3:22 pm

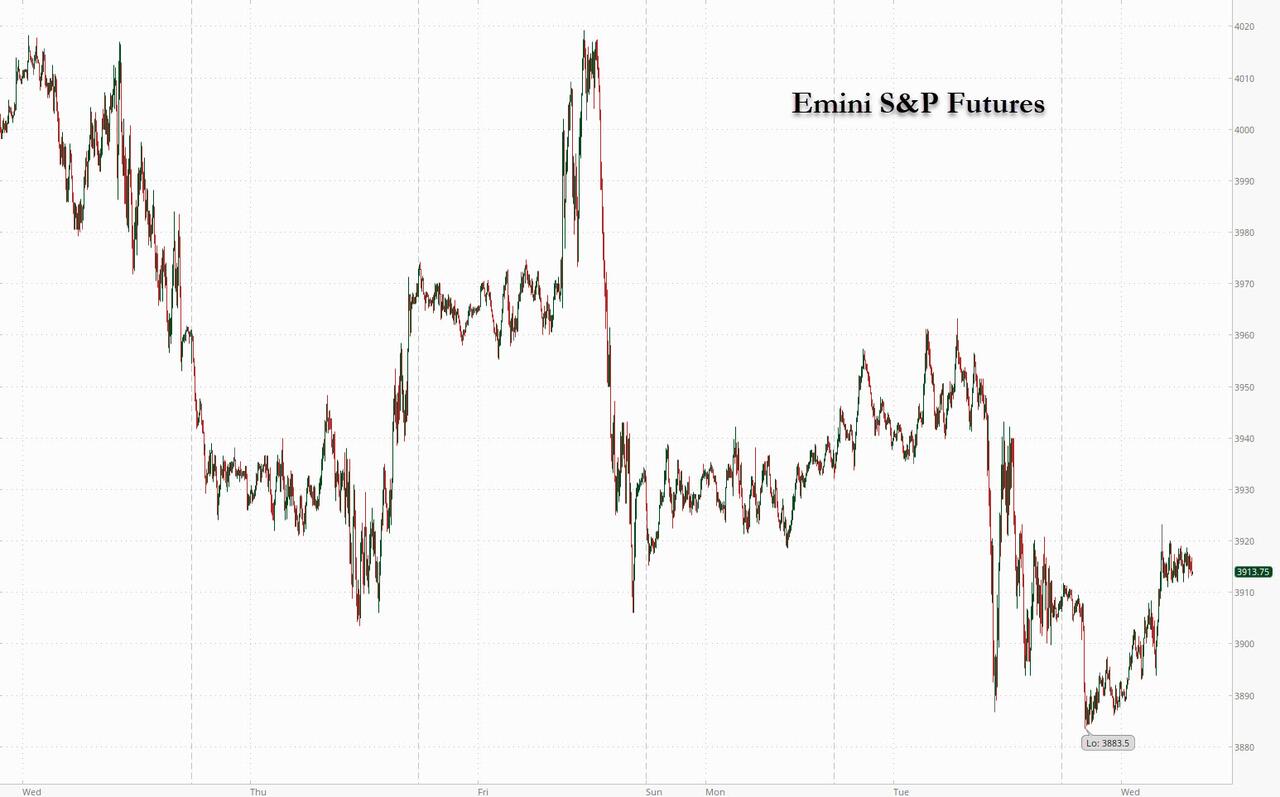

The SPX has clearly violated the neckline of its most recent Head & Shoulders formation at 3903.65 by declining to 3886.75. It is currently struggling to get back above 3925.00 where short gamma begins. Even if it succeeds, the door is still wide open for one or more limit down days by the end of the week. Stand by for the next panic leg (or two) down.

2:52 pm

The cause of our malaise in the markets is the collapse of the Euro. It was created on January 1, 2000 and became the official currency in Europe on January 1, 2002. The chart shows those dates clearly. Sir John Templeton explained it to me, recommending Euro stocks in my clients portfolio. We made a killing, more than doubling our investment on the currency alone. However, there was a fatal flaw. They never consolidated their individual country debts into Eurobonds, like the US Treasuries. As a result, one by one, the weaker countries imploded. In 2014, Eurobonds with negative interest rates were created. That action crossed the trendline (Lip) of a Cup with Handle formation that spelled the end to the Euro’s strength. 86 months later (June 2022), it slipped beneath all supports and is now teetering toward collapse. In April 2020, it may have left another Cup with Handle formation with an even lower target at 65.72.

In the meantime, on October 2020, US banks refused to take any more Euro-denominate debt, creating a credit crisis where the Fed had to step in to bail out European banks! What actually triggered the crisis is the Federal reserve starting to raise interest rates in June. The Europeans, who will not borrow their own currency, are deep in US debt and can no longer pay the rising interest rates, much less a more expensive currency.

We will know more by the end of October , when the current Master Cycle ends. The combination of the collapse in Europe and our upcoming election is likely to affect us, as well. This will not turn out well.

ZeroHedge outlines the problem, “What is the scale of the energy challenge?

We got a very shocking sense of the staggering numbers involved in the existential, crippling European crisis earlier today when Norwegian energy giant Equinor echoed what Zoltan Pozsar said in March, warning that “European energy trading risks grinding to a halt unless governments extend liquidity to cover margin calls of at least $1.5 trillion.” As Bloomberg put it, in its best non-Zoltan imitation, “aside from inflating bills and fanning inflation, the biggest energy crisis in decades is sucking up capital to guarantee trades amid wild price swings. That’s putting pressure on European Union officials to intervene to prevent energy markets from stalling.”

10:55 am

BKX, our liquidity proxy, may be about to break down through its massive Head & Shoulders neckline at 97.01. This formation is largely unrecognized, because it measures 17.2 months from point-to point at the low. Most technicians will recognize a 3-month long formation and sometimes a 6-month formation, if they are observant. However, the Cycles may measure in years and sometimes decades that often give a better view “from the top.”

8:15 am

Good Morning!

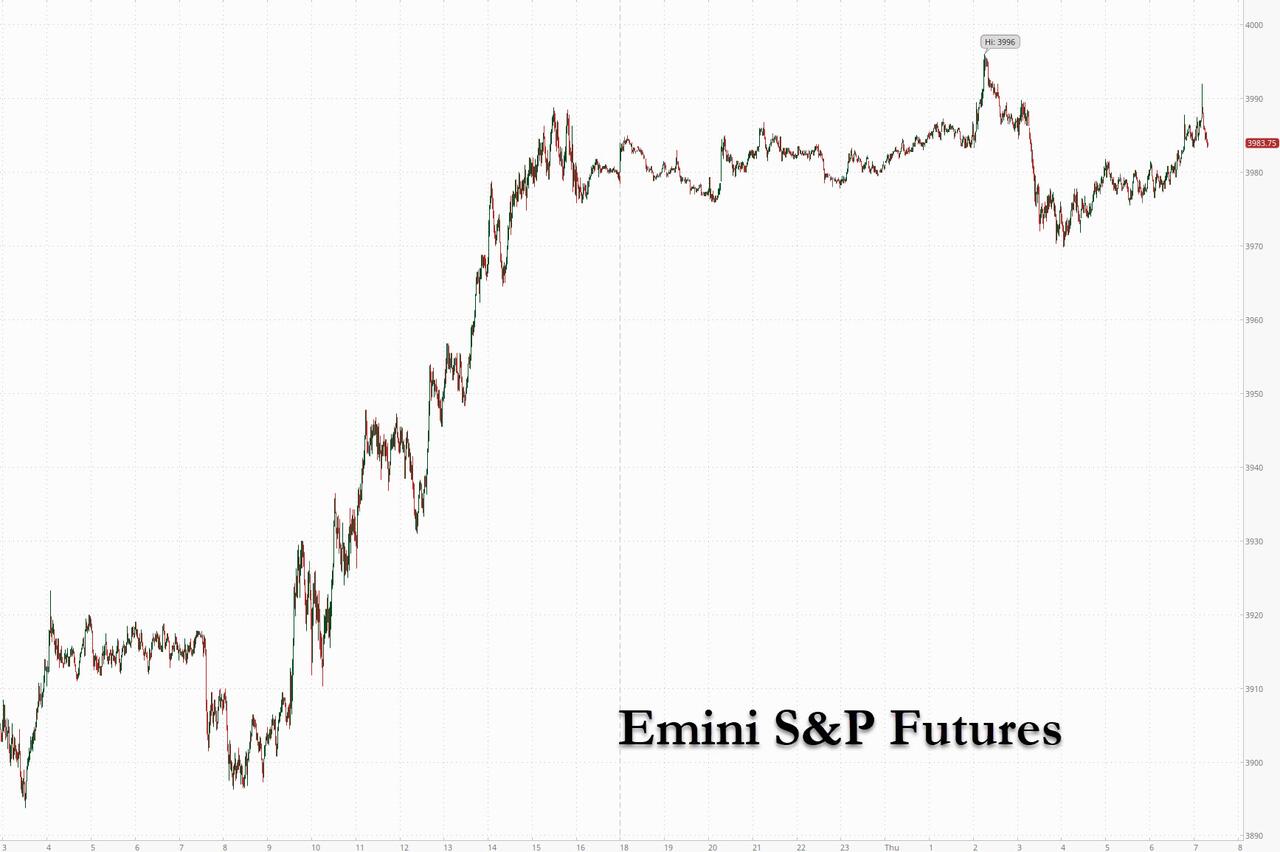

NDX futures made a 48.8% retracement of Friday’s debacle to12238.90, fulfilling its retracement requirements for the decline…and the complete hourly Cycle is taking 4.3 hours from Friday’s high. No one is expecting a bounce this short, but it may be complete and ready for the next big push lower. This week is primed for a Panic Cycle and we may see a limit down day (-7%) by the end of the week. Possibly two limit down days may ensue, since a 7% decline only takes the NDX to 11381.00, only halfway to the minimum Head & Shoulders target. Nervous investors and advisors are anticipating a bounce today, but the Cycles Model suggests that the market is so deep in short gamma that this decline may not end until September monthly Options Expiration.

Om today’s op-ex, Max Pain is at 12275.00, while short gamma begins at 12225.00, which explains the bounce this morning. However, the Cycles Model suggests a possible reversal in the first hour of the day.

ZeroHedge offers this thought, “NASDAQ – 12k is huge

NASDAQ has entered significant support areas with the first big one being the 12k level. Note the 50/100 moving day average cross on the shorter term view. Just about to happen?

Source: Refinitiv

We are in deep short gamma

Recall that short gamma dealers do not care about direction. They must sell low and buy high mechanically (we have still not met the short gamma trader that manages trading deltas successfully). This mechanical hedging flow works both ways, so don’t forget that a possible move higher will force dealers to start chasing deltas higher (and the inverse works should we sell off, dealers will need to sell deltas).”

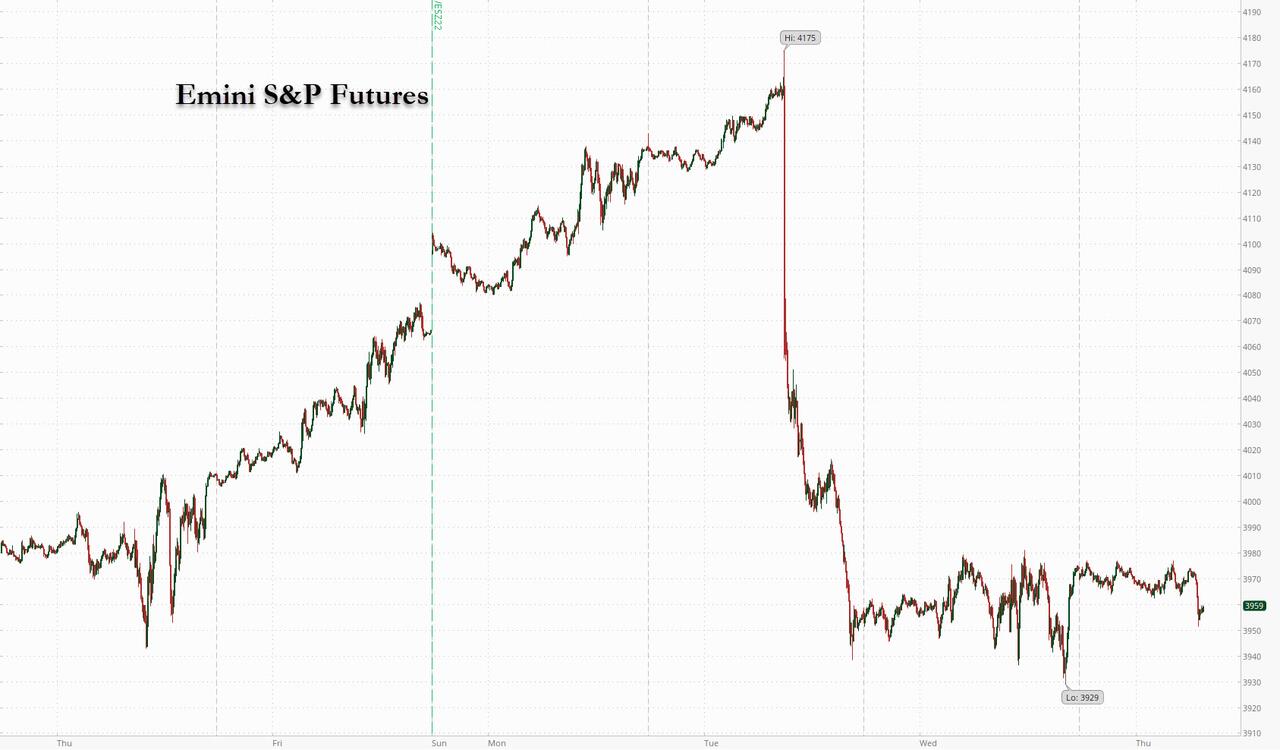

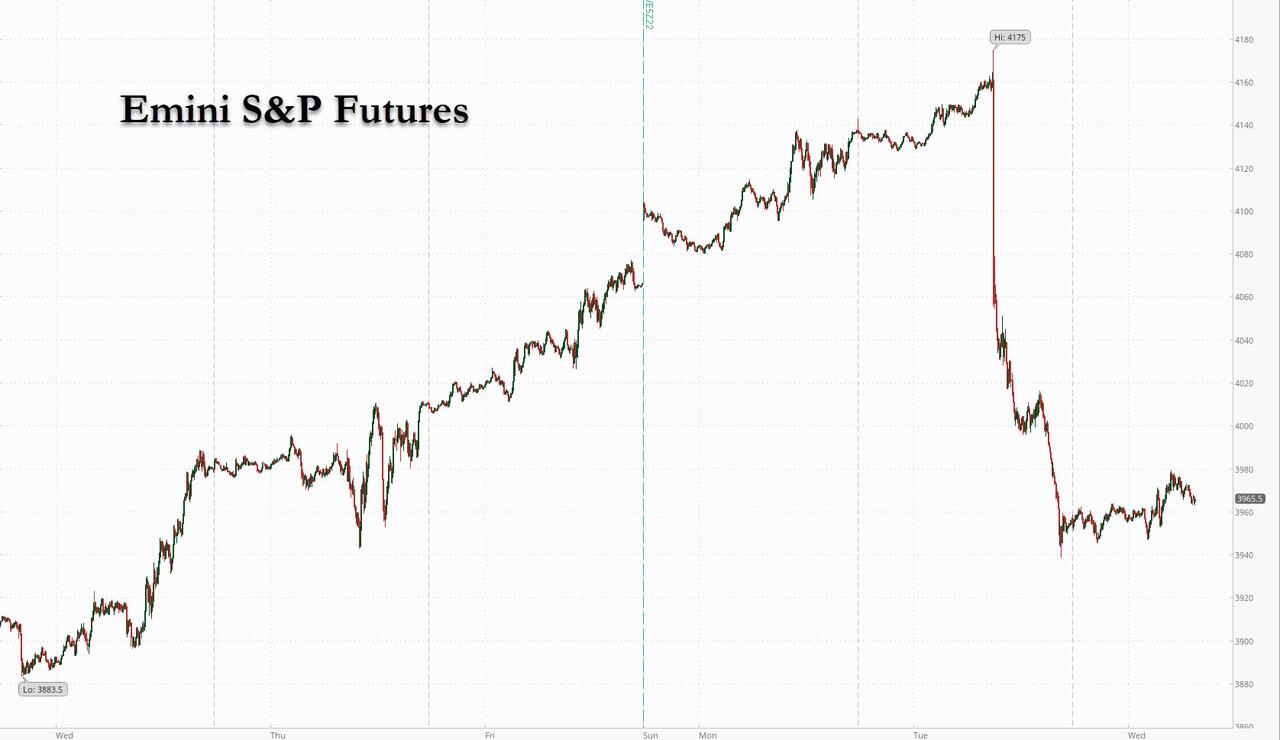

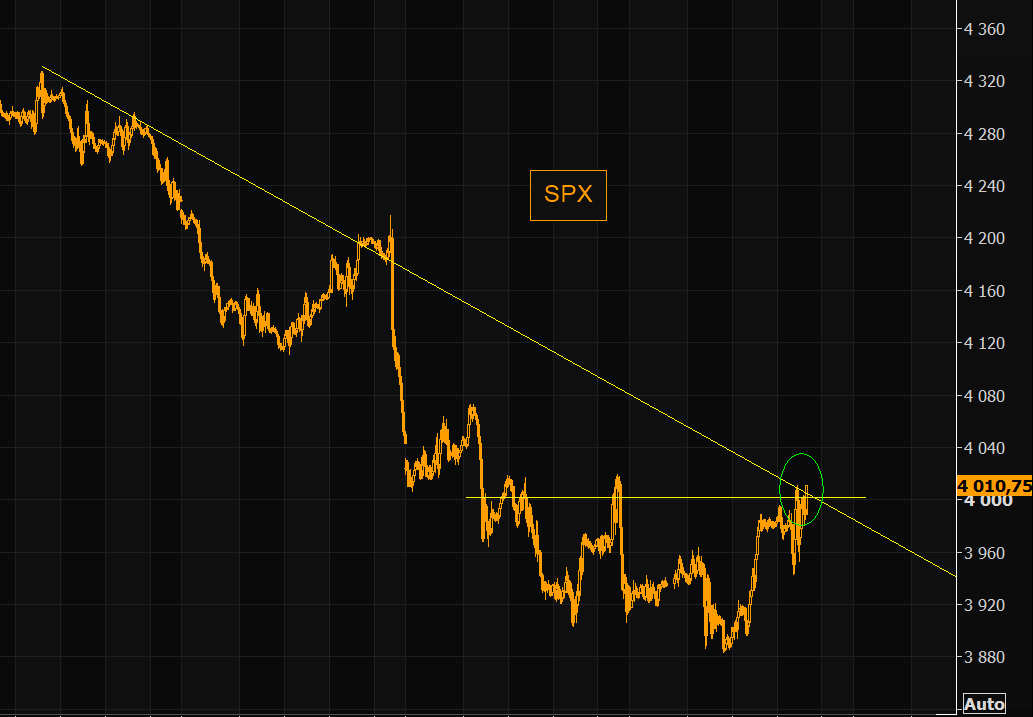

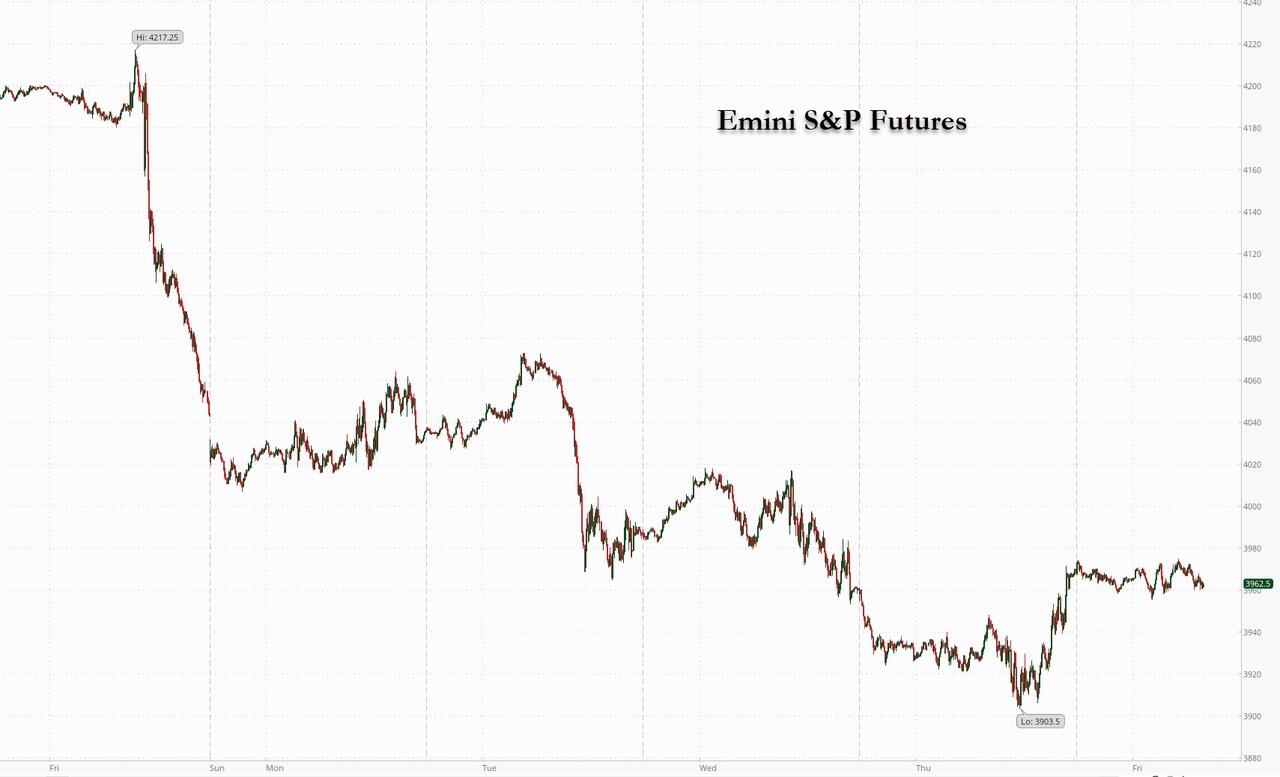

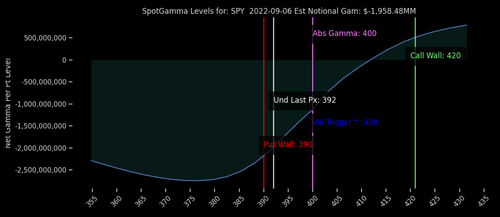

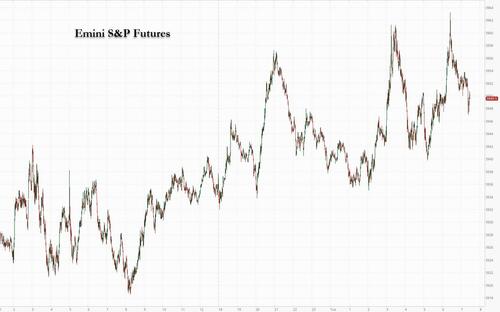

SPX futures rose to a weekend high of 3962.60, an exact 50% retracement of Friday’s decline. Should the SPX limit down today, its decline would take it to 3685.00, leaving investors and advisors calling it “capitulation” and expecting the bounce to gain traction. Unfortunately, the old-fashioned technical expertise has left the markets and no one sees the alternative outcome, which is “more decline.”

In today’s op-ex, Max Pain is at 3975.00. However, long gamma doesn’t begin until 4020.00. Options turn short at 3965.00 and short gamma kicks in with a bang at 3925.00. You can see why dealers did not want the SPX to close any lower on Friday.

ZeroHedge reports, “Following a flat Monday futures session when the US was closed for Labor Day and European stocks slumped as Russia confirmed it would halt NS1 pipeline flows indefinitely, on Tuesday European stocks and US equity futures rose as governments attempted to blunt the growing energy crisis, injecting tens of billions in fiscal stimulus to offset soaring energy prices and undoing central bank attempts to crush demand with tighter financial conditions. S&P futures rose 0.6% as Wall Street was set to resume trading after the long weekend, while Nasdaq futures rose 0.7%, ignoring – for now – news of more Chinese lockdowns. Meanwhile, as traders eyes the flood of fiscal “energy support”, Treasuries fell across the board, taking the two-year yield to 3.46%, while oil edged down reversing yesterday’s OPEC+ production cut gains on demand risks from fresh Chinese Covid lockdowns. The pound rebounded as traders assessed the agenda of incoming PM Liz Truss. European natgas prices eased with politicians scrambling to find solutions after Moscow switched off its main pipeline to the continent.”

VIX futures eased down to 25.33, a 31.7% retracement. The Cycles Model suggests a rally in strength for the next 2-3 days as the VIX completes is first bullish Wave from the Master Cycle low. A minimum target may be near 36.00, but it is just as likely to challenge the Head & Shoulders neckline at 40.00.

In tomorrow’s op-ex, Max Pain resides at 21.00. While puts are numerous and widely dispersed, they seem to have no traction above 20.00. Calls dominate above 22.00 with long gamma beginning at 27.00. Once above 27.00, long gamma appears in full force to 50.00, suggesting the neckline may be breached.

CNN offers this advice, “Markets are hard to predict right now, and that’s raising a question for some on Wall Street: Does a common measure of volatility actually work the way it should?

Traders don’t have a crystal ball to measure the level of risk when they make investment decisions. Instead they depend on the VIX, or the Chicago Board Options Exchange Volatility Index.

Known as Wall Street’s “fear gauge,” the index is supposed to reflect the market’s estimate of future volatility — or how fast prices will change — 30 days out.

An elevated VIX means increased fear and risk while a low VIX means the market is entering a less stressful period. That’s why the VIX tends to move in the opposite direction of the market.”

TNX (cash market) rose to 33.42 at the open, as fear of higher rates may give way to fear of a panic stock market. The current Master Cycle has extended to 277 days, above the normal 2 standard deviation allowance attributed to these Cycles. This panic may last until mid-November, lopping as much as 50% off the current yield.

That may drive UST to a range of 128.00 to 132.00 by mid-November from Friday’s close at 116.88. For those who have some cash set aside and choose to be more conservative with their investments, TLT may offer a long alternative.

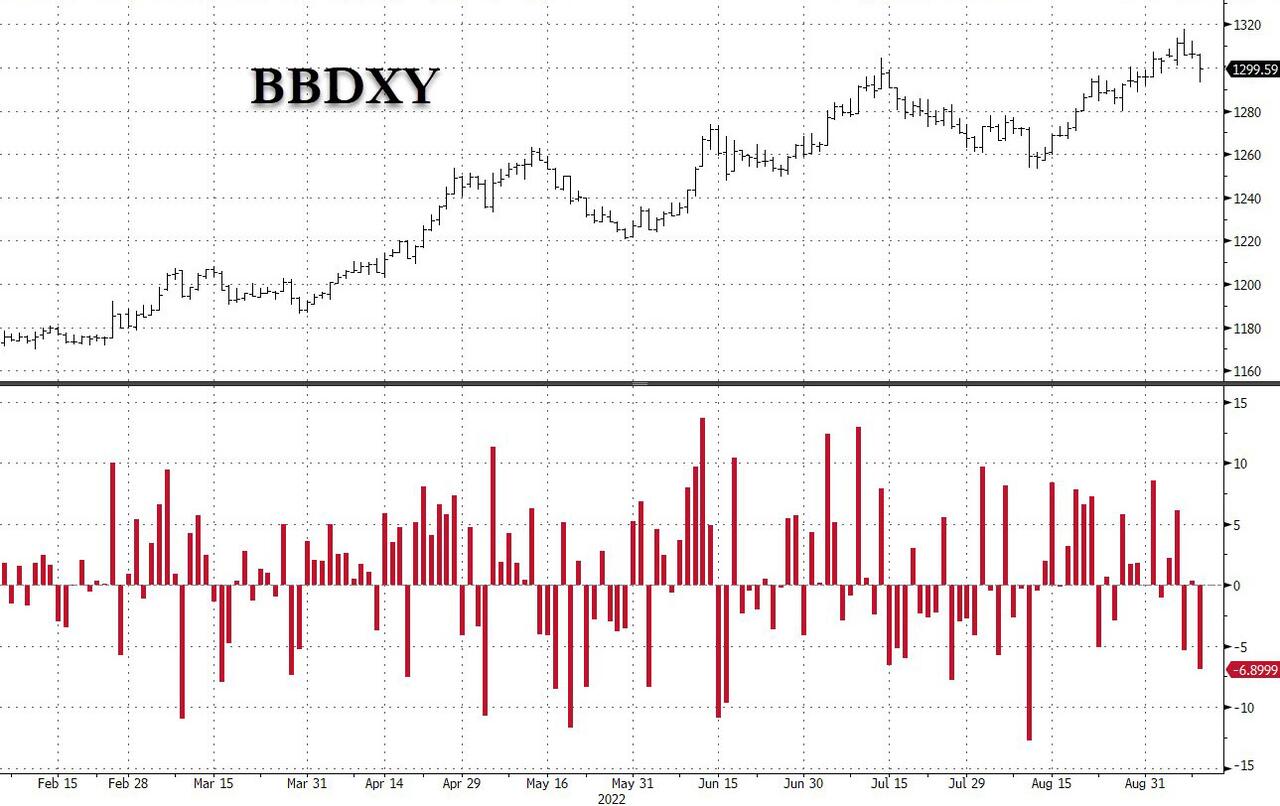

USD futures broke out to a new high at 110.54 this morning, as pressures on the Euro and Yen continue to rise. The Euro, currently priced beneath 100.00, is in a formation that may take it to 65.00. More on that later. In the meantime, the Cycles Model suggests a Panic Cycle beginning this week and lasting through the end of September. The threat of breaching the July 2001 high at 121.21 looms high.

WTIC futures declined to a weekend low of 86.20 as it tests the prior Master Cycle low at 85.73. Should it break down, there may be nearly two months of decline. People have asked me why I still have the Broadening Wedge target in full view, despite rising crude oil prices. The main reason is that the European “fix” may fail miserably, leaving a huge void in liquidity in all markets, including oil.

ZeroHedge reports, “As we detailed over the weekend, many companies are finding it increasingly difficult to manage margin calls, an exchange requirement for extra collateral to guarantee trading positions when prices rise…

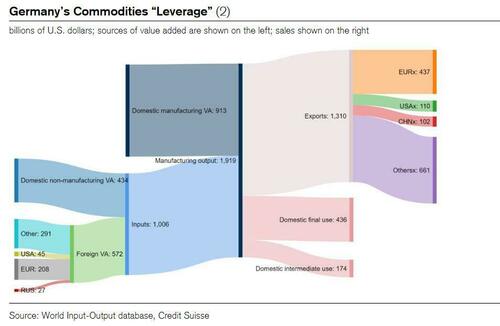

Credit Suisse repo guru Zoltan Poszar published what may have been the most insightful snippet of the entire European energy crisis (to date) when he extended the infamous “Minsky Moment” framework to Europe, and specifically Germany, which he said “can’t cover its payments without Russian gas and the government is asking citizens to conserve energy to leave more for industry.” He then elaborated that “Minsky moments are triggered by excessive financial leverage, and in the context of supply chains, leverage means excessive operating leverage: in Germany, $2 trillion of value added depends on $20 billion of gas from Russia… …that’s 100-times leverage – much more than Lehman’s.”

(Zoltan’s entire note is a must read for everyone with a passing interest in what comes next).

But while Germany is front-and-center in this margin call malaise, many other European nations are suddenly succumbing to what Zoltan dubbed a “supply-chain Minsky moment.”

10:25 am

Some leaders are planning massive bailouts to avert a crisis (rioting in the streets). Case in point, ZeroHedge observes, “Liz Truss, the Conservative Party’s new leader and incoming prime minister, drafted plans for a massive £130 billion support package over the next 18 months to help struggling households and businesses lower energy bills, according to policy documents seen by Bloomberg.

Truss faces massive economic challenges as energy hyperinflation, and a cost-of-living crisis darkens the outlook, with a recession becoming more likely. She has to act swiftly to avert social unrest.”

10:27 am

Other leaders are breaking ranks, as they see much more damage to their own countrymen than to Russia. ZeroHedge comments, “European solidarity continues cracking amid growing protests in different corners of the EU, with citizens angry at the collective policy of “standing up to Russia” in support of Ukraine at all costs. For example, Germany’s Foreign Minister Annalena Baerbock days ago openly expressed that she’s committed to support Ukraine “no matter what German voters think.”

But elsewhere, Italy’s League party leader Matteo Salvini, (which the mainstream media consistently dubs as “far-right wing” – though he would describe his party as the government of “good sense”) on Sunday broke ranks with other European leaders who have lately seemed to echo some form of this ‘Ukraine first’ policy.

On Sunday Salvini urged an end to Russia energy sanctions which are only leaving Europeans “on their knees” due to higher energy bills and lack of supply. “Several months have passed and people are paying two, three, even four times more for their bills,” he said in an interview RTL radio. “And after seven months, the war continues and Russian Federation coffers are filling with money.”

He explained that not only are the sanctions not working, but they hit Italy harder. While saying he stands in solidarity with Ukraine, he’s not willing to stick with something obviously counterproductive where the blowback is felt more in Europe, Italy in particular with its soaring energy import prices, and not the intended target of the Putin government.”

Gold futures rose to 1737.10, but has since backed down from Friday’s close. The Cycles Model suggest that gold may continue lower at least until Options Expiration in mid-September. Should it break through the Lip of the Cup with Handle at 1680.00 in the interim, a much deeper decline may ensue. Gold has lost its luster, primarily due to the lack of secure transportability and the threat of seizure, as the federal government tracks all transactions. Should gold break beneath the 2015 low at 1045.40, we may see gold decline further toward 800.00.

ZeroHedge reports, “Towards the end of July, news emerged in the Russian media that Moscow and a number of its Eurasian allies are now reviewing a proposal to create an entirely new trading and pricing infrastructure for the international precious metals in order to both destroy London and New York’s monopoly over global precious metals pricing, and to stabilize the Russian gold market.”