as SpotGamma notes, we head into that expiration with an elevated VIX structure. If you compare today’s VIX term structure to that of mid-November you can see current levels (black) remain well above Nov(blue).

Nov is “pre Omnicron” and “pre Taper” so it makes sense that current prices are elevated – but we suspect that the VIX expiration will start to drag current prices lower as traders roll.”

10:40 am

Here’s some insight into the VIX options about to expire tomorrow, December 22. This morning VIX pulled back into its Max Pain zone at 23.00. Gamma turns positive at 24.00 with open interest in 71,786 call contracts vs. 52,984 put contracts, which aligns with the Cycle Top resistance. Above that VIX options are remarkably positive with a net 37,000 calls at 26.00, a net 121,500 calls at 30.00, a net 74,000 calls at 35.00 and a net 102.800 calls at 40.00. Should VIX rally above 24.00, we may see a mighty panic-driven blast higher in the next 24 hours.

This contrasts to the analyst highlighted in the article below. The hourly Cycles Model suggests one more (panic-driven) decline in the SPX before the holiday break.

Zerohedge comments, “As cash indices were grinding to session lows yesterday, Nomura’s Charlie McElligott points out that there was substantial closing-out of downside (selling Puts / Put Spreads to close – notables incl ARKK and KWEB, as well as a bunch in single-name) along with some buying of upside (KRE Calls and Call Spreads, XBI CS, single-name ‘stock replacement’ trades). In other words, constructive behavior, taking some protection off, others tilting to offense, and perhaps that explains the rebound overnight in futures…”

7:45 am

Good Morning!

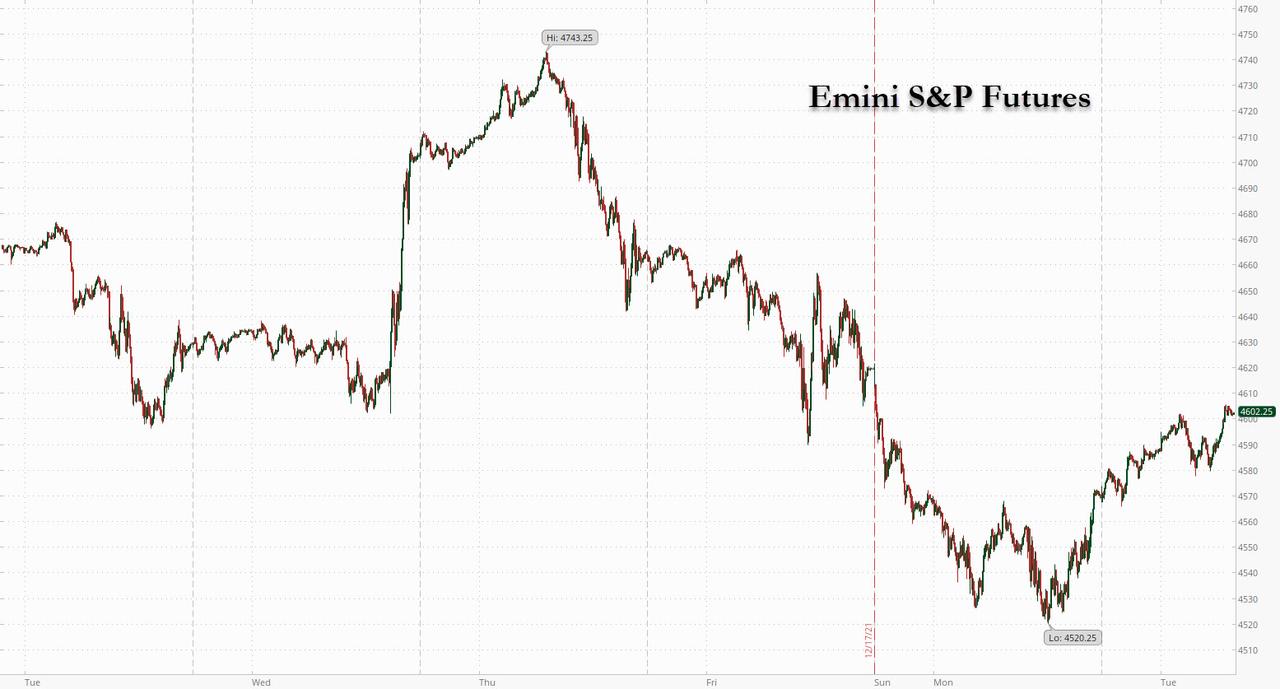

SPX futures went higher than expected, to 4615.20 this morning, the 61.8% retracement level. As usual, tomorrow’s options expiration has a lot to do with it. The 4550.00 strike with 4916 open interest put contracts was an obvious level to avoid. However, negative gamma stretches up between 4580.00 to 4605.00 with gamma flipping positive at 4620.00 (can’t go there!). A possible level to watch is 4620..64, the top of gap left on Friday. Inability to overcome that leel suggest this bounce is short covering and not fresh capital being put to work. The same levels apply to the December 23 options expiration. Friday is a full stock market holiday.

The Cycles Model suggests at least another day of decline in the current hourly Cycle, so what we are seeing is a coiling action that may propel equities much lower. The Wave (4) low appears to be a possible target at 4278.94,a 10% decline from the November 22 peak.

ZeroHedge reports, “Perhaps catalyzed by Goldman’s persistent bullishness (see “As Markets Slide, Here Is Goldman’s Bull Case: $125 Billion In January Inflows“), or perhaps it was just a booster shot of optimism that vaccines will keep the omicron outbreak in check coupled with hope for a revival of Joe Biden’s $2 trillion economic package (see “Here Is The “Fallback Plan” Manchin Would Support… And Why Goldman Thinks It Wouldn’t Move The Needle“), or maybe the Santa rally decided to make a scheduled appearance (it usually begins on Dec 21) but on Tuesday US futures, Asian markets and European bourses all rebounded after three days of steep selling. Emini S&P futures were up 1% or 44.50 points, Nasdaq futures were up 170 points ot 1.09% and Dow futures were up 314 points or 0.9% as the recent bout of turbulent moves continues. Europe’s Estoxx50 was higher by 1.3% as the mining sector climbed 2.4%. Asia stocks closed higher bolstered by a rebound in Japan (+2.1%) and a rally in Chinese property developers. 10Y yields rose above 1.45%, the dollar was flat and cryptos jumped, with bitcoin trading close to $50,000 again and ether above $4000.”

VIX futures made a low of 21.64 this morning. It also is showing coiling action with a Master Cycle peak (Wave 3?) anticipated on or near December 28. That outlook may change should VIX decline beneath 20.49.

The NYSE Hi-Lo Index showed serious erosion yesterday, suggesting any bounce today may be short-lived, despite its strength.

NDX futures rose to an overnight high of 15831.90, then receded back beneath 15800.00. The 50-day Moving Average is the key resistance here. The next level of support is the Ending Diagonal trendline at 15250.00. The hourly/daily Cycle may find support at Wave (4) at 14384.93 by the end of the year.

Yesterday’s close of the NDX Hi-Lo Index tells us that the overnight action is short covering and not due to any serious addition of capital. It also remains on a sell signal.

The Banking Index broke through its trendline and its 200-day Moving Average at 128.87 yesterday, giving us a very serious selling confirmation. The Cycles Model suggests two more weeks of selling in what may be an Intermediate Wave (3) decline. This decline may be a vicious one, since the current Cycle appears to end in early January with quadruple strength on the downside.

ZeroHedge relates, “The economist consensus is optimistic about economic growth in 2022.

Financial conditions will remain broadly accommodative despite monetary policy tightening. With a faster vaccine rollout and new Covid antibody cocktails, the pandemic will be under control, at least in the developed world. The direct inflationary effect of bottlenecks will progressively vanish. On the production side, supply will increase and will reduce the risk of shortage.

But what if the consensus is wrong?

Our proprietary leading indicator for growth, the global credit impulse, flashes a warning to major economies. It tracks the flow of new credit issued by the private sector as a percentage of GDP. In our sample, we have the eighteenth largest economies which represent 69.4 % of global GDP share. The global credit impulse is now in contraction territory, running at minus 1.3 % of global growth, according to our preliminary estimates.”

TNX vaulted above the 100-day Moving Average to test the mid-Cycle resistance at 14.75. There may be enough trending strength to break out above its Cycle Top in the next week. The new Master Cycle may stretch to mid-February with particular strength in the third week of January.

ZeroHedge remarks, “If you did any Fed watching this week, you probably heard all about how Jay Powell has turned (or perhaps returned) to hawkishness, and how the Federal Open Market Committee is all about fighting price inflation now.

A particularly cartoonish version of this claim was written by Rex Nutting at MarketWatch, who declared, “Everyone’s a hawk now. There are no doves at the Fed anymore.” He wrapped up with “This means that inflation no longer gets the benefit of the doubt. It’s been proven guilty, and even the doves will prosecute the war until victory is won. For the inflation doves at the Fed, Nov. 10, 2021, was bit of [sic] like Dec. 7, 1941: Time to go to war.”

USD futures pulled back after rising back above the Cycle Top resistance at 96.50. Trending strength may return next week with a clear breakout above previous highs. The current Master Cycle is due to pivot in the second week of January, leaving time for a 61.8% retracement of the 2020 decline at 98.30.